DIpil Das

What’s the Story?

This report presents the results of Coresight Research’s latest weekly survey of US consumers on the coronavirus outbreak, undertaken on August 12, 2020. We explore the trends we are seeing from week to week, following prior surveys on August 5, July 29, July 22, July 15, July 8, July 1, June 24, June 17, June 10, June 3, May 27, May 20, May 13, May 6, April 29, April 22, April 15, April 8, April 1, March 25 and March 17–18.Holiday Season Shopping

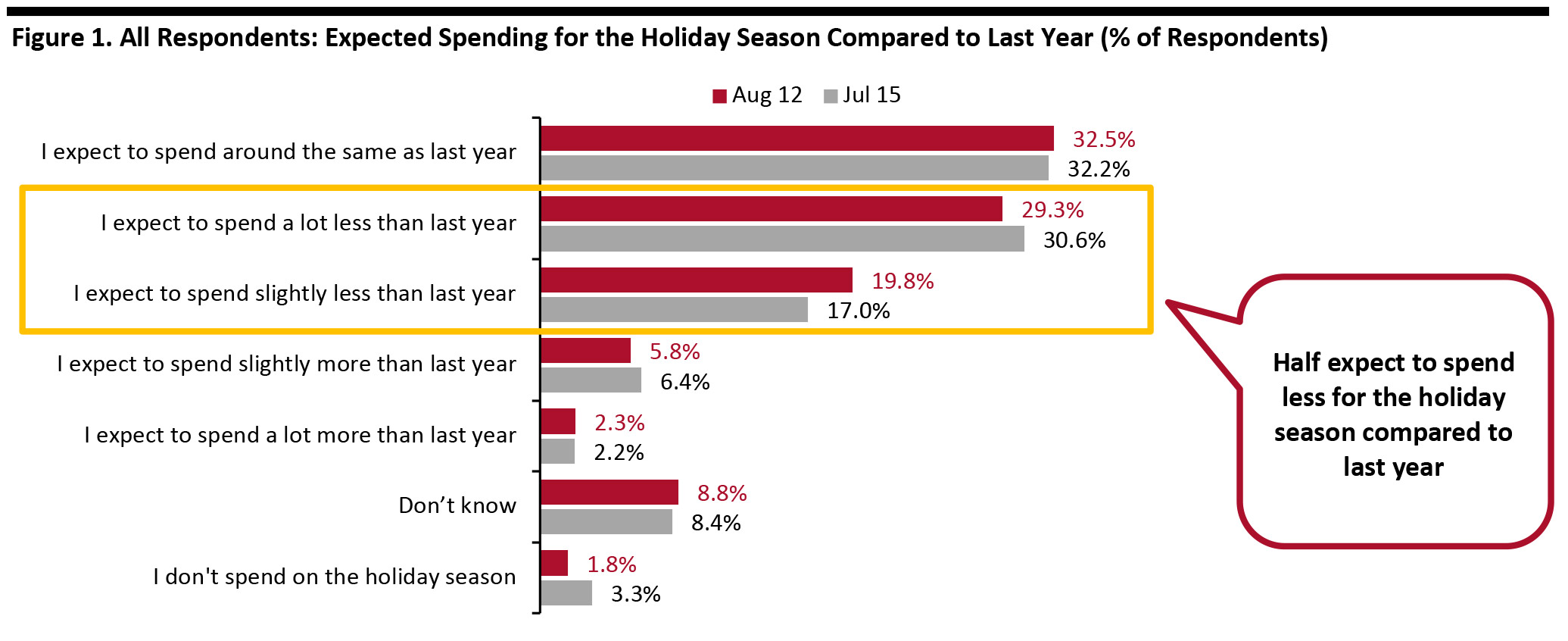

This week, we asked consumers again about their expected shopping behaviors for the holiday season 2020 and compare the results with our findings from when we asked four weeks ago, on July 15. We asked respondents:- About their expected overall holiday season spending—including gifts and expenses related to traveling and dining out—this year compared to 2019.

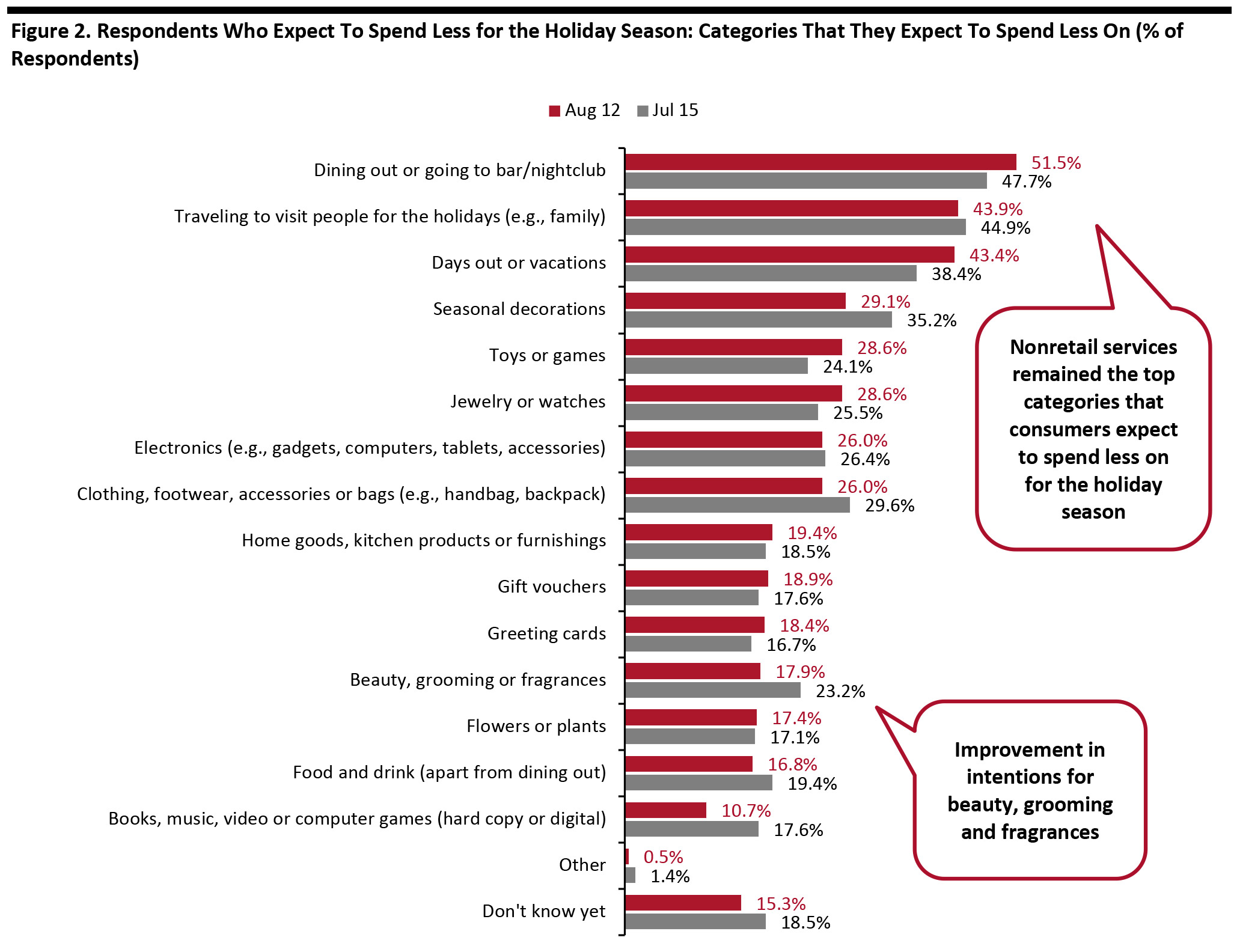

- For those who expect to spend less this holiday season, what categories they plan to spend less on—from 15 options (as well as “other” and “don’t know”).

