DIpil Das

Introduction

The US womenswear market continues to grow, with selected categories such as occasion wear and plus-size wear driving the market. We are seeing consumers shifting away from the popular pandemic categories, such as casual and activewear, into more occasion-based apparel. In this report, we analyze the US womenswear market and identify key drivers and trends in the market. In addition, we examine what brands and retailers are doing to better capture the opportunities in the market. Our coverage of womenswear includes female (aged 15+) apparel, footwear and apparel accessories, excluding jewelry, watches and eyewear.US Womenswear Retailing: Performance and Outlook

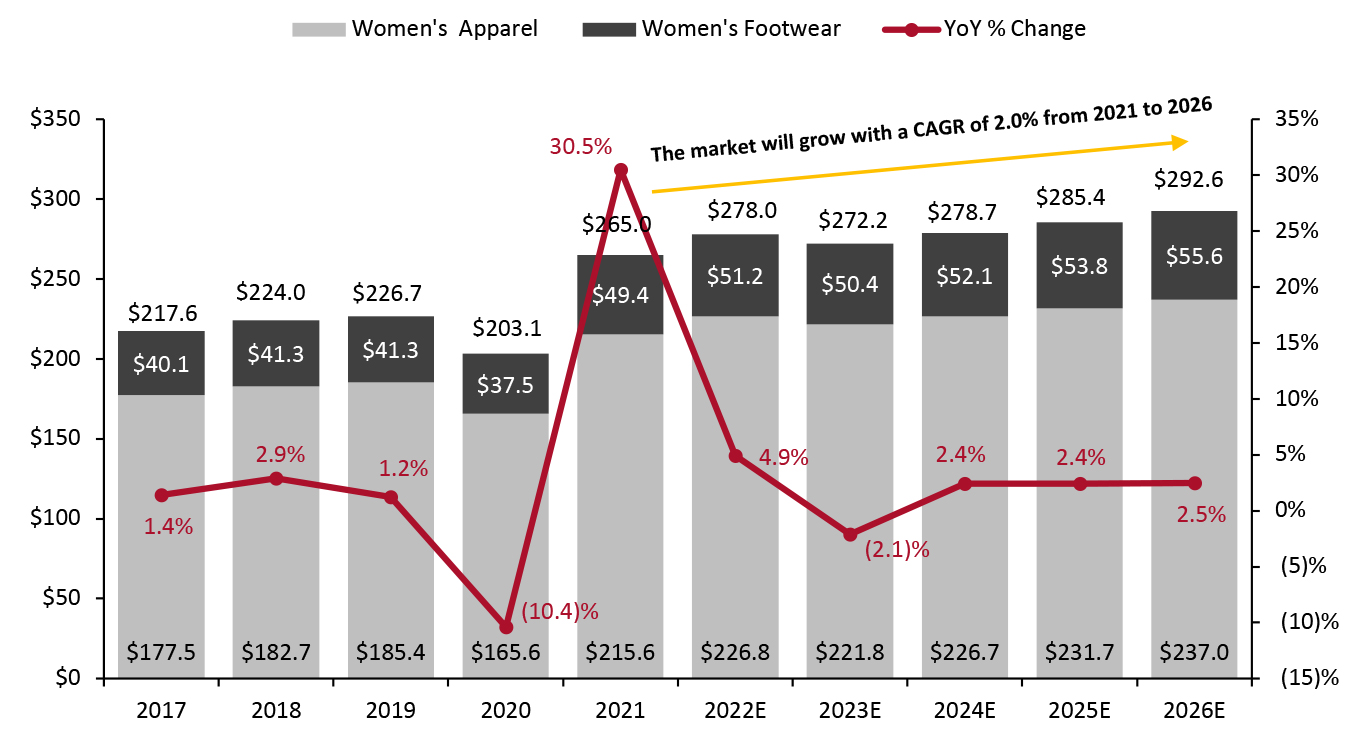

The US Womenswear Market Overview Propelled by rising prices, we estimate that the US womenswear market will grow 4.9% in 2022, marginally faster than the growth of the total apparel and footwear market, reaching $278.0 billion and accounting for 57% of the total market. By category, we expect women’s apparel to continue to dominate the womenswear market, with an estimated scale of $226.8 billion in 2022, capturing 81.6% of the total womenswear market. We estimate the women’s footwear market will reach $51.2 billion in 2022, capturing 18.4% of the total womenswear market. In 2022, consumers are participating in more activities and therefore are updating their wardrobes to refresh themselves. When we take into account other market drivers, such as the growing number of plus-size shoppers, the recovery of the occasion wear market, the growth of the shapewear market and inflation, we believe the momentum of consumer spending growth on women’s apparel and footwear will continue in 2022. Consumer spending on clothing and footwear remained solid from January to April 2022 (latest), according to the Bureau of Economic Analysis (BEA), albeit with growth accounted for by inflation in the latest two reported months. We expect price rises to be the driver of spending growth for apparel and footwear at a total level for the second half of 2022, with volumes down slightly, year over year, across the total market. We expect the market to see a low-single-digit percentage decline in 2023 as consumers will have already updated their wardrobes in 2021 and 2022, and the pent-up demand and effect of stimulus checks will have faded away. We estimate that the market will fully normalize in 2024 and return to low-single-digit percentage annual growth rates, similar to those seen before the crisis. The market will grow with a CAGR of 2.0% from 2021 to 2026. We estimate that the US womenswear market totaled $265.0 billion in 2021—up 30.5% year over year. This growth was primarily driven by the rollout of vaccinations and consumers’ return to more normal living habits. The market saw a strong recovery in 2021, at 16.9% higher than pre-crisis level. The market totaled $203.1 billion and $226.7 billion in 2020 and 2019, respectively.Figure 1. US Womenswear Sector Size (Left Axis; USD Bil.) and YoY % Change (Right Axis) [caption id="attachment_150194" align="aligncenter" width="699"]

