Nitheesh NH

Introduction

Each report in our Sector Overview series analyzes a retail sector or consumer market. In this report, we dive into the U.S. home and home improvement segment, including hardware stores and furniture and home goods companies.

This report includes:

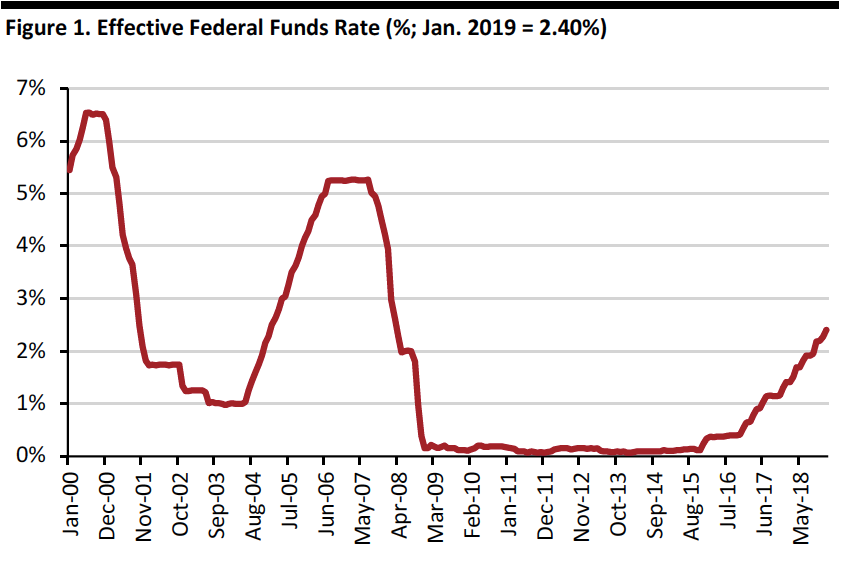

Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

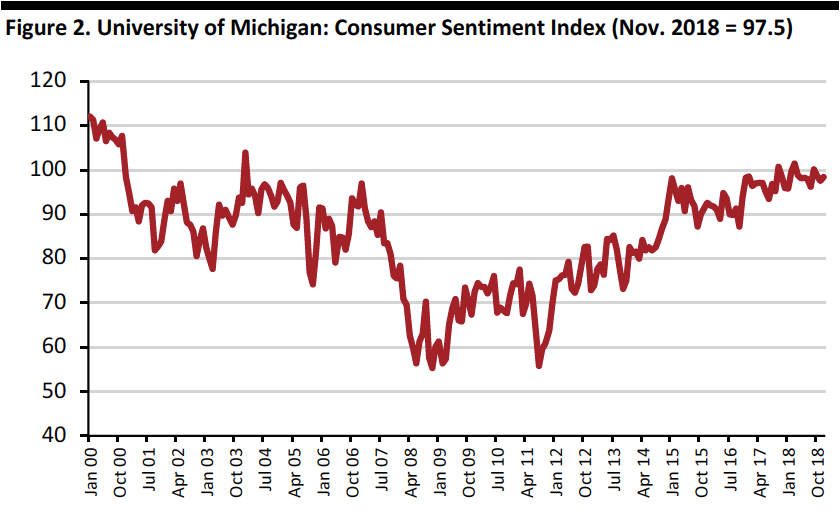

Has US Consumer Confidence Peaked?

The University of Michigan Consumer Sentiment Index has been on the rise, after dipping to a relative trough of 55.8 in August 2011. However, the index appears to have peaked, having declined for the last three consecutive months and has failed to set new highs following a relative high of 101.7 in October 2017.

[caption id="attachment_72119" align="aligncenter" width="580"]

Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

Has US Consumer Confidence Peaked?

The University of Michigan Consumer Sentiment Index has been on the rise, after dipping to a relative trough of 55.8 in August 2011. However, the index appears to have peaked, having declined for the last three consecutive months and has failed to set new highs following a relative high of 101.7 in October 2017.

