Introduction

Subscription services continue to be a niche but significant disruptor to traditional retail, chipping away billions of dollars that would otherwise go to conventional retailers. Alongside other kinds of retail alternatives such as rental services, subscription services are providing a kind of “retail as a service” that combines the delivery of conventional products with a recurring revenue model that is similar to how consumers pay for services.

Online subscription services consist of customers receiving products on a routine, scheduled basis—usually monthly or quarterly. Subscription startups can scale operations quickly online. As we note in this report, however, the business model tends to come with high marketing costs.

Segmenting Subscriptions

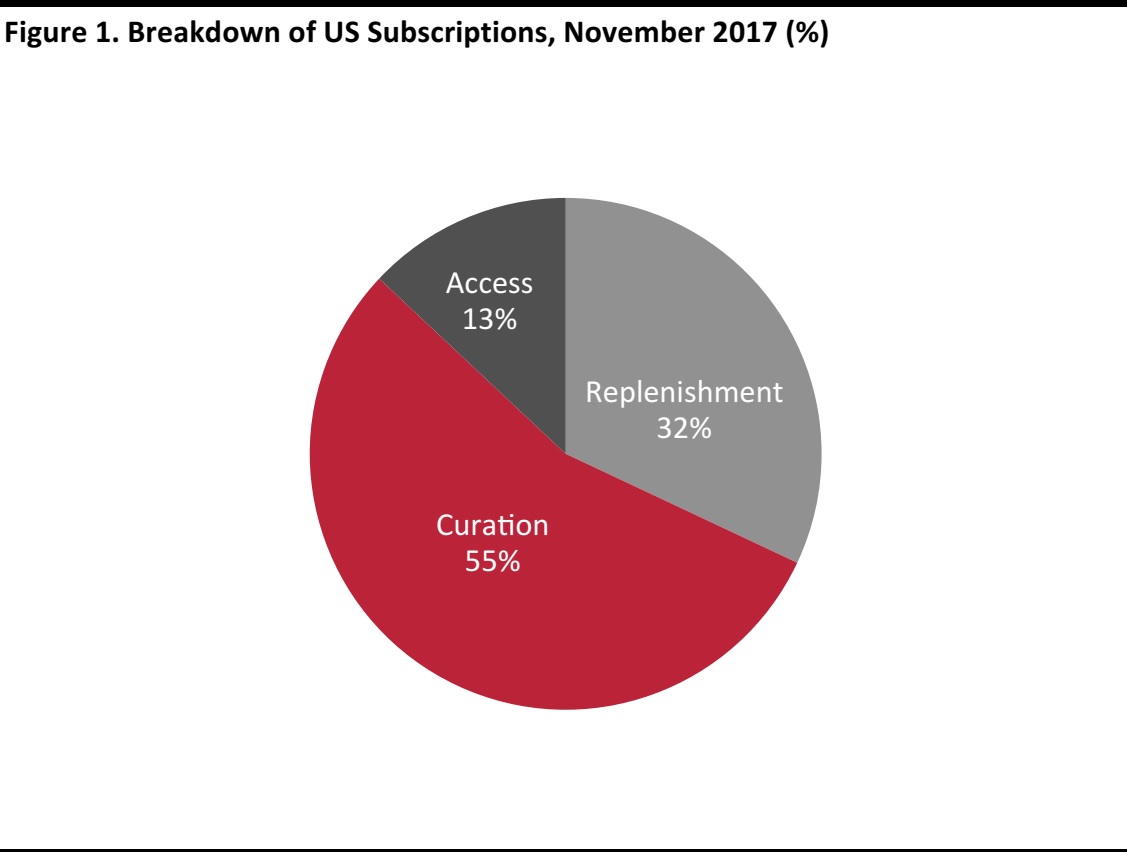

Most subscription services fall into one of two categories:

- Curation: This type of subscription service introduces shoppers to new products,such as samples of new-to-market cosmetics. Examples include Birchbox in beauty and Stitch Fix in apparel.

- Replenishment: This kind of service offers replenishment deliveries of regularly used, routine products such as men’s shaving items. Examples include Dollar Shave Club and Amazon Subscribe & Save.