Source: BEA/Coresight Research[/caption]

Women’s Apparel by Categories

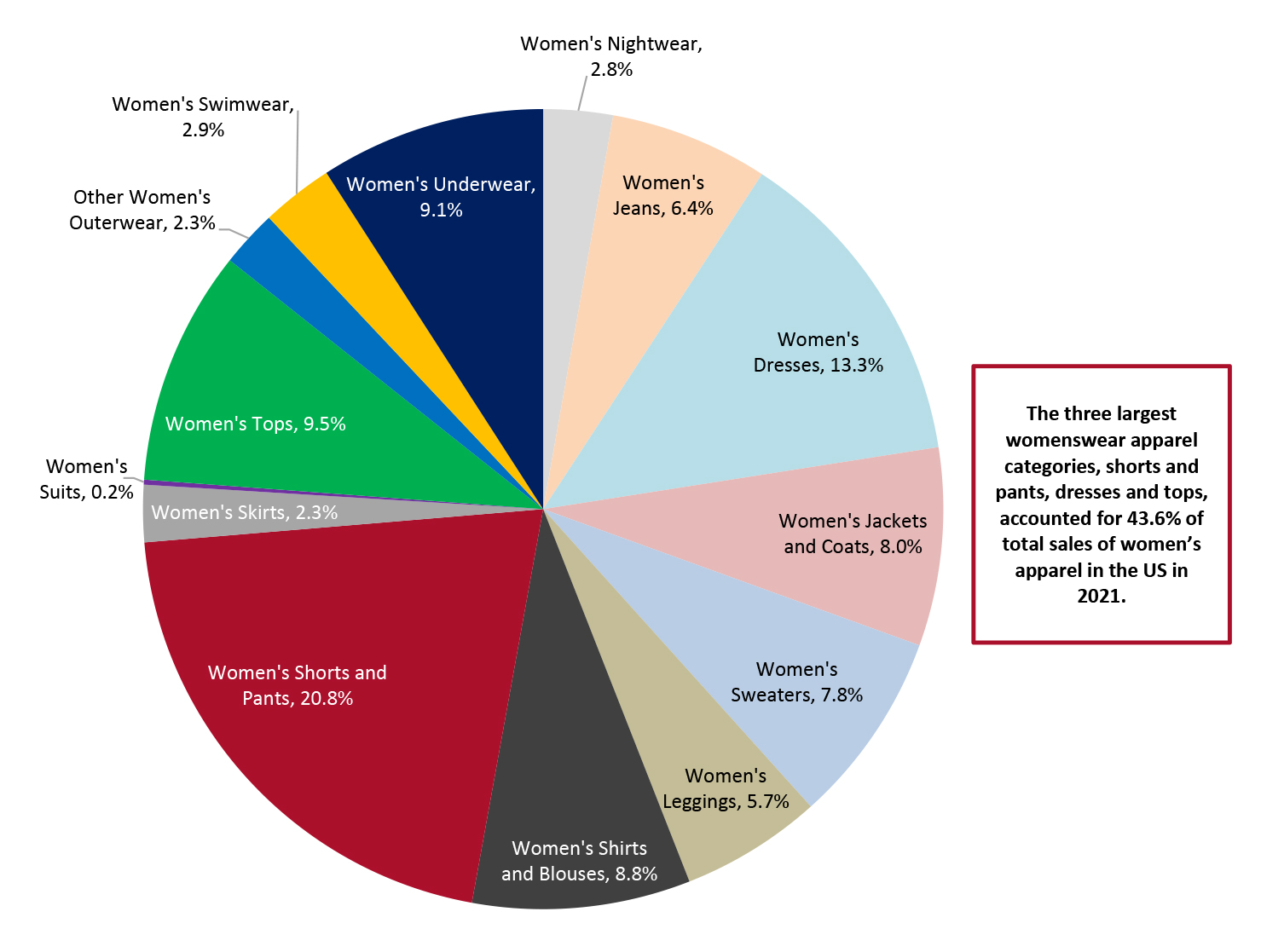

In 2021, the three largest womenswear apparel categories accounted for 43.6% of total sales of women’s apparel in the US in 2021, according to Euromonitor International: Shorts and pants comprise the largest category, with a 20.8% share of total sales, followed by dresses (13.3%) and tops (9.5%). Suits saw around $300 million in revenue in 2021, representing only 0.2% of the total market.

Source: BEA/Coresight Research[/caption]

Women’s Apparel by Categories

In 2021, the three largest womenswear apparel categories accounted for 43.6% of total sales of women’s apparel in the US in 2021, according to Euromonitor International: Shorts and pants comprise the largest category, with a 20.8% share of total sales, followed by dresses (13.3%) and tops (9.5%). Suits saw around $300 million in revenue in 2021, representing only 0.2% of the total market.

Figure 2. Women’s Clothing by Share of Category, 2021 (%) [caption id="attachment_150195" align="aligncenter" width="700"]

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

In 2022, we are seeing consumers shifting away from the popular pandemic categories, such as casual and activewear, into more occasion-based apparel, such as dresses. We expect categories in occasion wear (which consumers wear for special occasions such as weddings, social occasions such as parties and work), including blazers, blouses, dresses, skirts, leather shoes, shirts and suits will gain shares in the total apparel and footwear market, versus the casual wear and activewear market, as people are returning to the office or dining out with friends. We are seeing signs of occasion wear sales recovery and a revival of consumer demand in the market.

Figure 3 presents insights from brands and retailers compiled by Coresight Research.

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

In 2022, we are seeing consumers shifting away from the popular pandemic categories, such as casual and activewear, into more occasion-based apparel, such as dresses. We expect categories in occasion wear (which consumers wear for special occasions such as weddings, social occasions such as parties and work), including blazers, blouses, dresses, skirts, leather shoes, shirts and suits will gain shares in the total apparel and footwear market, versus the casual wear and activewear market, as people are returning to the office or dining out with friends. We are seeing signs of occasion wear sales recovery and a revival of consumer demand in the market.

