*Not meaningful

Source: Company reports/Coresight Research

*Not meaningful

Source: Company reports/Coresight Research

3Q18 Results

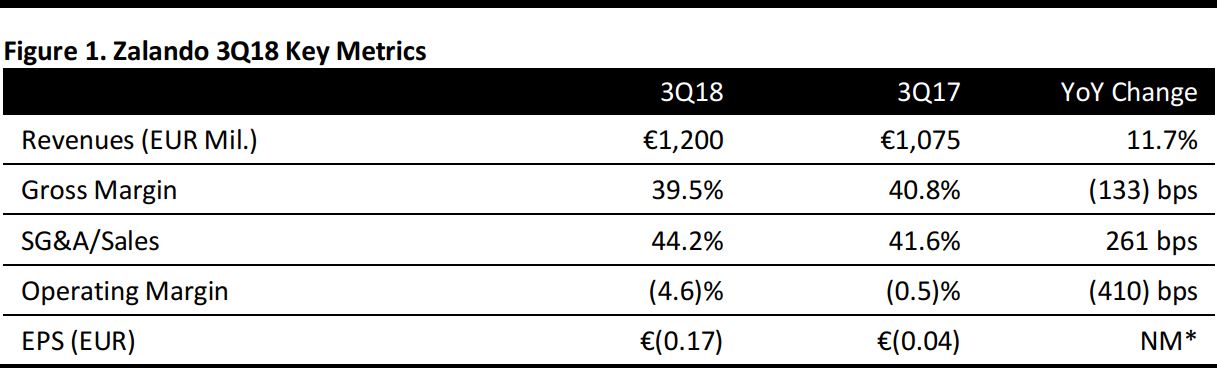

Zalando grew revenues by 11.7% year over year to €1.20 billion in 3Q18, slightly below the consensus estimate of €1.22 billion and a sequential slowing from the 20.9% growth in 2Q18. Growth in revenues were driven by a 16.6% increase in gross merchandise volume (GMV) and a 22.8% increase in the number of orders. A long, hot summer resulted in a late switch to fall and winter shopping and weighed on sales growth. The company reported an increase in the number of active customers to 25.1 million.

Zalando reported an operating loss of €55.7 million in the quarter, compared to an operating loss of €5.9 million in the year ago period. After adjusting for equity-settled share-based payments, restructuring costs and one-offs, EBIT came in at €(38.9) million, compared to €0.4 million in the year-ago quarter. Zalando attributed the increased expenses to the grant of further tranches under its share-based payments.

The EBIT margin was also hurt by increased SG&A costs, including rising fulfillment costs. Fulfillment costs added 3.1 percentage points to EBIT margin decline and included costs related to logistics and technology, as the company plans to expand its logistics network. Logistics costs were also impacted by a decrease in the average basket size and an increase in carrier prices.

Zalando reported a 7.3% year over year decline in the average basket size to €57.5, mainly due to the seasonal mix as a higher proportion of orders was for lower-priced summer articles available at higher discounts than fall articles.

Diluted EPS of €(0.17) fell short of the consensus estimate of €(0.13).

Segment Performance

- Fashion Store: This segment, which comprises full-price websites, grew revenues by 10.8% year over year and reported EBIT of €(54.8) million.

- Off price: This segment grew revenues by 40.2% year over year and reported an EBIT of €7 million.

- All Others: This segment, which includes private labels and various emerging businesses, reported 23.0% year-over-year increase in revenues and posted an EBIT of €(6.5) million.

Outlook

Management lowered its FY18 guidance and now expects full-year revenue growth to be around the lower end of the previously stated 20%–25% target range (lowered from 2Q18 guidance of the “lower half” of this range). It expects adjusted EBIT in the €150–€190 million range, revised from the previously stated €220–€270 million range.

The company plans to continue its investments in logistics and technology and anticipates spending €300 million in 2018, which is slightly lower than the previous estimate of €350 million.