Source: Company reports/Coresight Research

Fiscal 2Q19 Results

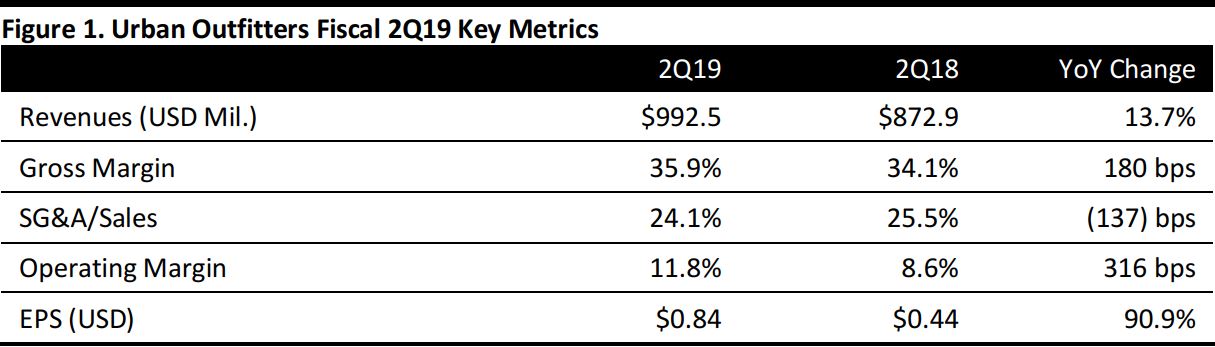

Urban Outfitters reported fiscal 2Q19 EPS of $0.84, up from $0.44 in the year-ago quarter and above the $0.76 consensus estimate. Total revenues were $992.5 million, up 13.7% year over year and above the $977.0 million consensus estimate.

By brand, Anthropologie Group net sales were $401.3 million, up 10.7% year over year. Urban Outfitters brand sales were $379.3 million, up 17.1% from the year-ago quarter. Free People sales increased by 14.5%, to $206.4 million. By division, retail segment net sales increased by 14.1%, to $902.0 million and wholesale segment sales were up 9.9%, to $90.4 million.

Same-store sales were up 13.0% during the quarter, beating the 11.2% consensus estimate. Comps were driven by double-digit growth in online sales and positive retail store sales. Digital continued strong growth, posting double-digit sales increases at each of the brands, driven by increases in sessions, average order value and conversion rates. Comps across brands were driven by increases in traffic (up 1%), average order value and units per transaction, which in turn, was driven largely by fewer markdowns as a percentage of sales.

All three brands posted double-digit retail segment comp sales, driven by strength in apparel and accessories. By brand, Free People comps were up 17.0%, beating the 14.2% consensus estimate. Anthropologie Group comps were up 11.0%, beating the 10.0% consensus estimate, and Urban Outfitters brand comps were up 15.0%, versus the 11.2% consensus estimate.

The company’s gross margin increased by 180 basis points, to 35.9%, primarily driven by lower markdowns at all three brands. These markdowns were partially offset by lower margins that were attributable in part by deleverage in delivery expense due to increased online penetration.

SG&A expense as a percentage of sales fell by 136 basis points compared with the year-ago period. The change in SG&A was primarily due to increased marketing expenses and direct selling.

Inventories increased by $10.5 million, or 2.9%, to $375.7 million on a year-over-year basis. Comparable retail segment inventory increased by 3.0% at cost.

Management noted that the 90.9% increase in first-quarter EPS was a result of strong sales, healthy margin improvement, SG&A leverage and a lower tax rate.

During the quarter, the company opened a total of seven new locations—three Free People stores, two Anthropologies Group stores and two Urban Outfitters stores—and closed two locations: one Urban Outfitters store and one Anthropologie Group stores.

Outlook

The company did not provide quantitative guidance for FY19.

- Urban Outfitters plans to open 17 new stores during the year and to close 11 stores. Anthropologie and the Food and Beverage divisions will each grow their store counts.

- The company anticipates that the digital channel will remain a strong sales growth driver.