Figure 3 presents insights from brands and retailers compiled by Coresight Research.

Figure 3. Category Trends Reported by Selected Apparel Brands and Retailers [wpdatatable id=2079]

Source: Company reports

Market Factors

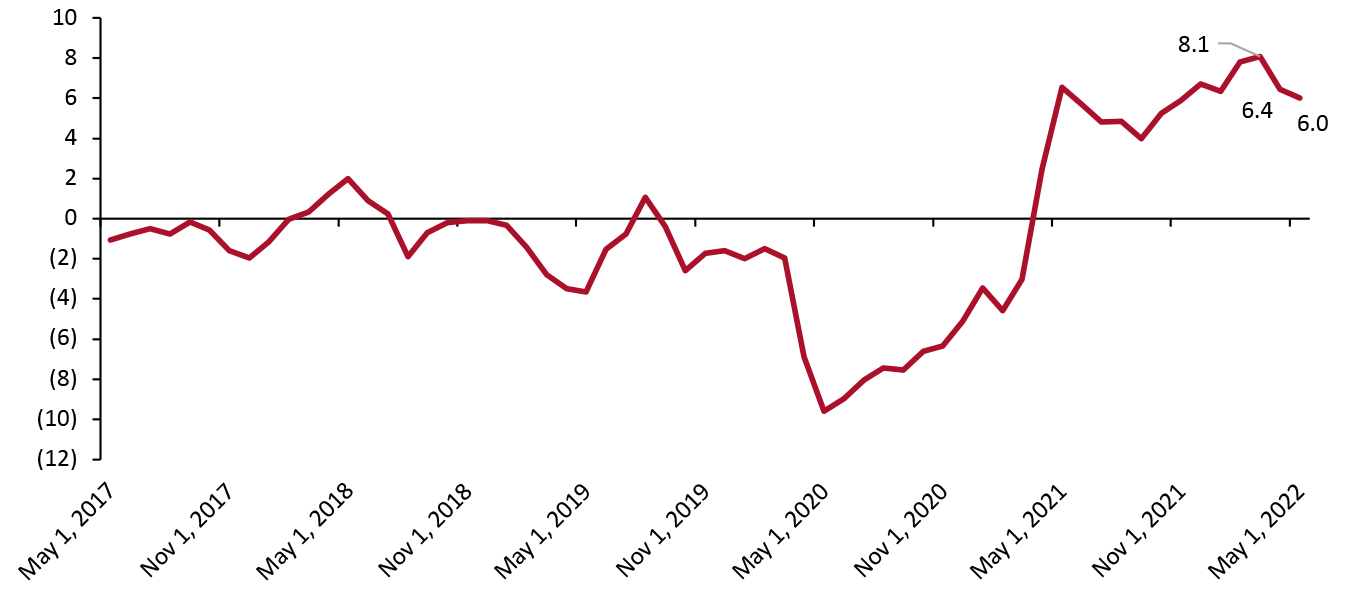

Growing Number of Plus-Size Customers The proportion of US adults that are overweight has been increasing in recent years, according to the Centers for Disease Control and Prevention. The US womenswear market has a further opportunity as consumers gained weight due to the Covid pandemic. 42% of US adults reported undesired weight gain since the start of the pandemic, with an average gain of 29 pounds, according to an American Psychological Association survey conducted in February 2021. We expect this will impact women’s apparel sales as women may require new sizes. A Return of Demand for Occasion Wear What will also drive the US womenswear market is a return to in-person events such as dining out, and therefore, the demand for occasion and more formal, dresswear categories, discussed in detail below in the themes section. Formal events such as weddings will also drive dresswear categories. There will be an estimated 2.5 million weddings in 2022, which is the most the US has seen since 1984, according to The Wedding Report, a market research firm. Many people postponed their celebrations during the pandemic and are planning to book venues and celebrate the weddings in 2022, which will drive women’s dresswear businesses. Brands and retailers are already seeing the recovery of occasion wear categories. Gap reported on March 3, 2022 that its subsidiary Banana Republic’s women blazers outperformed expectations in the quarter ended January 29, 2022. Nordstrom is seeing signs of renewing customer interest in post-pandemic occasion-based categories with improving trends in dresses, outerwear and women's shoes, according to the company’s earnings call on March 1, 2022. Shapewear Goes More Mainstream The shapewear industry has become a driving force in the US womenswear industry. Coresight Research estimates that shapewear accounted for approximately 3% of total US womenswear revenues in 2021; however, we expect this category to be one of the fastest growing for several reasons. First, consumers of all ages and sizes are seeking out shapewear for its smoothing properties. Second, many consumers are new to shapewear. Finally, brands and retailers are increasing shapewear innovations and offerings and the category is expanding to include more styles and colors. Shapewear is no longer considered a niche offering but is becoming more mainstream as evidenced by Spanx $1.2 billion valuation when the company sold a majority stake in October 2021 to Blackstone. Kim Kardashian’s Skims shapewear brand, which launched in 2019, has expanded into underwear, loungewear, maternity, accessories and even childrenswear, and it has collaborated with luxury designer Fendi. Skims was valued at $3.2 billion as of its latest investment of $600 million in January 2022, up from $1.6 billion in January 2021. Inflation We see inflation as an important driver of the US womenswear market. The US inflation rate in the apparel and footwear sector rose to 6.0% in May 2022 (seasonally adjusted), according to the Bureau of Labor Statistics. In March and April 2022, these year-over-year price rises exceeded year-over-year spending increases (as reported by the BEA), implying a real-terms erosion of apparel and footwear spend in those months. Rising prices will support the size of the womenswear market in 2022, likely concealing a weakness in volumes in the second half of the year and making consumers more selective about apparel purchases.Figure 4. YoY Changes of Consumer Price Index in Apparel and Footwear for All Urban Consumers (%, Seasonally Adjusted) [caption id="attachment_150196" align="aligncenter" width="699"]