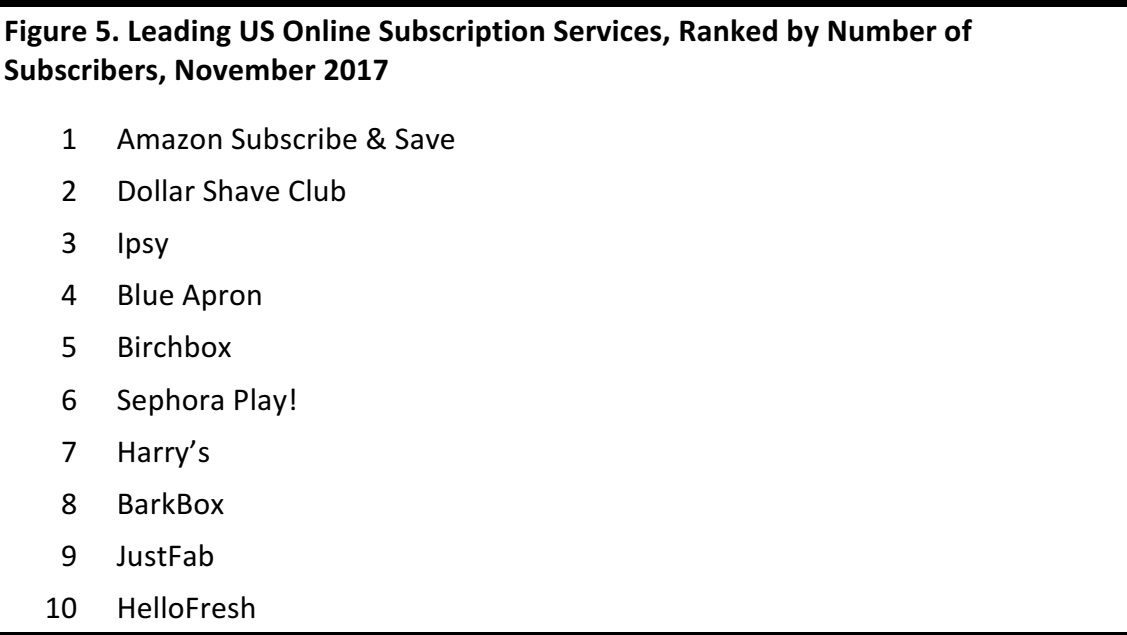

A more niche third segment consists of services that give subscribers access to benefits such as deep discounts. Examples of firms offering this type of service include NatureBox and JustFab. According to a consumer survey by consultants McKinsey in November 2017, the US subscription market breaks down, by number of subscribers, as follows:

Base: 607 US Internet users ages 18+ who have subscribed to a service in the past 12 months.

Source: McKinsey&Company

Sizing the Market

We believe that beauty and food are the two biggest subscription markets. For apparel, which is a semi durable category, the subscription market overlaps with the rental market and distinctions between the two are blurred.

- Beauty and personal care: We estimate that US consumers will spend around $1.9 billion on beauty and personal care subscription services this year, up from around $1.6 billion in 2017.

- Food subscription: US shoppers will spend around $3 billion on online meal kit services in 2018, we estimate, up from $2.6 billion in 2017. The total food subscription market, which includes segments such as snacks or sports nutrition sold on subscription, will be larger still.

- Apparel rental: We estimate that around $575 million will be spent on online apparel rentals in the US in 2018, up from approximately $500 million last year. This includes online rental services that do not use a subscription model.

Disruptors Being Disrupted

We are now seeing some US subscription commerce disruptors face disruption themselves. Two of the biggest subscription companies—meal-kits firm Blue Apron and beauty-box service Birchbox—appear to be struggling. Blue Apron has posted declining revenues and deepening losses, and website visitors to privately-owned Birchbox appear to be shrinking and the company has spent much of the past year looking for a buyer.

We see the challenges facing these two firms as typical of those facing all subscription companies: 1) high customer-acquisition costs; and 2) increased competition.

1) High Customer-Acquisition Costs

These models come with high acquisition and retention costs for several reasons, including convincing shoppers to switch to unfamiliar types of purchasing, preventing existing customers from returning to traditional channels, the lack of marketing visibility that physical retail formats enjoy and competition from rivals seeking to tempt shoppers with introductory offers. Customer churn rates are believed to be high.

In 2017, Blue Apron spent a substantial 17.5% of its revenues on marketing costs, although this was down from 18.1% in 2016. HelloFresh does not break out marketing costs in its financial reports, but its total selling, general and administrative (SG&A) costs accounted for fully 71.8% of revenues in 2017. Blue Apron’s 2017 SG&A ratio was 50.2%. For comparison, Walmart reported an SG&A ratio of 21.0% in 2017.