[caption id="attachment_72119" align="aligncenter" width="580"] Source: University of Michigan[/caption]

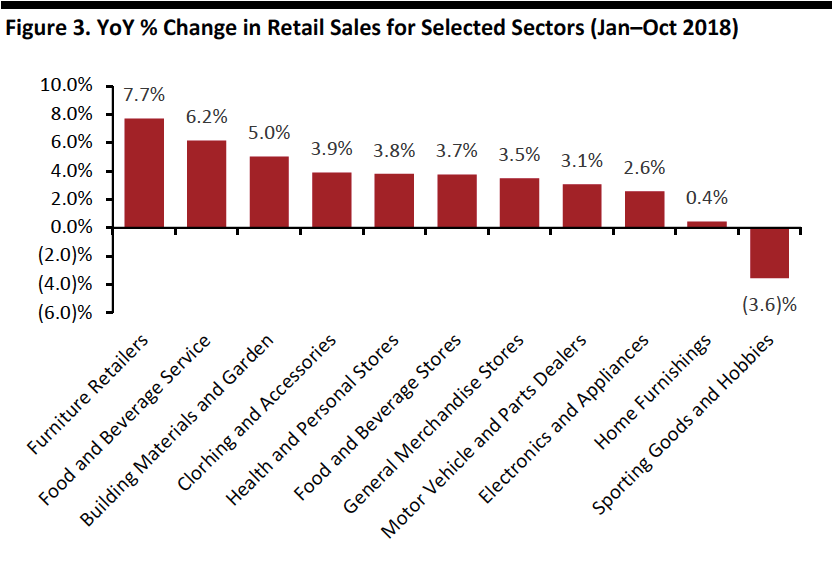

Home Improvement Leads Retail Growth

In the first 10 months of 2018, two of the three strongest retail sectors year over year were furniture and building materials and garden equipment, according to data from the U.S. Census Bureau, as shown in the figure below.

[caption id="attachment_72124" align="aligncenter" width="580"]

Source: University of Michigan[/caption]

Home Improvement Leads Retail Growth

In the first 10 months of 2018, two of the three strongest retail sectors year over year were furniture and building materials and garden equipment, according to data from the U.S. Census Bureau, as shown in the figure below.

[caption id="attachment_72124" align="aligncenter" width="580"] Source: U.S. Census Bureau[/caption]

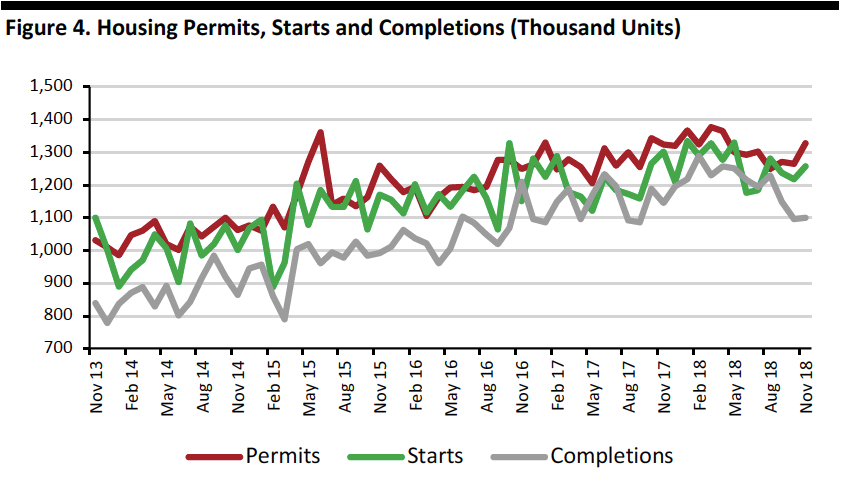

Data on Housing Permits, Starts and Completions Are Mixed but Remain at a High Level

Data on new housing permits, starts and completions offer mixed results, with housing permits up year over year and starts and completions down year over year. Still, this is relatively good news, since permits are the gating factor for a housing start or completion.

Authorized housing permits increased 5.0% month to month in November and 0.5% year over year, according to U.S. Census Bureau data. Housing starts increased 3.2% month to month but declined 3.6% year over year. Similarly, housing completions increased 0.4% month to month but declined 3.8% year over year.

[caption id="attachment_72126" align="aligncenter" width="580"]

Source: U.S. Census Bureau[/caption]

Data on Housing Permits, Starts and Completions Are Mixed but Remain at a High Level

Data on new housing permits, starts and completions offer mixed results, with housing permits up year over year and starts and completions down year over year. Still, this is relatively good news, since permits are the gating factor for a housing start or completion.

Authorized housing permits increased 5.0% month to month in November and 0.5% year over year, according to U.S. Census Bureau data. Housing starts increased 3.2% month to month but declined 3.6% year over year. Similarly, housing completions increased 0.4% month to month but declined 3.8% year over year.