Source: US Bureau of Labor Statistics[/caption]

Source: US Bureau of Labor Statistics[/caption]

Competitive Landscape

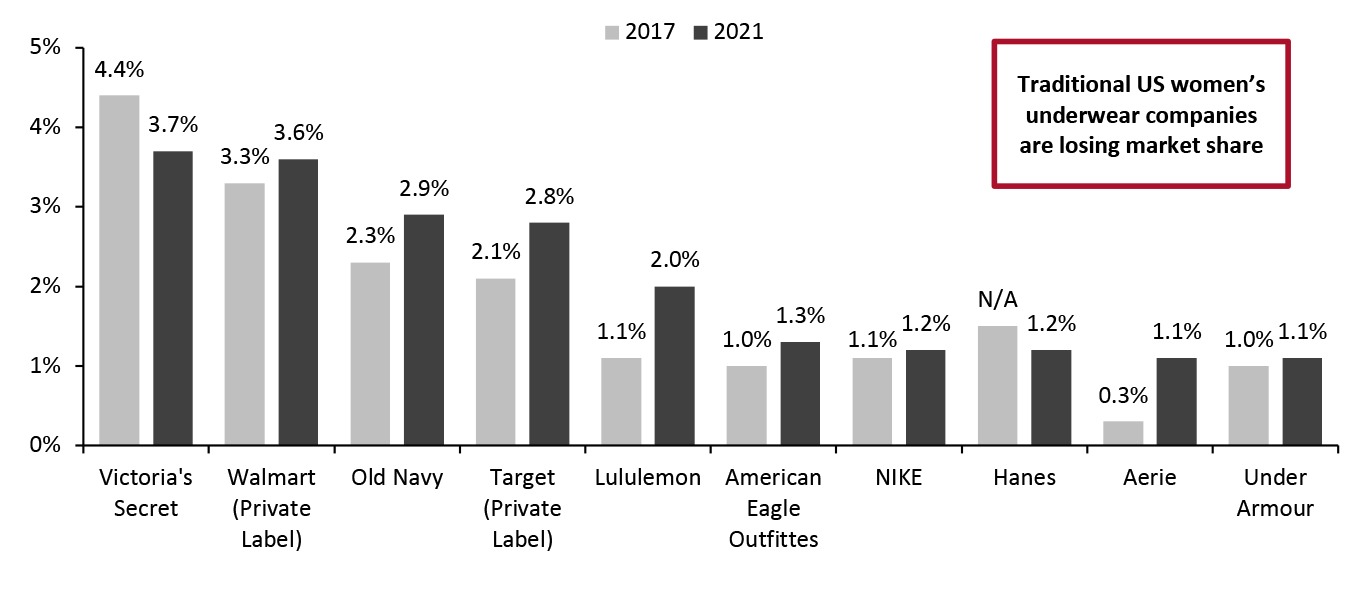

The US Women’s Apparel Market Is Fragmented Within the US women’s apparel market, the top 10 brands comprised 20.9% of the market in 2021, according to Euromonitor International. Victoria’s Secret is the leading brand, with a market share of 3.7% in 2021. The market has become more concentrated over the past five years; in 2017, the top ten US womenswear brands accounted for 18.1% of total sales. The athletic market has been gaining momentum over the past five years and saw growth in 2021 as compared to other underwear and casual brands and retailers. Athletic brands and retailers are focusing more on womenswear. For instance, NIKE launched the Dri-FIT Alpha Bra in early 2022 and saw momentum in women’s Free Metcon sneaker series. The company is also in the pipeline phase of launching the next generation of women’s leggings and bras, according to the company’s earnings call on March 21, 2022. NIKE is also investing in NIKE stores to specifically address gaps in distribution to serve the growth opportunities in women’s apparel. We expect big athletic brands to continue to grow, while small athletics brands will cede some shares to dresswear and occasion wear brands such as Ralph Lauren. Traditional US women’s underwear companies are losing market share. The market leader Victoria’s Secret has lost 0.7 percentage points in market share from 2017 to 2021. However, in 2021, Victoria’s Secret overhauled its image to become more inclusive and relevant with the modern woman. Victoria’s Secret also spun off from its parent company, L. Brands, in an IPO as its own public entity, VSCO, on August 2, 2021.Figure 5. Top Women’s Apparel Brands by Market Share, (%) [caption id="attachment_150197" align="aligncenter" width="700"]

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

The US Women’s Footwear Market Is Relatively More Concentrated Than the Apparel Market