2) Increased Competition

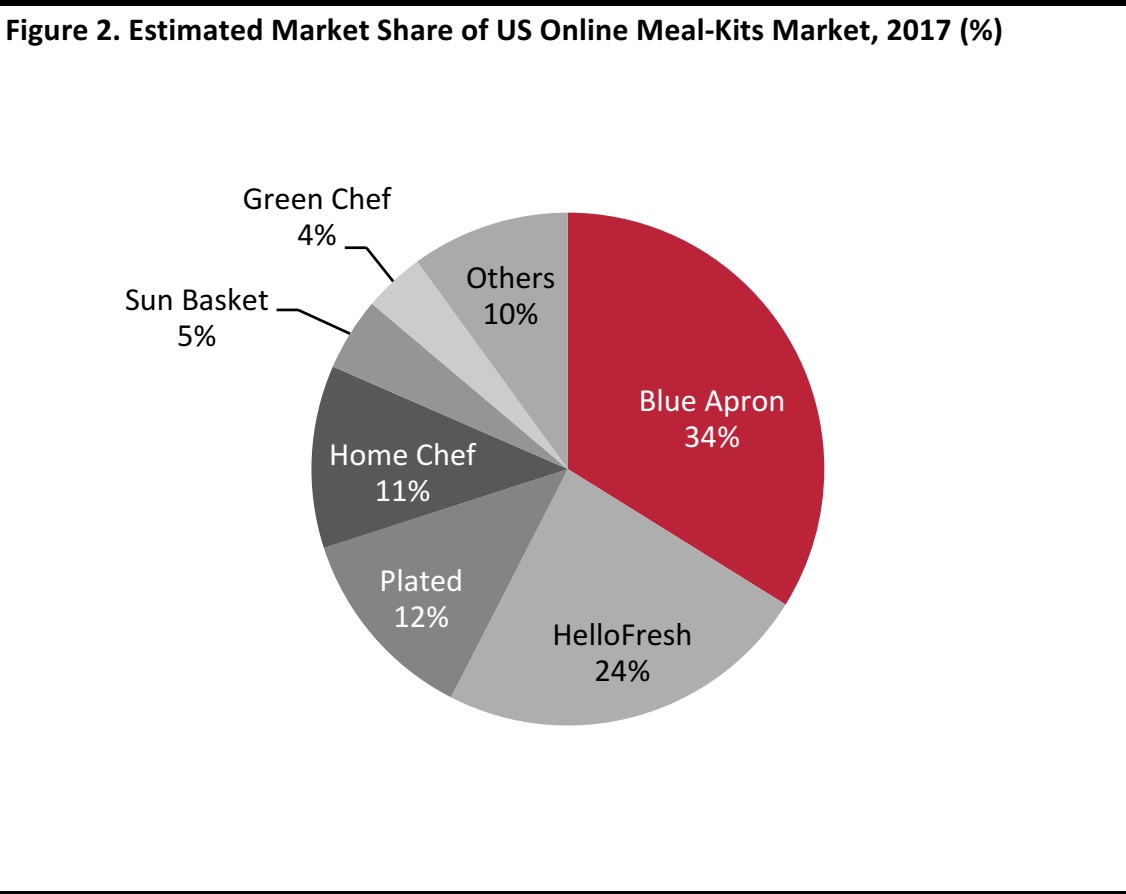

Incumbents face heightened competition from newer entrants, attracted by the prospect of market growth. In the US, HelloFresh is powering ahead in meal kits, almost certainly at the expense of Blue Apron. As we discuss later, we expect these two players to be neck and neck in terms of market share this year. Meanwhile, Birchbox has reportedly lost customers to rival Ipsy.

Blue Apron Faces Difficulties

The market leader in meal kits Blue Apron has been posting falling revenues and deepening losses. It attributed its recent decline in revenues to a scaling back of marketing activity. However, it faces heightened competition and the challenge of high customer turnover rates.

In the first quarter of 2018, Blue Apron’s revenues fell by 20% year over year, accelerating from a 13% decline in the fourth quarter of 2017. On the company’s fiscal 2017 earnings call, CEO Brad Dickerson said “We believe that it will take time to build momentum this year, particularly given our significant pullback in marketing in the second half of last year.”

In 2017, Blue Apron posted revenues of $881 million and guided for 2018 revenues to be “moderately down” on those reported in 2017, with negative growth falling most heavily in the first quarter. If we assume a full-year decline of 5%, that would suggest 2018 revenues of $837 million. Blue Apron reported a net loss of $210 million in 2017, versus a loss of $55 million in the prior year.

HelloFresh is fast catching up with Blue Apron. In 2017, HelloFresh reported US-only revenues of €545 million ($616 million), up fully 94% in dollar terms year over year. Based on company guidance, HelloFresh looks likely to increase its US sales by around 30%–35% this year, implying that it would be snapping at Blue Apron’s heels with around $816 million in US revenues in 2018. HelloFresh reported a net loss of €92 million ($104 million) in 2017, versus a loss of €94 million ($106 million) in 2016.

We expect Blue Apron and HelloFresh to be neck and neck in the US market this year. HelloFresh acquired Green Chef in March 2018, and that may help it to edge ahead of Blue Apron in terms of market share.