[caption id="attachment_72126" align="aligncenter" width="580"] Source: U.S. Census Bureau[/caption]

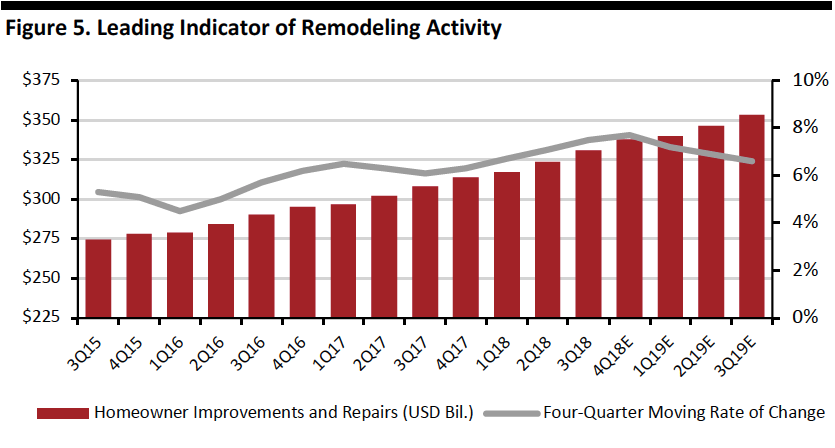

Growth Rate of Spending on Home Improvement Is Expected to Slow

Annual growth in national spending on home improvement and repair is expected to decelerate in 2019, due to rising mortgage interest rates and flat home sales activity, according to the Joint Center for Housing Studies of Harvard University. Despite this deceleration, other indicators such as home prices, permit activity, and retail sales of building materials are expected to continue to strengthen and drive continued increases in spending in 2019.

[caption id="attachment_72127" align="aligncenter" width="580"]

Source: U.S. Census Bureau[/caption]

Growth Rate of Spending on Home Improvement Is Expected to Slow

Annual growth in national spending on home improvement and repair is expected to decelerate in 2019, due to rising mortgage interest rates and flat home sales activity, according to the Joint Center for Housing Studies of Harvard University. Despite this deceleration, other indicators such as home prices, permit activity, and retail sales of building materials are expected to continue to strengthen and drive continued increases in spending in 2019.

[caption id="attachment_72127" align="aligncenter" width="580"] Source: Joint Center for Housing Studies of Harvard University[/caption]

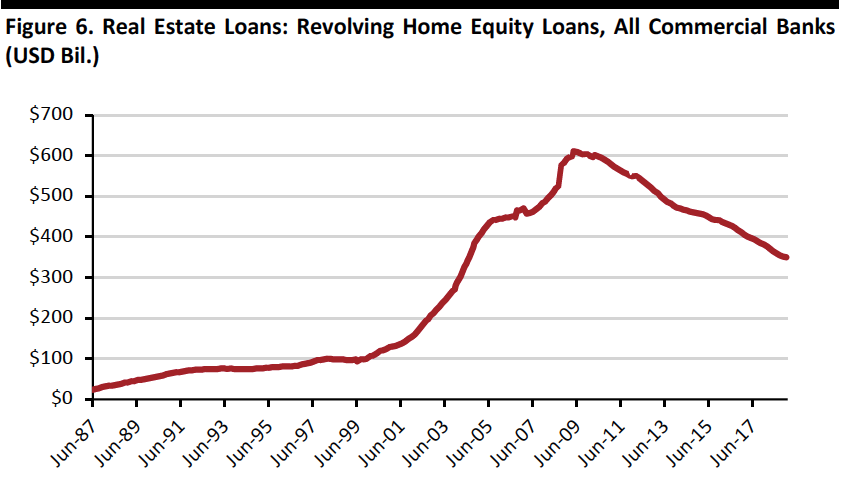

Total Home Equity Loans Still Declining from Peak in 2009

Total U.S. home equity loans are down 43% from the peak of more than $611 billion in May 2009, reflecting lower debt levels among U.S. homeowners but offering additional firepower for future home improvements. Total U.S. home equity loans are shown in the figure below.

[caption id="attachment_72130" align="aligncenter" width="580"]

Source: Joint Center for Housing Studies of Harvard University[/caption]

Total Home Equity Loans Still Declining from Peak in 2009

Total U.S. home equity loans are down 43% from the peak of more than $611 billion in May 2009, reflecting lower debt levels among U.S. homeowners but offering additional firepower for future home improvements. Total U.S. home equity loans are shown in the figure below.