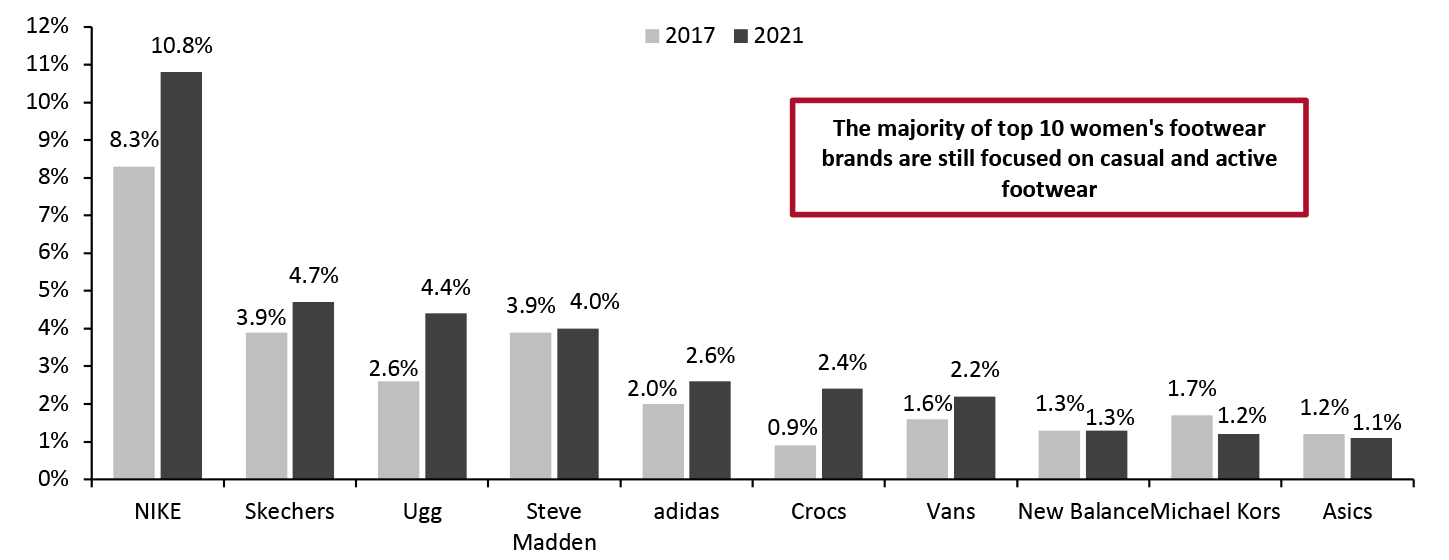

We still see casual and active footwear brands dominate the US footwear market. Among the leading 10 women’s footwear brands, nine of them are focused on casual and activewear footwear. Within the US women’s footwear market, the top 10 brands comprised 34.7% of the market in 2021, according to Euromonitor International. NIKE is the leading brand, with a market share of 10.8% in 2021. The market has become more concentrated over the past five years; in 2017 the top ten US women’s footwear brands accounted for 27.4% of total sales. We expect the market to be more concentrated as it is more brand-prominent than the apparel market.

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

The US Women’s Footwear Market Is Relatively More Concentrated Than the Apparel Market

We still see casual and active footwear brands dominate the US footwear market. Among the leading 10 women’s footwear brands, nine of them are focused on casual and activewear footwear. Within the US women’s footwear market, the top 10 brands comprised 34.7% of the market in 2021, according to Euromonitor International. NIKE is the leading brand, with a market share of 10.8% in 2021. The market has become more concentrated over the past five years; in 2017 the top ten US women’s footwear brands accounted for 27.4% of total sales. We expect the market to be more concentrated as it is more brand-prominent than the apparel market.

Figure 6. Top Women’s Footwear Brands by Market Share, (%) [caption id="attachment_150198" align="aligncenter" width="701"]

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

Where Consumers Are Shopping and What They Are Buying

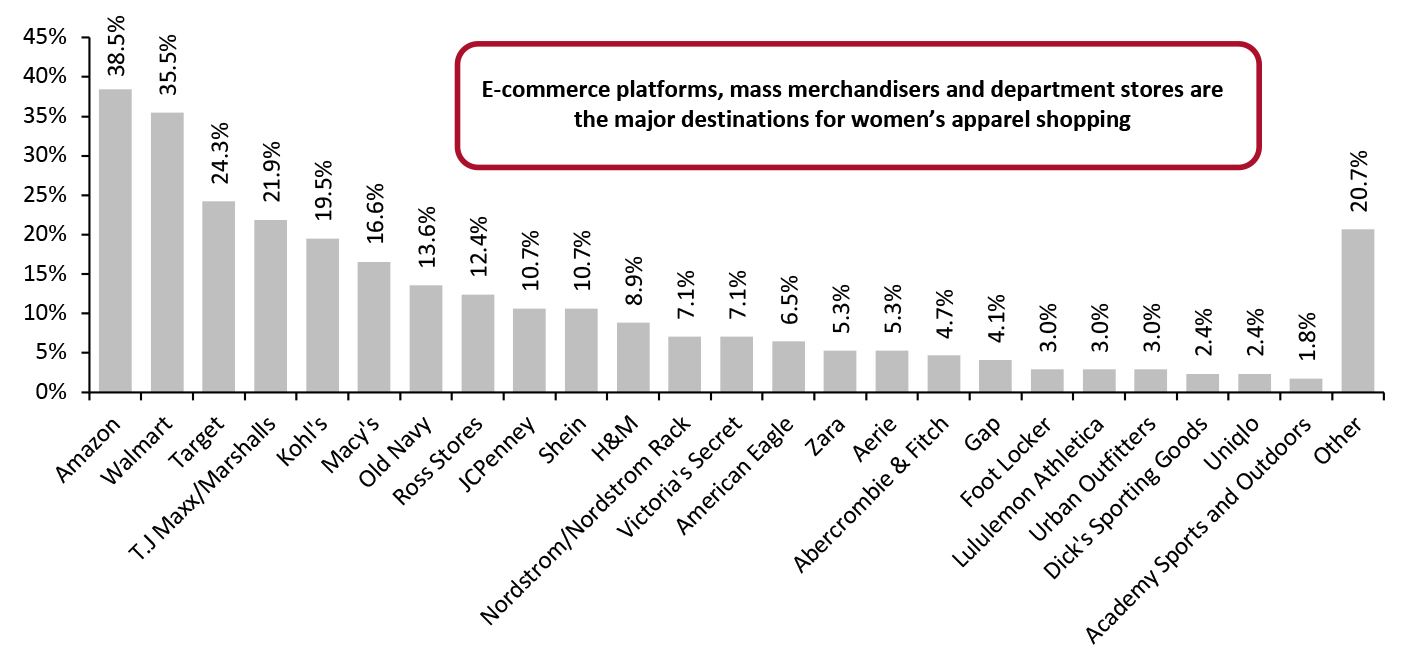

Amazon, Walmart, and Target are the top three retailers US female shoppers bought clothing or apparel accessories from in the past three months ended May 3, 2022, according to Coresight Research survey data.