Source: Company reports/Coresight Research

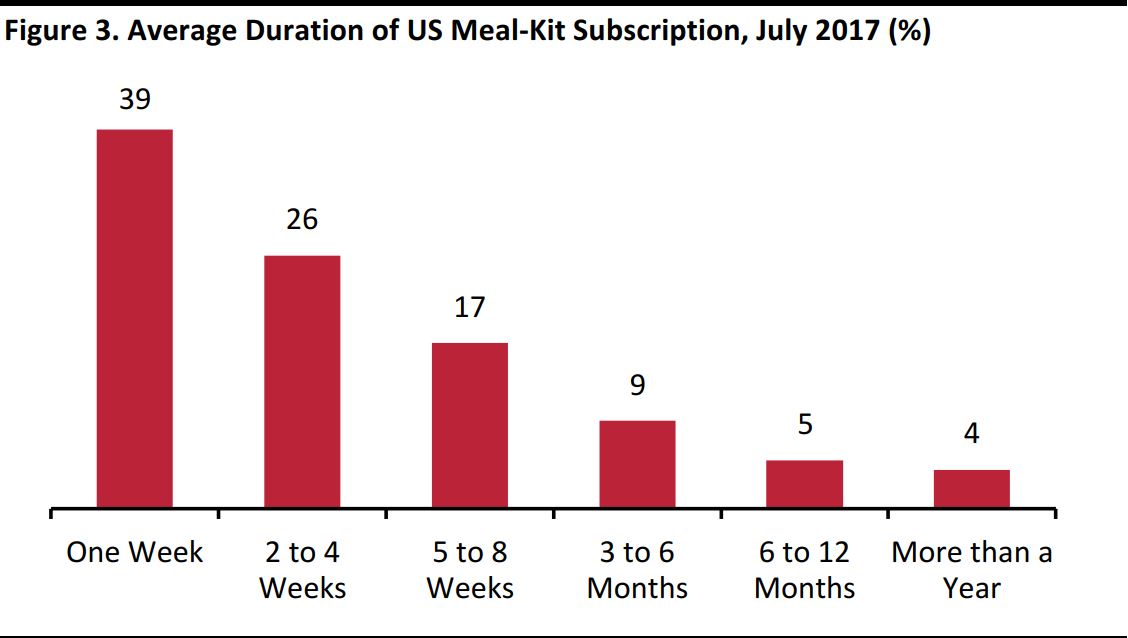

A challenge that all meal-kit subscription firms face is apparently high customer churn rates. As we show below, the majority of those consumers who have subscribed to meal kits have done so for only a very short time. Many consumers appear to find the format inconvenient—because it imposes forced meal choices and has a lack of flexibility. In addition, meal-kit firms are competing against deep introductory promotions from rivals.

The high turnover of customers suggests that meal-kit firms will continue to face substantial customer-acquisition costs and so will find it challenging to consistently achieve profitability.

Base: 2,191 US consumers ages 18+.

Source: Morning Consult

Base: 2,191 US consumers ages 18+.

Source: Morning Consult

Signs of Struggles at Birchbox

After nearly a year of trying to find a buyer, Birchbox sold itself to an existing investor this spring. On May 1, 2018, news website Recode reported that one of Birchbox’s investors, the hedge fund Viking Global Investors, had acquired a majority stake in the company, after agreeing to invest around $15 million of new cash. Birchbox had been up for sale since summer 2017 and had been engaged in talks with QVC and Walmart ahead of debt secured in 2015 reportedly becoming due in early 2018.

Recode reported that Birchbox’s other investors, which include venture capital firms, would see their investments wiped out. It also said that the company had struggled to grow fast and profitably, due to high customer-acquisition costs and the low margins associated with selling third-party brands.

Meanwhile, rival subscription site Ipsy, which offers monthly “Glam Bags” with personalized beauty content, has reportedly captured market share at the expense of Birchbox. In September 2017, Ipsy said that it had more than 3 million subscribers; in May 2018, Birchbox said that it had 2.5 million subscribers.

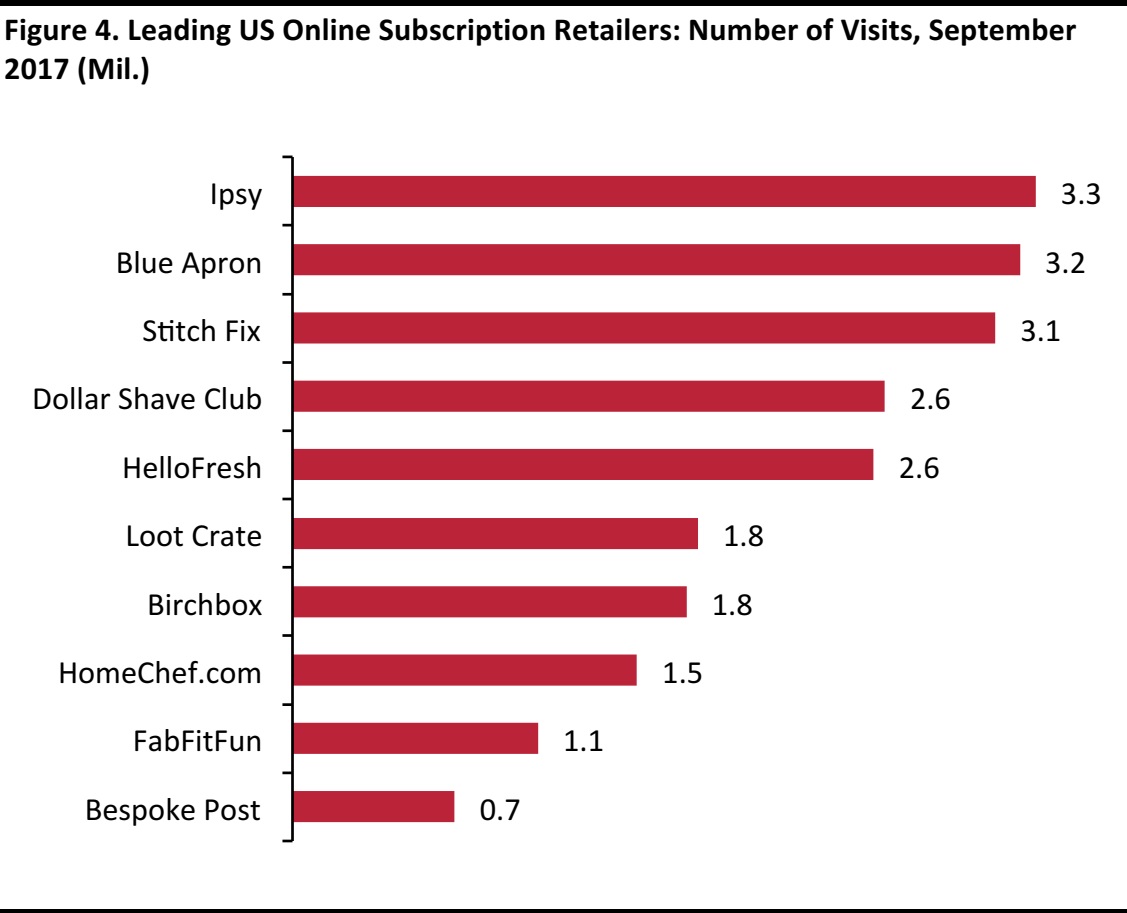

Also bearing out Ipsy’s leadership over Birchbox are website visitor figures from Hitwise:

- In January 2016, Hitwise reported 3.6 million monthly visits to Birchbox.com

- By September 2017, Hitwise was reporting just 1.8 million monthly visitors to Birchbox’s site.

- In September 2017, Ipsy’s site attracted 3.3 million monthly visitors.

Subscription Services: Consumer Overview

Overall Rankings

By number of visitors, the most-popular specialized subscription services were split between apparel, food and personal care, as of September 2017. Stitch Fix represents apparel, Blue Apron and HelloFresh represent food, and Ipsy and Dollar Shave Club represent personal care.

Source: Hitwise/eMarketer

Source: Hitwise/eMarketer

In terms of coverage of subscription services, Amazon is often overlooked in favor of specialized providers. However, a consumer survey by McKinsey in November 2017, found Amazon Subscribe & Save was the most popular subscription service in the US, although it did not put a figure on the number of subscribers. McKinsey’s data also confirmed that Ipsy is outperforming Birchbox.

Base: 607 US Internet users ages 18+ who had subscribed to a service in the past 12 months.

Source: McKinsey& Company

Base: 607 US Internet users ages 18+ who had subscribed to a service in the past 12 months.

Source: McKinsey& Company

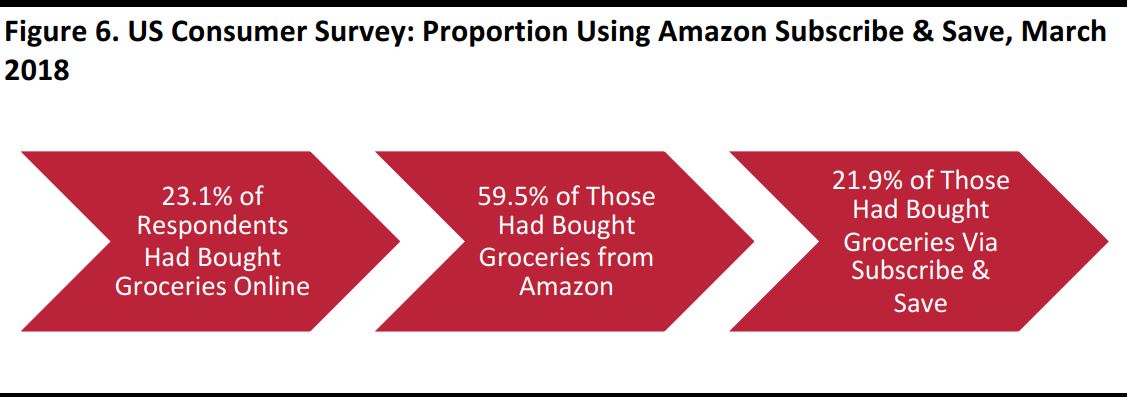

In addition, our own

online grocery consumer survey found that 22% of online grocery shoppers who had bought groceries from Amazon had used Subscribe & Save. Extrapolating from these figures, suggests that around 3% of all US consumers had used Subscribe Save to buy grocery items in the 12 months prior to our survey.

Survey questions referred to purchases in the past 12 months.

Base: 1,885 US Internet users ages 18+.

Source: Coresight Research

Survey questions referred to purchases in the past 12 months.

Base: 1,885 US Internet users ages 18+.