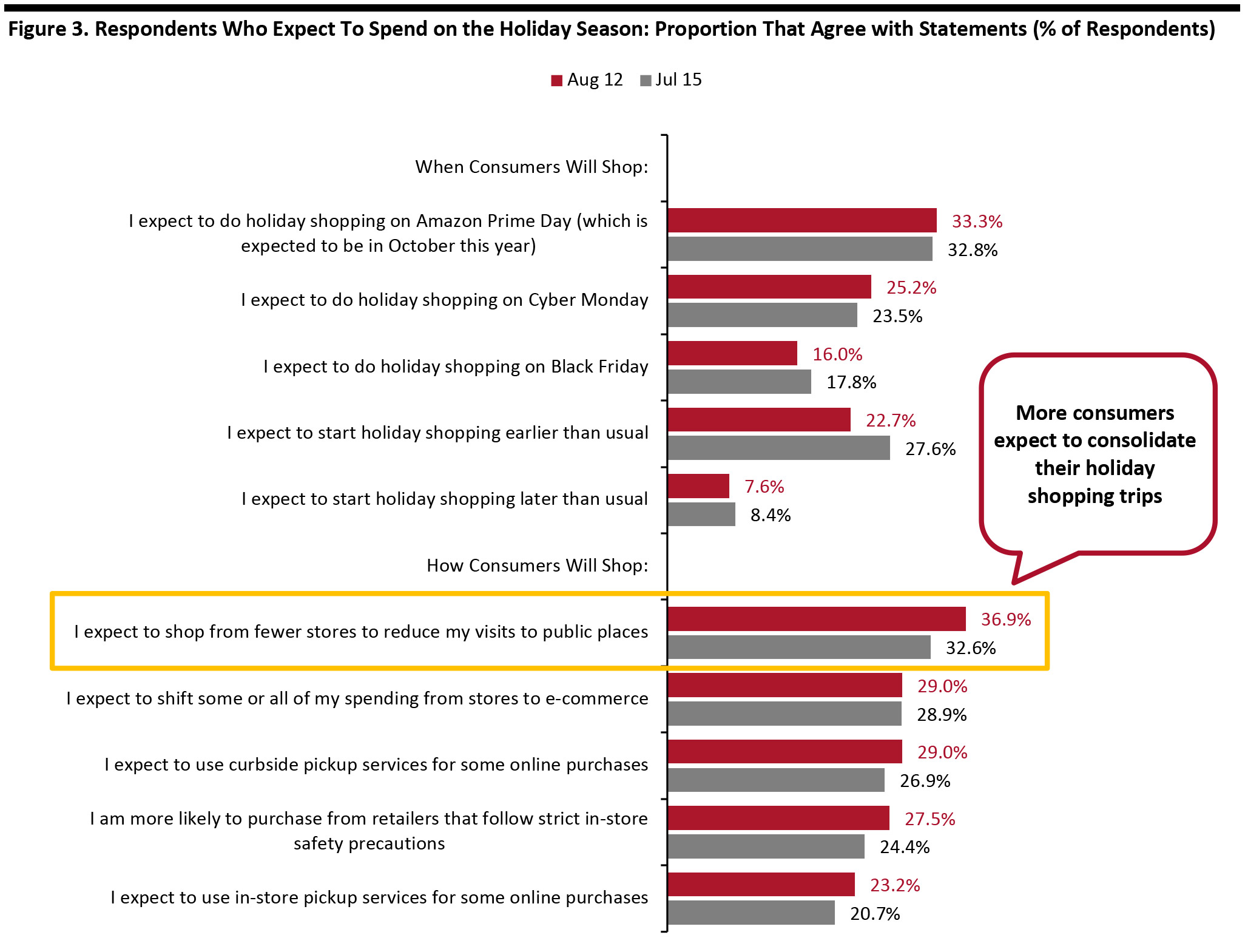

- Whether they agreed with any or all of 10 attitudinal and behavioral statements related to holiday-season shopping.

Base: US Internet users aged 18+

Base: US Internet users aged 18+ Source: Coresight Research [/caption] For those who expect to spend less for the holiday season, around half of the 15 options saw increases in consumer expectations to spend less:

- Nonretail services remained the top categories in which consumers plan to spend less—more than half said they will spend less on dining out or going to bars/nightclubs, versus 47.7% who expected to spend less on such activities a month ago. The proportion of consumers that expect to spend less on vacations jumped by five percentage points, to 43.4% from 38.4% a month ago.

- Cuts in retail categories are mixed. Seasonal decorations again ranked the top product category that consumers plan to spend less on for holiday 2020—around three in 10 said that they expect to cut their spending on such products, but we saw a six-percentage-point decline compared to the proportion from a month ago. Toys or games took the second place from clothing and footwear this time, with 28.6% expecting to spend less on toys. Beauty/fragrance products recorded a decrease in consumers’ expectation to spend less—some 17.9% expect to spend less on beauty/fragrance than they did for holiday 2019.

- We asked respondents to think about their retail spending overall—so cutbacks in retail categories will reflect not just shoppers cutting gift spending but the effects of Covid-19 restrictions on retail purchases that are driven by parties, dinners, other gatherings and getaways.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+ who expect to spend less on the 2020 holiday season than they did last year

Source: Coresight Research [/caption] Holiday Sales Calendar Distorted by Prime Day and Covid-19 Our findings again confirmed that there will be a shift in the holiday spending timeline this year:

- The proportion of holiday shoppers that expect to shop on Amazon Prime Day remained stable at around one-third.

- Recent announcements by major retailers to keep stores closed on Thanksgiving and Amazon’s postponement of Prime Day to early October are expected to pull holiday sales forward. The role of in-store sales that traditionally kick off holiday shopping on Thanksgiving will be less important this year. While retailers have not yet announced plans for Black Friday, only 16.0% of respondents said they will do holiday shopping on that day, slightly less than the 17.8% from a month ago. One-quarter expect to do holiday shopping on Cyber Monday, versus 23.5% a month ago.

- Some 22.7% plan to start holiday shopping earlier this year, slightly down from 27.6% a month ago. Only 7.6% expect to start later than usual.

- Some 36.9% expect to shop from fewer stores to reduce their trips to public spaces, up four percentage points from around one-third a month ago. The consolidation of shopping trips could translate to higher sales and traffic for retailers that offer a wide range of product categories and brands, such as mass merchants and warehouse clubs.

- The proportion of consumers that plan to switch some or all of their holiday spending from stores to e-commerce this year remained stable at around three in 10. This figure is also roughly in line with the proportion that expect to shop more online in the long term (which we discuss later in this report).

- We saw more consumers expect to embrace contact-light options for holiday shopping: Almost three in 10 expect to use curbside pickup services for some of their online purchases, versus 26.9% a month ago; some 23.2% plan to use in-store pickup services, compared to one-fifth a month ago.

- Safety measures implemented by retailers are a must-have for consumers’ in-store shopping: Some 27.5% holiday shoppers are more likely to purchase from retailers that follow strict in-store safety precautions, versus 24.4% a month ago.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+ who expect to spend on the holiday season

Source: Coresight Research [/caption]