Our findings indicate that compared to specialty retailers such as American Eagle and Gap, e-commerce platforms, mass merchandisers and department stores are major destinations for female consumers’ apparel shopping—mainly due to larger product assortments, more convenient services such as buy online, pick up in-store (BOPIS), fast delivery and easy inventory requests, according to our analysis.

Source: Euromonitor International Limited 2022 © All rights reserved[/caption]

Where Consumers Are Shopping and What They Are Buying

Amazon, Walmart, and Target are the top three retailers US female shoppers bought clothing or apparel accessories from in the past three months ended May 3, 2022, according to Coresight Research survey data.

Our findings indicate that compared to specialty retailers such as American Eagle and Gap, e-commerce platforms, mass merchandisers and department stores are major destinations for female consumers’ apparel shopping—mainly due to larger product assortments, more convenient services such as buy online, pick up in-store (BOPIS), fast delivery and easy inventory requests, according to our analysis.

Figure 7. Female Respondents Who Purchased Clothing or Apparel Accessories in The Past Three Months: Retailers That Consumers Purchased from, (%), May 2022 [caption id="attachment_150199" align="aligncenter" width="700"]

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022 Source: Coresight Research [/caption]

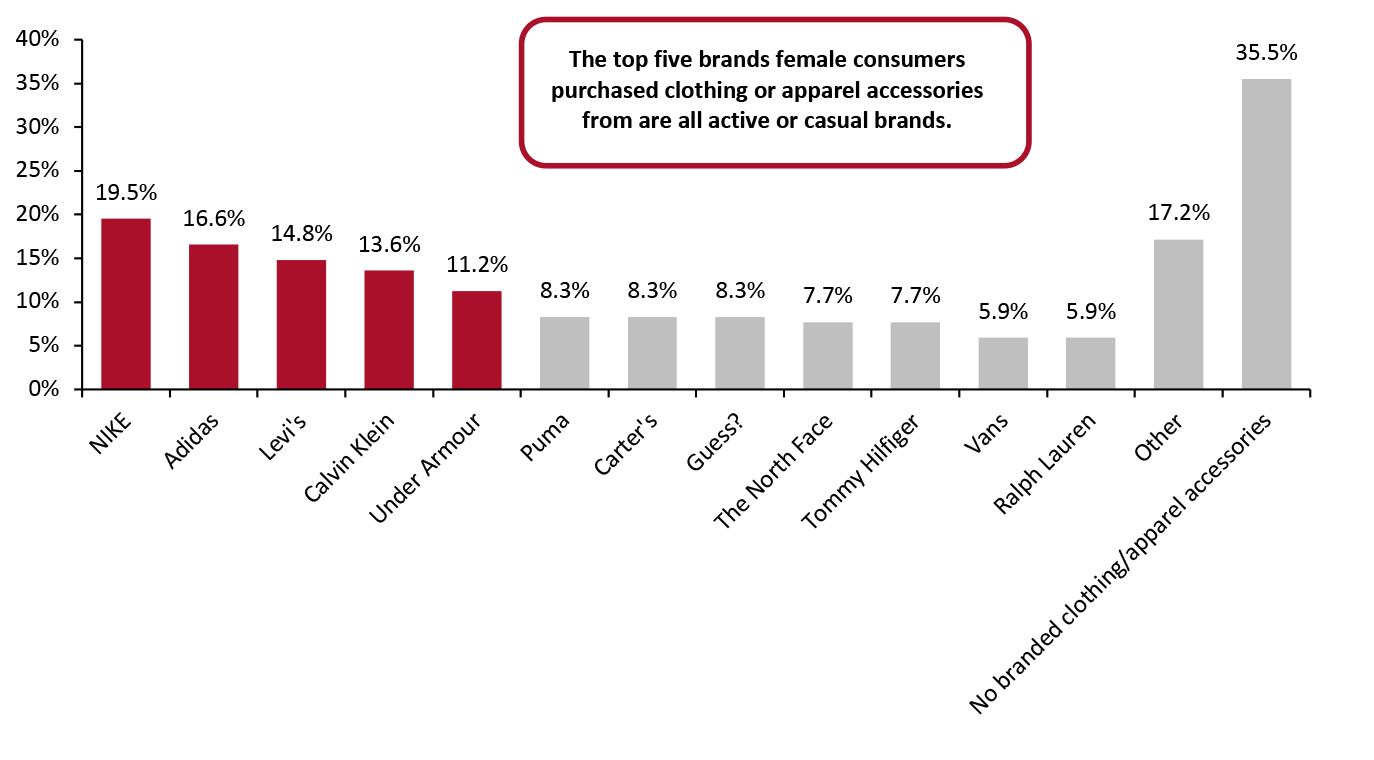

By brand, NIKE, adidas, and Levi’s are the top three brands that US female shoppers bought clothing or apparel accessories from in the last three months, ended May 3, 2022, followed by Calvin Klein, Under Armour, and Puma, according to our survey. No occasion wear brands pop up on the top five of the list, and we believe there is potential bias existing in the survey results due to a mix of reasons including small sample size, occasion wear’s low wardrobe refreshment frequency and seasonality. We also found that a significant portion (35.5%) of female consumers had not bought branded clothing or apparel accessories.