Source: Coresight Research

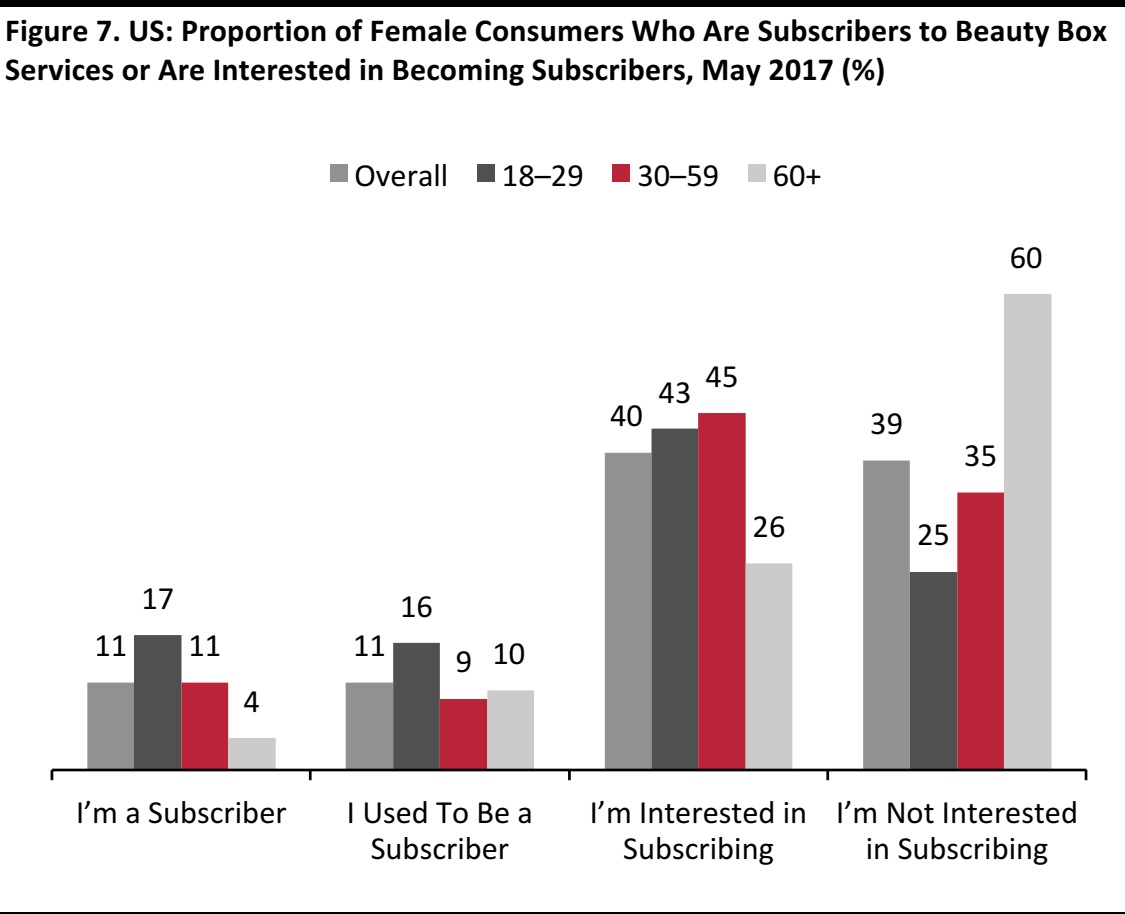

There remains substantial interest in subscribing to beauty subscription services:some 40% of US female respondents told Statista that they were actively interested in signing up, while 39% had no interest in subscribing.

Base: 1,006 US female respondents ages 18+.

Source: Statista

Base: 1,006 US female respondents ages 18+.

Source: Statista

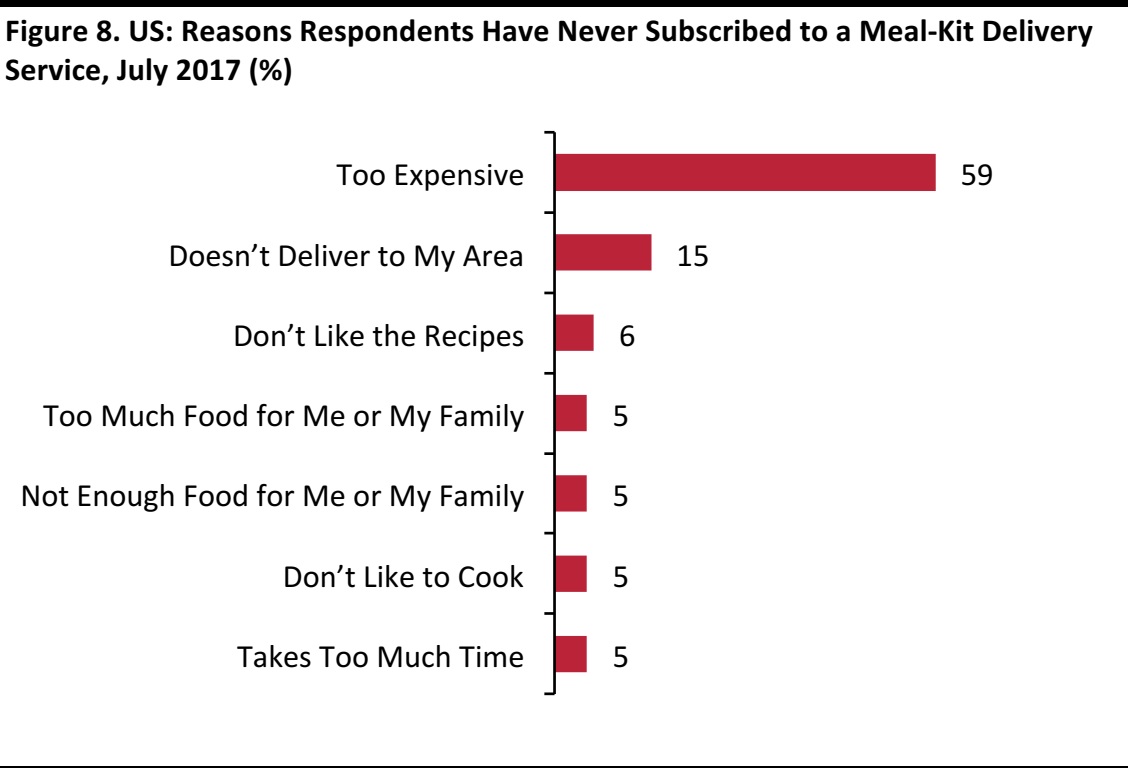

According to a 2017 survey by survey firm Morning Consult, high prices are the most-cited reason for not subscribing to a meal-kit service.