What Shoppers Are Doing and Where They Are Going

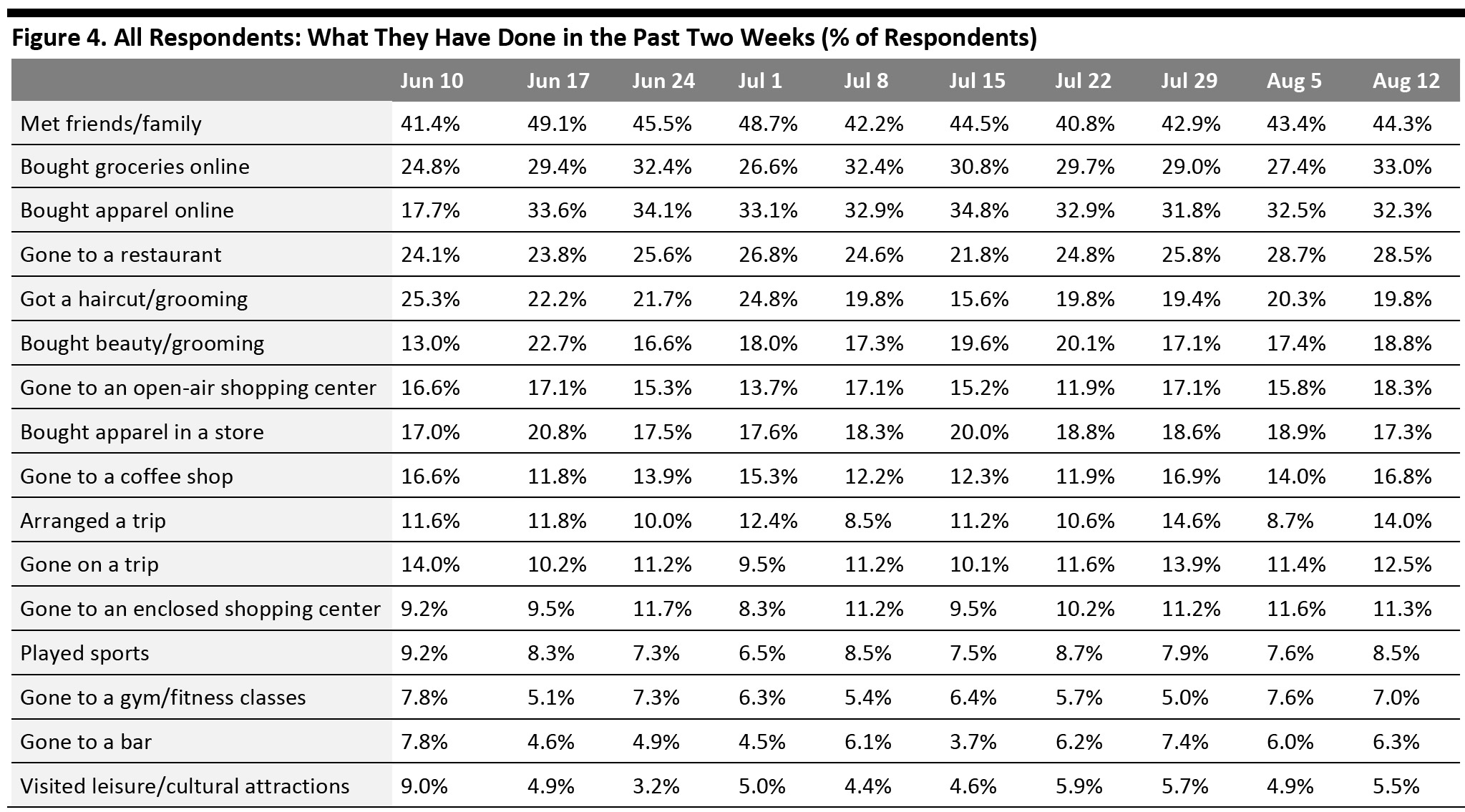

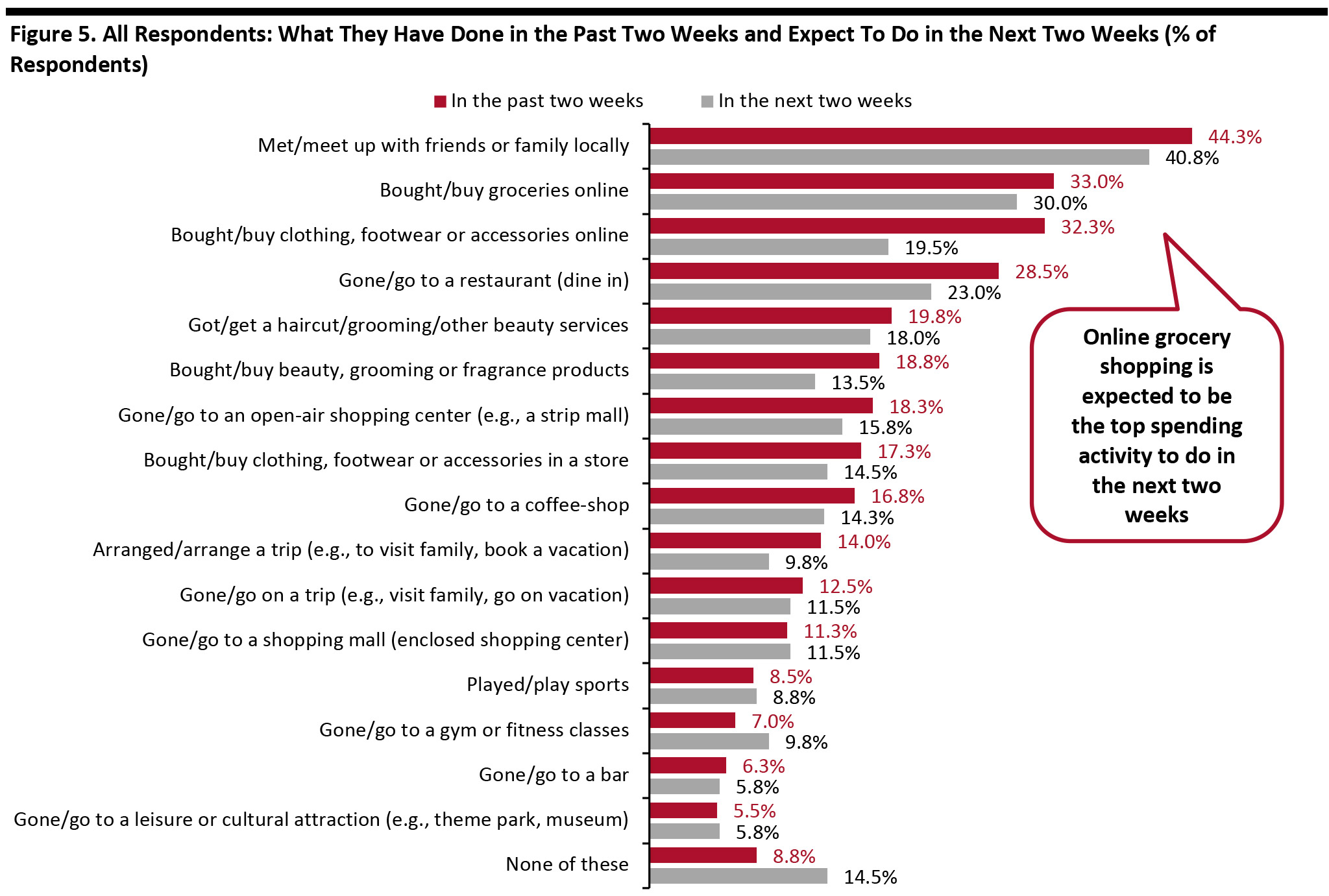

Online Grocery Shopping Becomes the Top Spending Activity in the Past Two Weeks Each week, we ask consumers what they have done in the past two weeks. This week, the proportions of respondents increased for half of the 16 options we provided for activities done recently—although most were within the margin of error. Online continues to overtake in-store as the top shopping activities to do in the past two weeks. This aligns with findings elsewhere in our survey that online shopping has spiked again.- The proportion of respondents that had bought apparel online in the past two weeks remained consistent at around one-third this week. Some 17.3% had bought apparel in a store, versus 18.9% last week (a change that is not statistically significant).

- The proportion of respondents that had bought groceries online bounced back after gradual declines in the past couple of weeks, which is in line with the later finding in our survey that a higher proportion of consumers are buying more food online than before the pandemic. This week, one-third had done so, up almost six percentages points from last week and reaching the highest level since we started asking the question.

- The proportion of respondents that had visited an open-air shopping center has been fluctuating in the past few weeks. Some 18.3% had visited this type of public place this week—the highest level we have seen in two months. However, the rate is still low as consumers continue to avoid shopping malls/centers (discussed later in the report). The proportion of consumers that visited an enclosed shopping mall broadly leveled off at 11% this week.