Figure 8. Female Respondents Who Purchased Clothing or Apparel Accessories in The Past Three Months: Brands That Consumers Purchased from, (%), May 2022 [caption id="attachment_150201" align="aligncenter" width="700"]

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022 Source: Coresight Research [/caption]

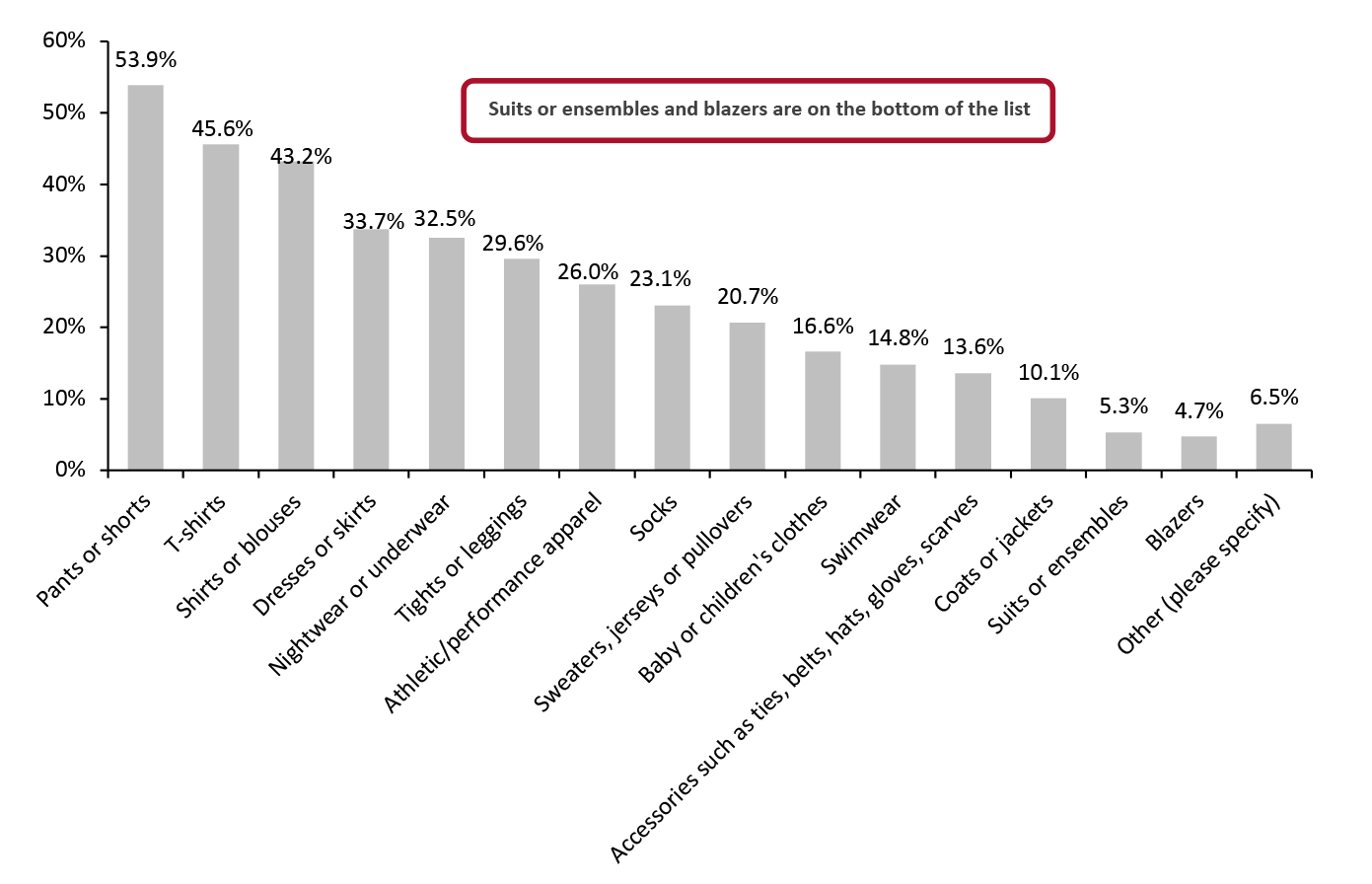

By categories, pants or shorts, T-shirts and shirts or blouses are the top three clothing or apparel accessories categories US female shoppers bought in the past three months ended May 3, 2022, according to our survey. Although dresswear categories such as suits or ensembles and blazers are on the bottom of the list, we believe these categories are recovering fast in 2022.

Figure 9. Female Respondents Who Purchased Clothing or Apparel Accessories in The Past Three Months: Categories That Consumers Purchased (%) May 2022 [caption id="attachment_150202" align="aligncenter" width="700"]

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022

Base: 169 US female consumers aged 18+ who purchased clothing or apparel accessories in the past three months ended May 3, 2022 Source: Coresight Research [/caption]

Themes We Are Watching

Outperformance in Luxury Apparel and Footwear

We are seeing outperformance in high-end apparel and footwear, while retailers targeting consumers on modest incomes have tended to report weakened demand amid soaring inflation for essentials. We expect to see continued strong demand in luxury women’s apparel and footwear. Companies such as Capri Holdings, Hermès, Kering, Nordstrom and Ralph Lauren have reported strong apparel and footwear sales growth. The outperformance of high-end womenswear will have a relatively limited uplift effect on the total market: Luxury women’s clothing and footwear accounted for around 9.8% of total US women’s clothing and footwear sales, by value, in 2021, according to our analysis of Euromonitor data.

In the mass market, some price-sensitive consumers are cutting discretionary spending as high inflation persists in essentials such as groceries and gasoline. In May 2022, for instance, Ross Stores reported that discretionary spending for the lower-income customer is being squeezed. Kohl’s, which is positioned as a middle to value market player, reported in May 2022 that it is seeing average spend per transaction and units per transaction decline.