We also perceive a convenience barrier to widespread uptake of meal kits, although this was not included in the options provided in Morning Consult’s survey. Even while more and more consumers opt to plan and buy meals at the last moment, meal kits demand advance planning and give consumers limited flexibility to change their plans and preferences: once their meal kit has arrived, customers are committed to preparing a specified meal. In some respects, therefore, meal kits run counter to the macro trend of shoppers expecting greater convenience.

Base: 1,772 US consumers ages 18+ who have never subscribed to a meal-kit service.

Source: Morning Consult

Base: 1,772 US consumers ages 18+ who have never subscribed to a meal-kit service.

Source: Morning Consult

Profiling Major Subscription Firms

Below, we highlight some of the most-popular and prominent online subscription services.

Apparel, Footwear and Accessories

Rent the Runway

Pure-play, online designer fashion apparel and accessories rental company Rent the Runway launched a subscription service called Unlimited in March 2017. The service charges consumers $139 for monthly rentals or $1,700 annually. The subscription provides customers with a rotating closet of rented designer pieces to women that would otherwise not be able to afford them. The company was founded in 2009 and operates retail locations in Chicago, New York City, Washington, D.C., Los Angeles, San Francisco and Las Vegas.

Gwynnie Bee

US-based Gwynnie Bee offers online women’s plus-size fashion rentals by subscription, targeting professional women ages 28–45. Gwynnie Bee offers women’s clothing rentals in sizes 10–32 from more than 190 brands, including ASOS. Since 2012, the company has increased sales by 10%–15% annually, becoming one of the largest purchasers in plus-size fashion. By 2015, the company had shipped more than 3 million subscription boxes.

Borrow For Your Bump

US-based Borrow For Your Bump is an online maternity-wear rental service. The company provides a one-time dress rental and/or a subscription box service for various maternity items. For $99, renters can borrow four items for 30 days.

Le Tote

San Francisco-based Le Tote offers a member service option that allows customers to rent a broad selection of apparel and accessories for a monthly fee of $59. Available brands include Nike, Lucky Brand, Vince Camuto, French Connection and Levi’s. Le Tote also offers maternity clothing and a specialized maternity subscription.

Stitch Fix

Stitch Fix was founded in 2012 and offers an online subscription clothing and styling service. Customers fill out style surveys and measurements, and based on algorithms, the company’s fashion stylists select five items from a variety of brands to send to the customer. Customers keep what they like and return anything that doesn’t suit them. Stitch Fix employs over 2,800 stylists.

Fabletics

Fabletics is an activewear subscription service that sends personalized fitness outfits based on personal workout and lifestyle preferences. Members are charged $49 for a monthly subscription and have the option to skip a month.

Ivory Clasp

Ivory Clasp offers a subscription service for in-season, stylish handbags that retail for over $100 for just $45 per month. The service sends name-brand bags and allows the subscriber to keep the purses they receive. Customers first take a style quiz. Subscribers can choose to pay $45 per month, or $45 bimonthly to receive a new bag every other month. Subscribers can get a full refund for any bag they do not like that is returned. The startup has been testing the service for a few months with over 300 active users and has hit $10,000 in monthly recurring revenues.

LSwop

LSwop (Luxury Swop) is an online, pure-play luxury sneaker rental service for men. The company operates on a monthly subscription business model, and sneakers can be rented for a period of one to four days. Customers can rent one pair a month for $150, two pairs for $250 and three pairs for $350. LSwop offers luxury sneakers which are typically priced at $800–$1,000 from Tom Ford, Christian Louboutin, Balmain, Givenchy and Rick Owens, among others. According to the company’s founder, no sneakers are rented out more than two times and subscribers can purchase sneakers at a discounted price. This fall, the company set up a temporary pop-up store in Soho in New York.

Briefd

A number of online underwear subscription services have sprung up in the UK, the US and Australia. The subscriber pays a fixed monthly fee and receives one to three pairs of underwear a month; subscription tiers are based on brand, quality and the required number of items. Some startups specialize in plus sizes or sizes outside of standard sizing. Several of the startups have raised investment funding of over $10 billion each.

One such UK online underwear subscription service for men is called Briefd. The company has a two-tier subscription service consisting of one pair of underwear shipped per month for £17.99, or a higher-end pair for £23.99 per month. Brands include Armani, Hugo Boss, Calvin Klein, Ralph Lauren, Tommy Hilfiger, French Connection and Diesel, among others. Some other underwear subscription startups include RelatedGarments,

MeUndies and

Nice Laundry.

Beauty and Personal Care

Subscription services in the beauty and personal care categories span functional purchase categories, such as razor blades, and categories where shoppers want to discover new products, such as cosmetics.

Birchbox

New York-based Birchbox pioneered the first subscription box service when it launched one for beauty products in 2010. The company offers subscriptions for weekly and monthly deliveries of up-and-coming beauty products and cosmetics shipped in attractive boxes decorated with flowers, bright neons and abstract designs. On May 1, 2018, news website Recode reported that one of Birchbox’s investors, the hedge fund Viking Global Investors, had acquired a majority stake in Birchbox. Birchbox had been up for sale since summer 2017.