- We saw the proportion of respondents that had gone to restaurants in the past two weeks remain stable at three in 10 this week. More consumers had gone to a coffee shop—one in six compared to one in seven last week.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption] Expectations To Go to Food-Service Locations in the Next Two Weeks Fall Each week, we ask consumers what they expect to do in the next two weeks, with a comparable set of options to those for the last two weeks. In the chart below, we compare these short-term expectations with recent actual behavior. We saw slightly lower proportions of consumers expecting to do almost all activities in the next two weeks than actual behavior in the past two weeks.

- Online grocery shopping is expected to be the number-one spending activity in the next two weeks, with three in 10 planning to do so, only slightly lower than the actual behavior of such activity in the last two weeks.

- One-fifth expect to buy clothing or footwear online in the next two weeks, and 14.5% plan to do so in a store. Only 13.5% expect to purchase beauty products. From our past observations, the proportions in these discretionary spending options are typically lower than the actual behaviors, as consumers may not plan these activities in advance.

- Some 23.0% expect to dine in a restaurant in the next two weeks, and only one in seven plan to go to a coffee shop. The low expectation in going to food-service locations is aligned with the jump in consumers’ avoidance of restaurants/bars/coffee shops, which we discuss in the next section of this report.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

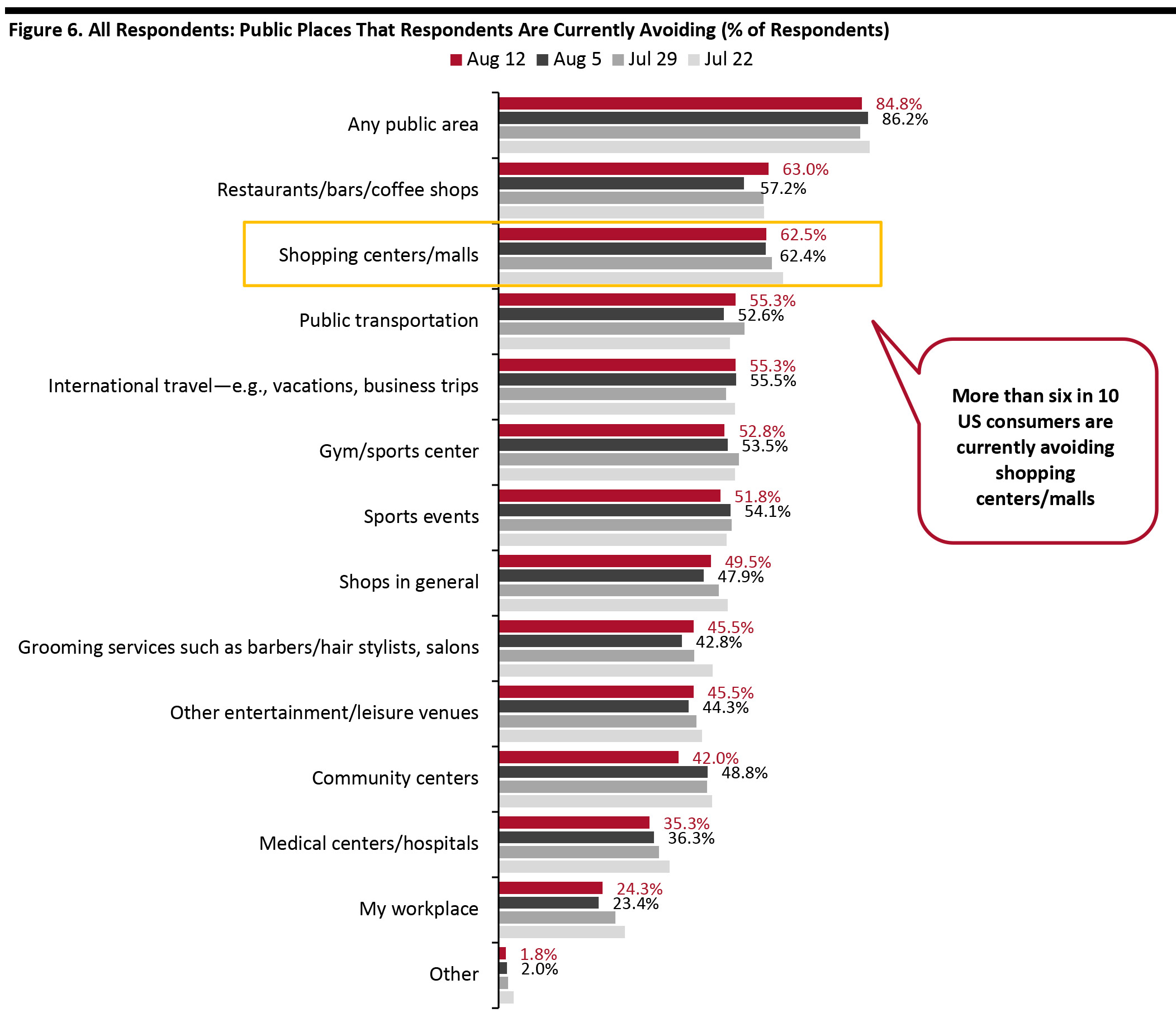

Source: Coresight Research [/caption] Over Four-Fifths Are Currently Avoiding Public Places This week, the proportion of respondents saying that they are avoiding any type of public area decreased very slightly to 84.8%, from 86.2% last week. However, this is the fifth consecutive week that the avoidance rate has been above 80%. We saw slight increases in avoidance for around half of the 12 options provided, although most of the changes were within the margin of error:

- The proportion of respondents that are currently avoiding shopping centers/malls remained stable this week, after reaching a peak of two-thirds three weeks ago. Some 62.5% said that they are currently avoiding these places; the rate has remained high at above 60% for a month now.

- The proportion of respondents that are currently avoiding food-service locations jumped to the highest level that we have seen in months, and this type of public place is now the most-avoided place among consumers. Some 63.0% are currently avoiding restaurants/bars/coffee shops, up six percentage points from 57.2% last week.

- Community centers saw the highest decline in avoidance rate this week, of seven percentage points: Some 42.0% of respondents are currently avoiding these places, versus almost half last week.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption]