Figure 10. Performance of Apparel and Footwear Reported by Selected High-End Brands and Retailers [wpdatatable id=2080]

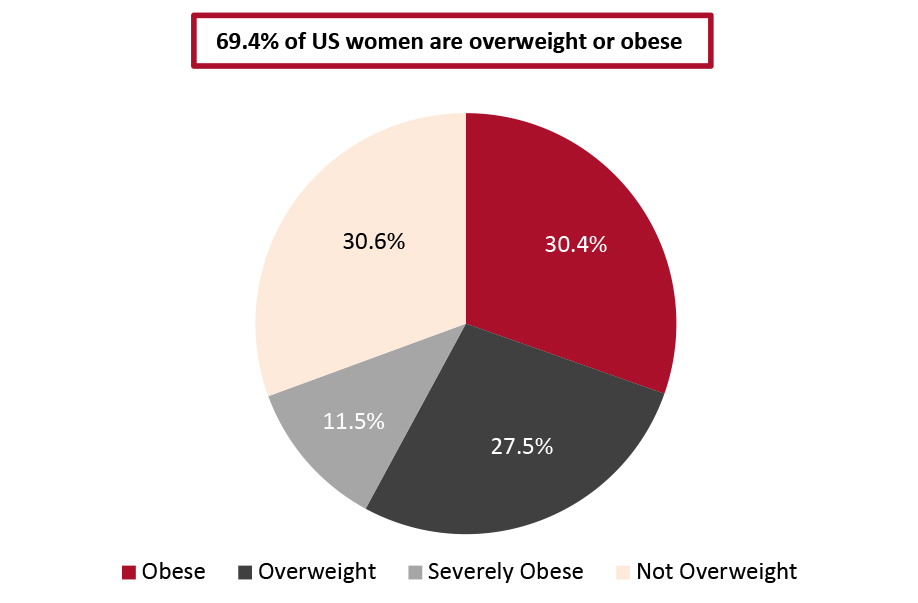

Source: Company reports Women’s Plus-Size Market Size inclusivity is no longer a buzzword but a consumer need. The proportion of US adults that are overweight has been increasing in recent years, according to the Centers for Disease Control and Prevention. Approximately 69.4% of the 131 million women in the US are overweight or obese, according to the organization’s latest estimates in 2018 (see Figure 8). This highlights the tremendous opportunity for brands and retailers to provide extended sizes in the women’s apparel market. More brands and retailers are entering the market or broadening their offerings to take advantage of the plus-size opportunity. For instance, in May 2022, the Los Angeles-based brand Miaou enlisted model Paloma Elsesser to develop a new plus-size collection. Retailers such as JCPenney and Target continue to launch plus-size collections. We estimate that the US women’s plus-size apparel market grew from $28.3 billion in 2020 to $34.3 billion in 2021, representing a year-over-year increase of 21.2%. We expect that in 2022, the market will experience more moderate growth of around 7.6%. However, we expect the plus-size market to increase at a faster rate than the total women’s apparel market and thus gain share of the total market.

Figure 11. US Women: Classification by Body Mass Index, 2017-2018* (% of Population) [caption id="attachment_150203" align="aligncenter" width="700"]

*Latest available data

*Latest available data “Overweight” is a body mass index (BMI) of 25.0–29.9 kg/m2; “obesity” is a BMI of 30.0 kg/m2 or above; “severe obesity” is a BMI of 40.0 kg/m2 or above. Pregnant women are excluded from the analysis.

Source: Centers for Disease Control and Prevention [/caption]

Growth of Niche Categories Including Maternity and Adaptive Segments

We expect to see more innovations in growing niche categories including maternity and adaptive categories in the womenswear market. Victoria’s Secret reported on its fourth-quarter earnings call of fiscal year 2021 dated March 3, 2022 that it launched a maternity bra in February 2022 and it sold 100,000 units within its first week, highlighting the growth potential of the market.

Coresight Research estimates that the potential market for adaptive apparel is nearly 50 times greater than the current state of supply. In 2021, we estimate that adaptive apparel spending totaled $1.3 billion, while the potential addressable market was worth $64.3 billion. We expect that consumer spending on adaptive apparel will grow at a faster rate than overall spending on apparel in 2022. This strong growth is anticipated due to the following factors: untapped demand—disabled people seeking entirely new product categories; new brands and retailers entering this space; advances and innovations in fit technology, materials and digital design; and increasing employment opportunities for disabled people, which will increase both spending power and demand for adaptive apparel products.

We are already seeing brands and retailers launching adaptive apparel to suit consumer demand. For instance, on May 23, 2022, Reebok launched its first adaptive footwear collection, called Fit to Fit. The collection features two sneakers that are designed for easy entry and exit for people with disabilities. The shapewear brand Skims launched adaptive collection for customers with limited mobility, on April 29, 2022. Major brands and retailers are launching adaptive brand extensions—including Kohl’s, Target and Tommy Hilfiger.

What We Think

We continue to see growth momentum in the US womenswear market in 2022 and we are seeing consumers shifting away from the popular pandemic categories, such as casual and activewear, toward more occasion-based apparel. Although activewear and casual wear continue to capture a larger share of the US womenswear market and top the female consumer’s shopping list, according to our survey on May 3, 2022, we believe that occasion wear is seeing strong recovery in 2022. We recommend apparel brand and retailers provide relevant product options in 2022 to suit consumer demand. In the long term, we still believe that the casualization trend will likely stay, as many consumers will continue to work remotely or will dress more casually onsite.

Implications for Brands/Retailers

- With the shift in consumer emphasis toward occasion wear, we recommend womenswear brands and retailers adapt their category focus to stay relevant.

- We are seeing an outperformance in high-end apparel and footwear, while companies targeting more value-conscious consumers appear to be increasingly vulnerable to volume declines. We are seeing companies such as Kering expanding luxury product offerings to capture strong consumer demand. We expect to see continued demand for luxury products in the womenswear market, but we expect the outperformance of the high-end segment to have a limited uplift effect on the total market.

- We also see opportunities in the women’s plus-size market. We recommend brands and retailers broaden their apparel size offerings to take advantage of the plus-size opportunity.

Source for all Euromonitor data: Euromonitor International Limited 2022 © All rights reserved