Honest Company

Honest Company, cofounded by actress Jessica Alba, sells healthy and natural consumer goods such as disposable baby diapers, household cleaners, personal-care and beauty products. The company distributes through brick-and-mortar retailers including Target and Whole Foods, but many consumers purchase through monthly subscription services.

Scent Trunk

Scent Trunk, a US e-commerce fragrance company, offers customized scents based on personal preferences and sells them through a subscription model. Scent Trunk sends customers a sampling kit or scent test that contains six core scents, representing different fragrance types. Customers fill out an online form about the scent test, and then the company creates a custom-blended fragrance using raw ingredients sourced from small-batch producers. The perfumes are dispersed in 5 ml bottles and shipped every month for $11.95. The company stated that it targets millennials.

Ipsy

Ipsy charges members $10 per month for a delivery of five product samples, which are reportedly provided free to the company by beauty brands. It was founded in 2011. In September 2017, CEO Marcelo Camberas stated that the company had 3 million subscribers. The company focuses on customizing its product offerings and says that it produces more than 10,000 variations of its Glam Bags each month.

Dollar Shave Club

Founded in 2011, male grooming products firm Dollar Shave Club offers a monthly subscription of shaving products and accessories. Razor subscriptions options are offered for $1, $6 and $9 monthly. Dollar Shave Club had 3 million subscribers and revenues of $160 million in 2016. Unilever purchased the company in July 2016 for $1 billion, marking unicorn valuation. The company estimated that it would reach sales of $200 million in 2016. Dollar Shave Club developed customer recognition through entertaining and humorous online advertisements on social media.

Harry’s

After Dollar Shave Club, Harry’s is one of the largest online sellers of shaving products for men. Harry’s was founded in 2011 and offers customized subscription plans based on needed frequency and desired products. In 2013, Harry’s opened a barber shop and store in New York to promote the brand offline. Harry’s had over 2 million customers, according to a Business Insider report published in July 2016.

Glossybox

Glossybox was founded in Berlin in 2011 and claims to be Europe’s number-one provider of beauty box subscription services. It operates in 10 countries, including the UK, the US, Germany, France and Sweden. Glossybox was acquired by UK online retailer The Hut Group in August 2017.

Jewelry

Rocksbox

Rocksbox offers three jewelry pieces at a time and free shipping and returns for $21 per month on a try-before-you-buy model; if the subscriber decides to keep an item, the $21 is applied toward the purchase. The site carries more than 30 designers such as House of Harlow 1960, Kendra Scott, Loren Hope and Sophie Harper. The company uses technology for greater personalization and previously stated an expectation that it would triple sales in 2017.

Flowers

bloomon

Amsterdam-based bloomon offers a flower-subscription service that delivers in Holland as well as the UK, Belgium, Denmark and Germany. The company collaborates with over 400 growers, designs in-season bouquets and delivers within 24 hours of order placement. The founder stated that there is potential for expansion, as its current customers are buying more flowers, meaning the company is growing the market itself.

Food

A number of subscription service companies are catering to demands for healthy eating and convenience.

Graze

Graze offers healthy snack discovery boxes, with regular deliveries of new flavors and a selection of over 100 different snack choices. Snacks are handpicked based on personal preferences.

Freshology

US-based Freshology offers a customized,gourmet meal program, with low-carb and gluten-free options, using seasonal, locally-sourced ingredients and all-natural, hand-crafted meals. Meals are delivered twice weekly.

Detox Kitchen

UK-based Detox Kitchen was founded in 2012 and offers a healthy and tasty meal delivery service. The company expected to grow by 50% year over year to £4.5 million in 2017, according to news website

Independent. Subscribers can select from five different packages, including one for vegans, starting at £28.90 daily, and one called “active protein” for £39.95 daily.

Blue Apron

New York subscription service Blue Apron offers weekly meal kits, ingredients and recipes for make-at-home meals. Blue Apron completed an IPO in June 2017, valuing the company at about $1.9 billion.The company reported revenues of $881 million in 2017, up from $795 million in 2016. However, as we noted earlier, revenues declined year over year in the fourth quarter of 2017 and the first quarter of 2018 (latest at the time of writing).

HelloFresh

Fast-growing meal-kits firm HelloFresh was founded in Germany in 2011. In November 2017, it went public with an IPO, which implied a company valuation of €1.7 billion ($1.9 billion at 2017 exchange rates). In 2017, HelloFresh reported US revenues of $545 million ($616 million) and international revenues of €360 million ($407 million). In March 2018, HelloFresh acquired smaller US rival Green Chef.

Key Takeaways

Consumers can benefit from the convenience of replenishment subscriptions and the excitement of curated subscriptions. However, the sustainability of standalone subscription services remains largely unproven.Facing new competition and high marketing costs, some of the biggest subscription firms are facing challenges in terms of growth and profitability.

Amazon Subscribe & Save is one of the most-popular subscription services, and we think that the subscription model is likely to work best as part of a suite of online purchasing options. A hybrid model means customers who want to transfer out of a subscription service can do so while remaining with the same retailer—for example, from Amazon Subscribe & Save to Amazon’s regular retail website—and the enhanced scale provides opportunities to leverage fixed costs associated with pure-play e-commerce and subscription models.