Reviewing Trend Data in Current Purchasing Behavior

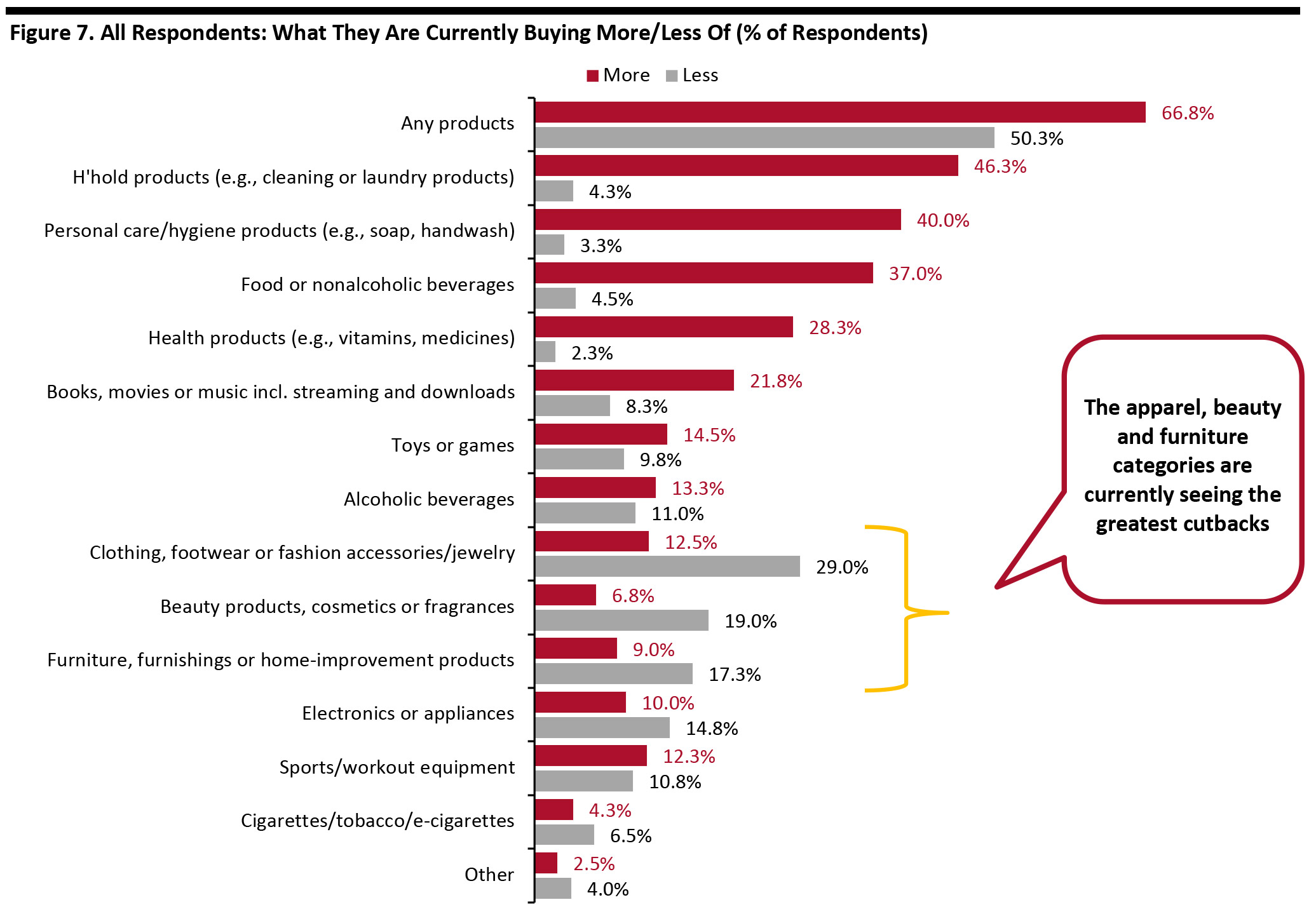

What Consumers Are Currently Buying More Of and Less Of The proportion of respondents that are currently buying more of any category stayed consistent at 66.8% this week, while the proportion of respondents that are currently buying less fell slightly. Half of consumers are currently buying less, versus 51.7% last week.- Buying more of certain categories and buying less of certain categories were not mutually exclusive options, so respondents could answer yes to both.

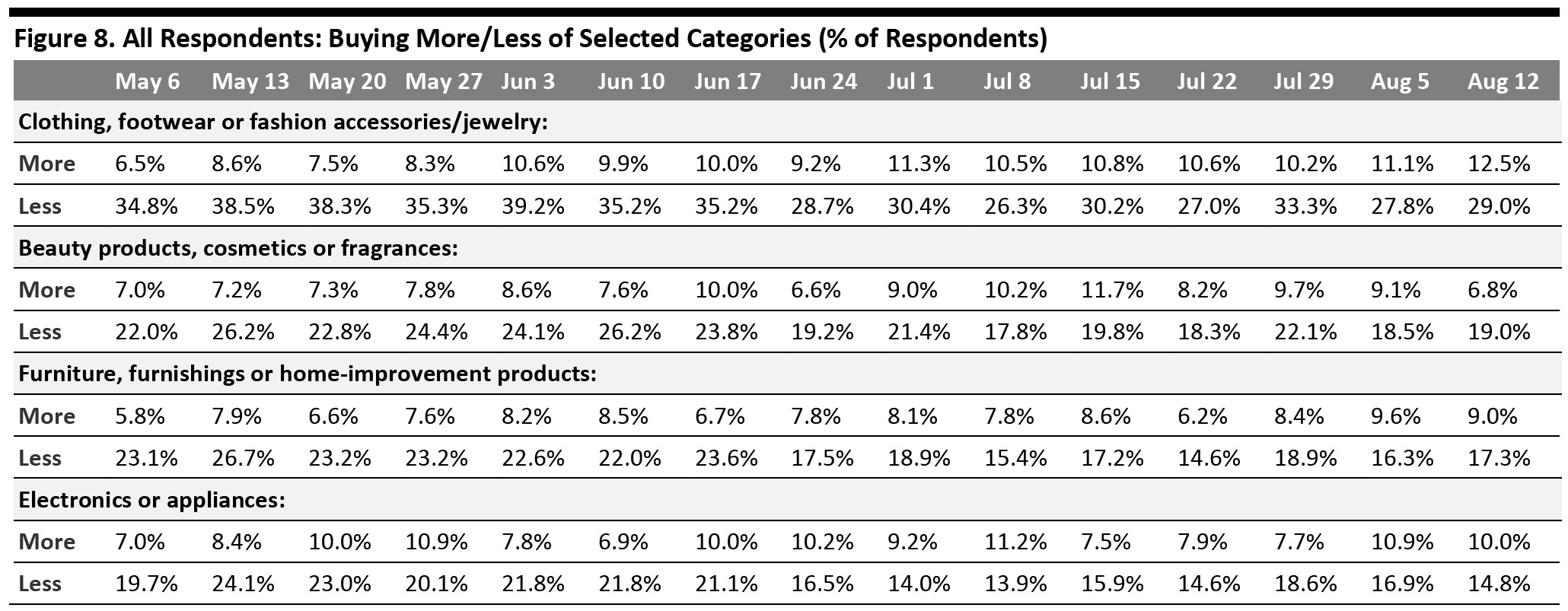

- The ratio for apparel decreased to 2.3 from 2.5 last week and 3.3 two weeks before. Encouragingly, this is the lowest ratio since we started asking the question back in March.

- The ratio for electronics dropped to 1.5 from 1.6 last week and 2.4 two weeks before.

- The ratio for beauty stood at 2.8, versus 2.0 last week. This is also the first time when the ratio of less to more for beauty is higher than that for apparel.

- The ratio for home raised to 1.9 this week, after reaching its lowest ratio of 1.7 last week.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption] [caption id="attachment_114480" align="aligncenter" width="700"]

Base: US Internet users aged 18+

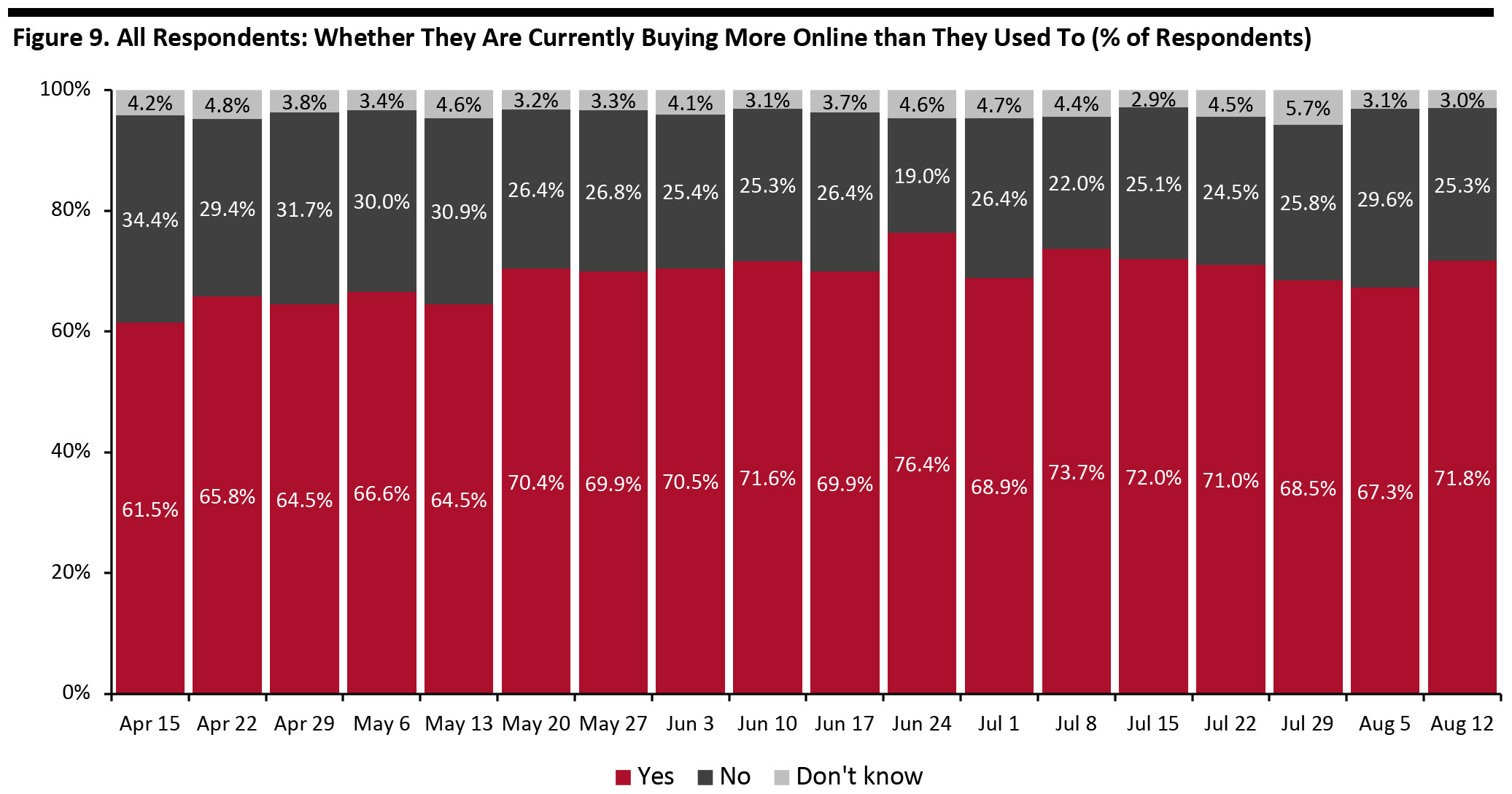

Base: US Internet users aged 18+ Source: Coresight Research [/caption] Seven in 10 Are Switching Spending Online This week, we saw the proportion of consumers buying more online than they used to rebound to above 70% after weeks of a declining trend. Some 71.8% of consumers stated that they are buying more online than they used to this week, up almost five percentage points from 67.3% last week. However, this is still lower than the peak of 76.4% from June 24. [caption id="attachment_114481" align="aligncenter" width="700"]

Base: US Internet users aged 18+

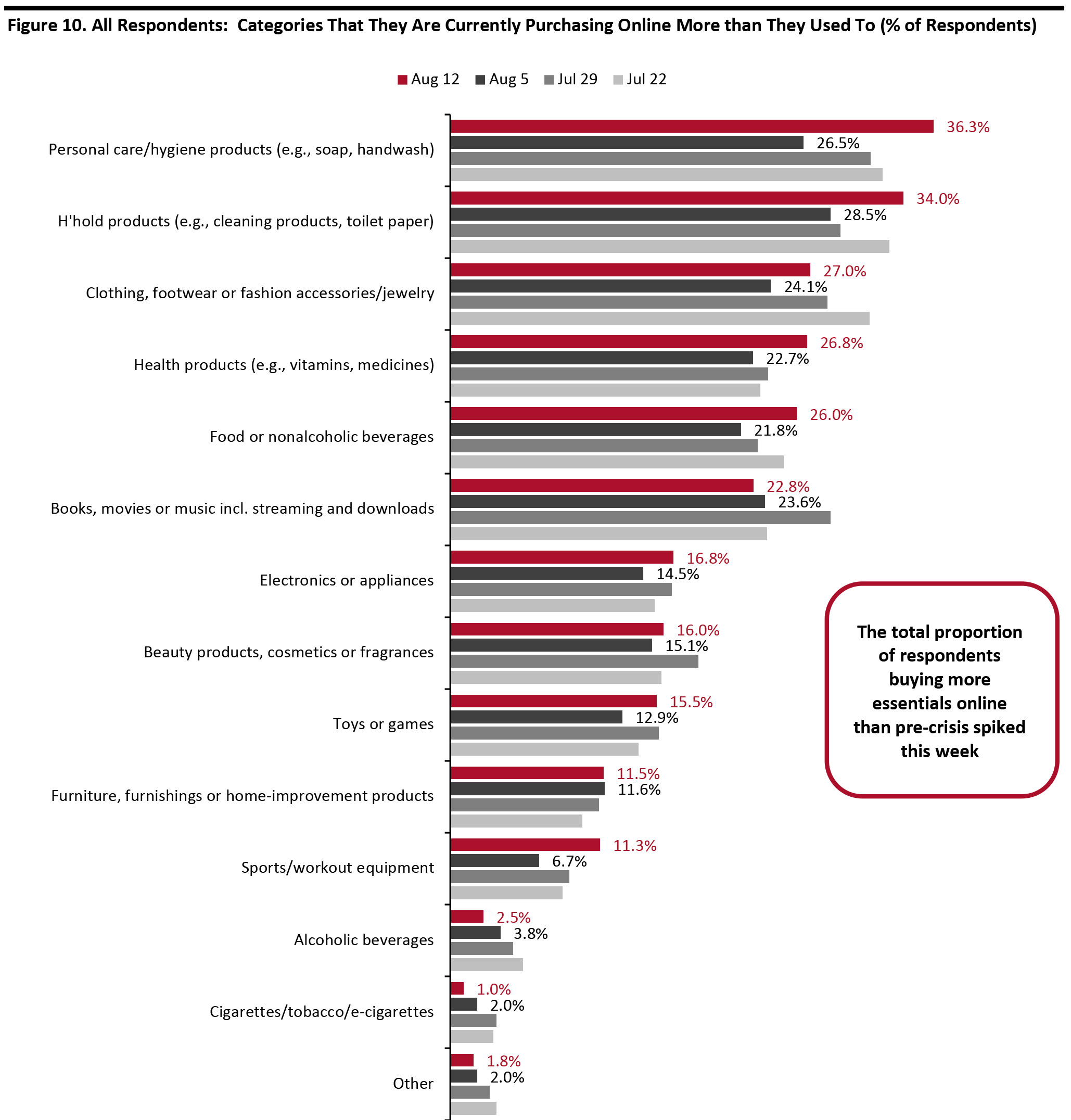

Base: US Internet users aged 18+ Source: Coresight Research [/caption] What Consumers Are Currently Buying More Of Online This week, we saw increases in the proportions of consumers that are currently buying more online than they used to in eight out of the 13 categories, driven by purchases of essential products. Personal care saw the largest surge, of 10 percentage points, after a decline last week, with 36.3% saying they are currently buying more online. Household products saw an almost six-percentage-point upswing this week. Echoing our previous finding that more consumers had shopped grocery online in the past two weeks, we saw over one-quarter of respondents buying more food online, up from 21.8% last week. The proportion of consumers that are currently buying more apparel online also went up this week, to 27.0% from 24.1% last week, and remained the third-most-purchased category online this week. One in six are currently buying more electronics online than they used to, versus one in seven last week. The proportion of respondents that are currently buying more beauty products online remained fairly stable at around 16.0% this week. [caption id="attachment_114482" align="aligncenter" width="700"]

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

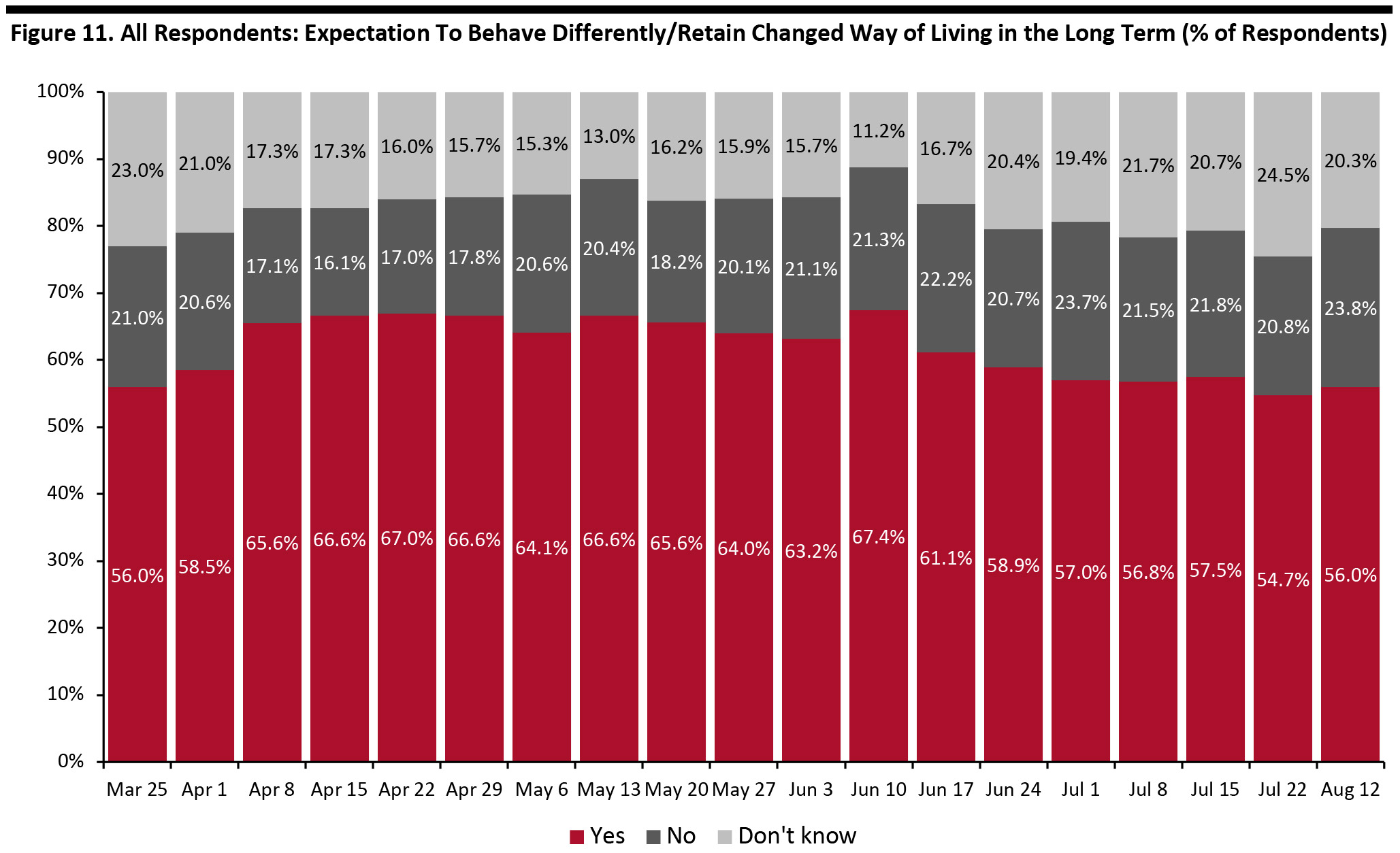

Source: Coresight Research [/caption] Fewer than Six in 10 Expect To Retain Changed Behaviors over the Long Term We ask respondents whether they think they will keep some of the behaviors they have adopted during the coronavirus crisis in the long term. This week, the proportion of respondents expecting to retain some changed behaviors came at 56.0%, versus 54.7% three weeks ago. This level is also very close to the plateau of around 57% that we saw in the first few weeks of July. [caption id="attachment_114483" align="aligncenter" width="700"]

Question not asked on July 29 or August 5

Question not asked on July 29 or August 5 Base: US Internet users aged 18+

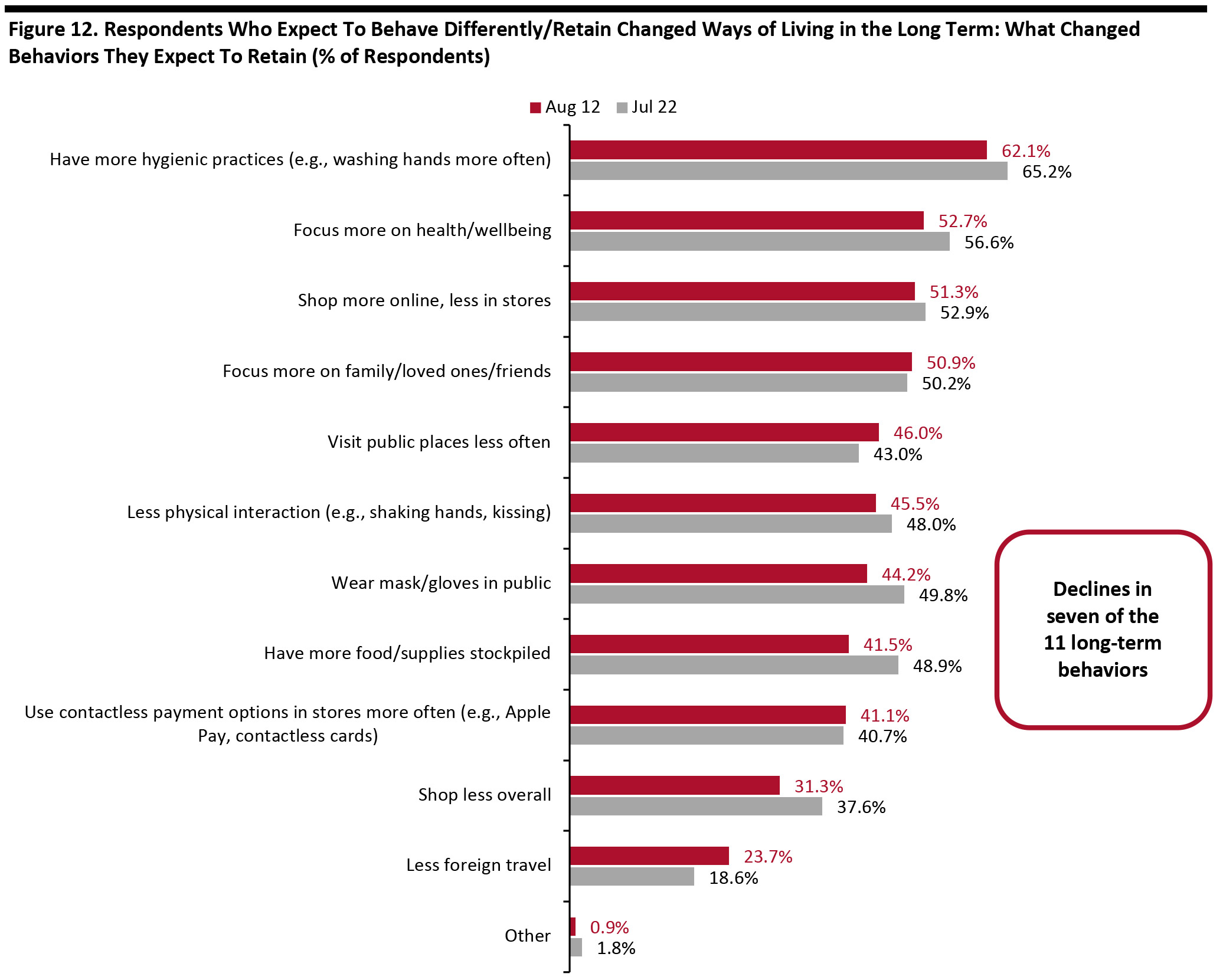

Source: Coresight Research [/caption] Among those expecting to retain changed behaviors, we saw declines in the proportions of respondents selecting seven of the 11 behavior options we provided, compared to three weeks earlier. The proportion of consumers expecting to have more food/supplies stockpiled in the long term saw the largest drop, down seven percentage points to 41.5% from almost half three weeks ago. Wearing masks/gloves in public is one of the few behaviors that experienced an increase in the proportion of respondents from three weeks before, with 46.0% expecting to retain this behavior in the long term, compared to 43.0% on July 22. The proportion of respondents expecting to use contactless payment options in stores more often than they did previously remained stable at around 41% this week. [caption id="attachment_114484" align="aligncenter" width="700"]

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+ who expect to behave differently in the long term/retain changed ways of living from the outbreak

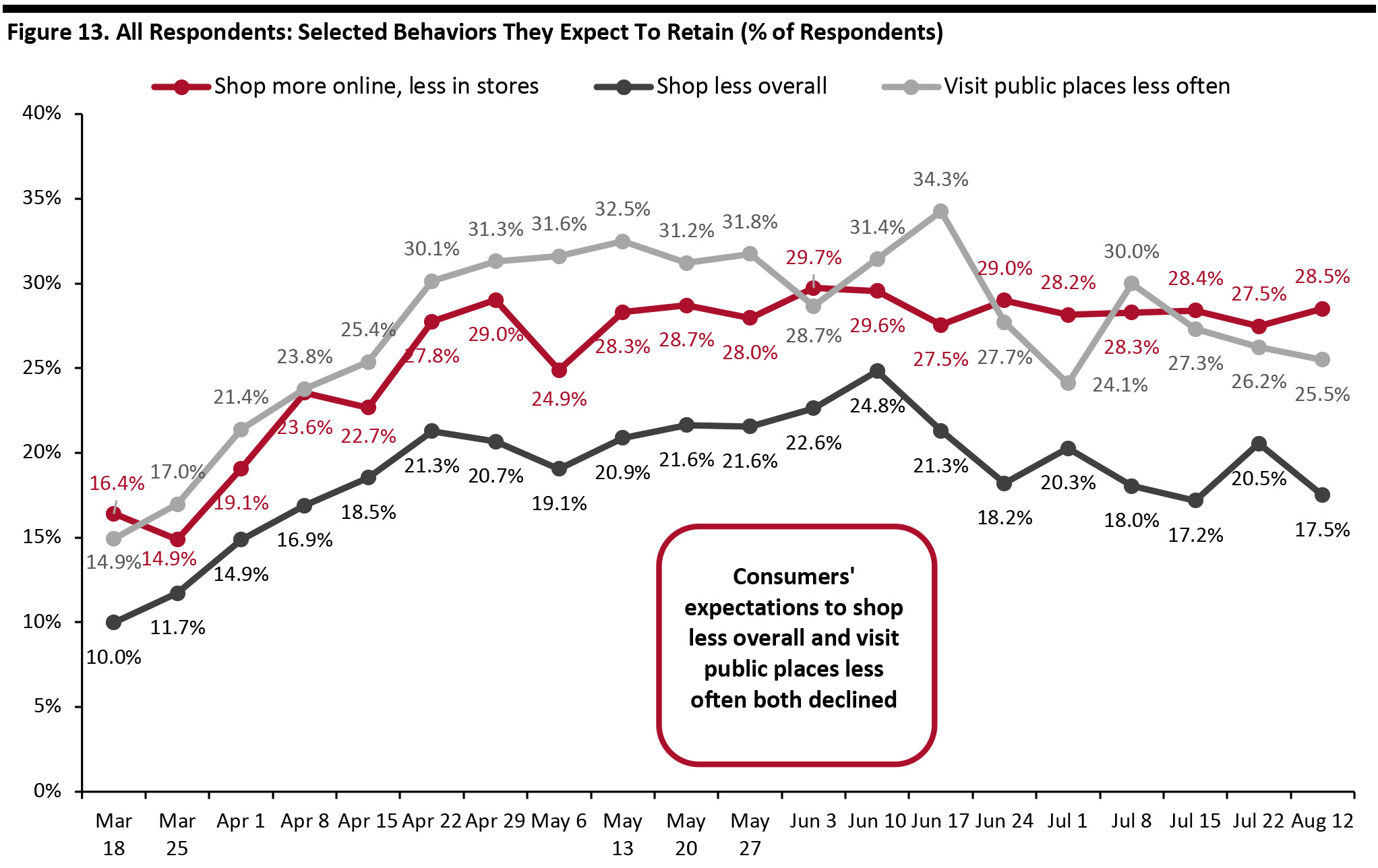

Source: Coresight Research [/caption] In the chart below, we show trended data in three of the metrics charted above. We represent these as a proportion of all respondents, to represent consumers overall, rather than as a proportion of those expecting to retain changed behaviors (which is what is charted above). Rebased to all respondents, the proportion that expect to visit public places less often and shop less overall in the long term both decreased compared to three weeks ago, despite the current high avoidance rate of any public places. Both metrics look to be past their peak:

- Consumers who plan to visit public places less often fell to one-quarter this week, compared the peak of 34.3% in the week of June 17.

- The proportion of respondents that expect to shop less overall slid from a June 10 peak of one-fifth to 17.5% this week.

Question not asked on July 29 or August 5

Question not asked on July 29 or August 5 Base: US Internet users aged 18+

Source: Coresight Research [/caption]

What We Think

Implications for Brands and Retailers Our survey results show that, compared to a month ago, more consumers expect to spend less for the holiday 2020 season than they did last year, and they expect to begin their holiday shopping as early as October—when Prime Day will likely to take place.- The delay of Prime Day until early October could push big-box retailers to offer similar deals at around that time. With less than two months to go until October, they should start planning such promotions to compete with Amazon: Some retailers, such as Best Buy, have announced that they will offer better deals for consumers than they have in previous years.

- Our survey reflects that consumers’ safety concerns around in-store shopping remain high. Brands and retailers should think about whether to open or close their stores on Thanksgiving. We have seen a growing list of major retailers—including Best Buy, Kohl’s, Target and Walmart—deciding to shut their doors on Thanksgiving to avoid the risk of overcrowding amid the pandemic. Retailers should also determine their store plans for Black Friday, which could include limited store hours and capacity, as well as providing additional fulfillment options such as in-store pickup and curbside pickup to ensure safety for employees and consumers.

- The higher proportion of consumers expecting to consolidate their shopping trips to physical stores compared to a month ago reinforces our view that multi-brand and multi-category retailers—such as mass merchants and possibly department stores—will see stronger traffic and demand.

- Our survey reveals a shift of shopping channels from in-store to e-commerce for the holiday season, with a slight month-over-month increase in the number of consumers expecting to shop on Cyber Monday and a stable proportion of 30% planning to shop online.

- Brands and retailers should rethink their last-mile delivery to handle high volumes. This could include using stores to fulfill orders.

- Apparel: Online remains the preferred channel over brick-and-mortar retail for apparel shopping. We have seen a stable proportion of around one-third of consumers buying apparel online in the two weeks prior to each weekly survey, and 27% of respondents are currently purchasing more apparel online than pre-crisis. Although apparel remains the most-cut category, with 29% reporting that they are currently purchasing less apparel, the ratio of respondents buying less apparel to those buying more this week was 2.3—the lowest level since March.

- Online Grocery: Shopping for groceries online in the past two weeks rose week over week: One-third of consumers reported that they have recently bought groceries online. Echoing this, we saw a jump in the proportion of consumers buying more food or household products online. Our new US CPG Sales Tracker recorded recorded a slowdown in online food sales growth in June (to a still substantial 68%), and we will shortly publish updated sales data for July. However, we expect grocery e-commerce sales growth to remain at elevated levels, with capacity rather than demand proving to be the major constraint.

- E-Commerce: Consumer expectations to retain the habit of buying more online have levelled off at around 29%. This week, we found a near-identical percentage of holiday shoppers expecting to switch some spending to e-commerce this year. However, a much more substantial 72% said that they are currently buying more online—suggesting potential for a much greater swing to e-commerce than 29% of consumers in the coming months. We expect capacity in logistics to be an inhibitor on e-commerce growth as we move toward the holiday peak.