[caption id="attachment_72130" align="aligncenter" width="580"] Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

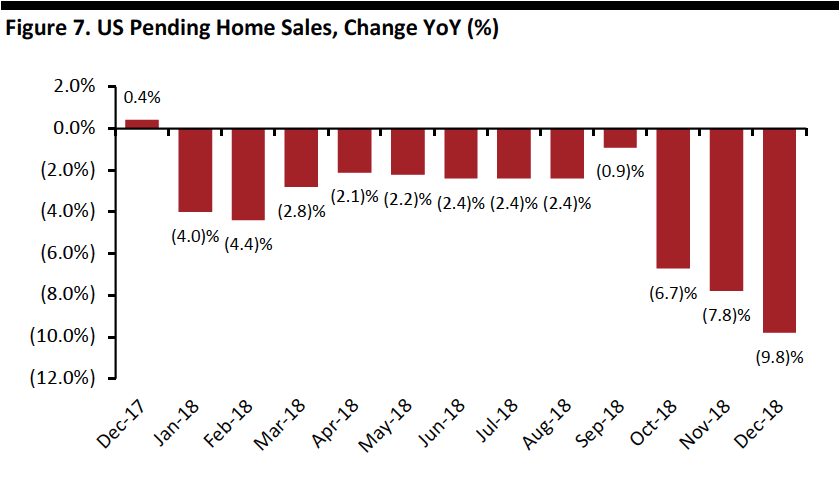

Slowdown in US Existing Home Sales Accelerates

Following nine consecutive months of declines, the fall in pending new home sales deepened further in the last months of 2018. The slide is likely due to high home prices and higher mortgage rates, keeping potential buyers on the sidelines. This could also dampen demand for home renovations and improvements.

[caption id="attachment_72134" align="aligncenter" width="580"]

Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

Slowdown in US Existing Home Sales Accelerates

Following nine consecutive months of declines, the fall in pending new home sales deepened further in the last months of 2018. The slide is likely due to high home prices and higher mortgage rates, keeping potential buyers on the sidelines. This could also dampen demand for home renovations and improvements.

[caption id="attachment_72134" align="aligncenter" width="580"] Source: National Association of Realtors[/caption]

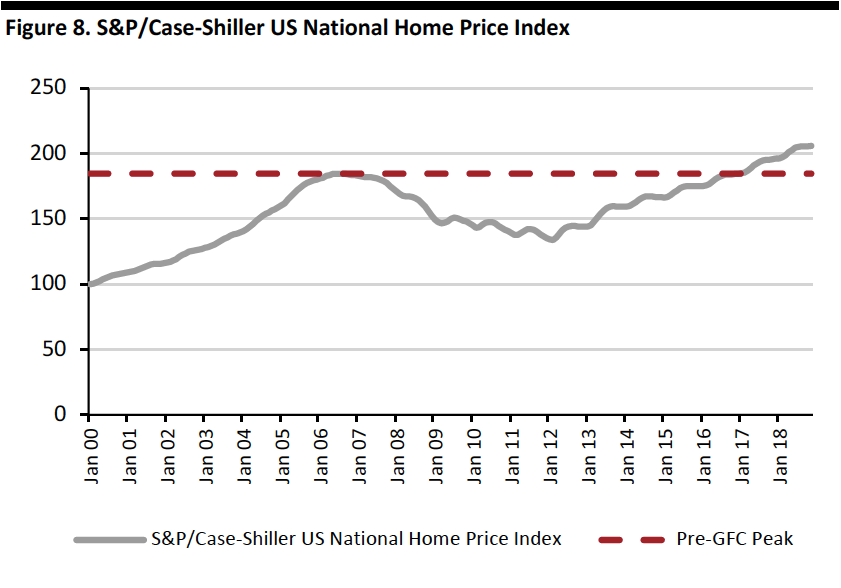

US Home Prices Exceed Pre-Global Financial Crisis Levels

In the first 11 months of 2018, U.S. home prices, based on the S&P/Case-Shiller index, were up 5% and exceeded the pre-Global Financial Crisis (GFC) peak in January 2017.

[caption id="attachment_72136" align="aligncenter" width="580"]

Source: National Association of Realtors[/caption]

US Home Prices Exceed Pre-Global Financial Crisis Levels

In the first 11 months of 2018, U.S. home prices, based on the S&P/Case-Shiller index, were up 5% and exceeded the pre-Global Financial Crisis (GFC) peak in January 2017.

[caption id="attachment_72136" align="aligncenter" width="580"] Note: Index Jan 2000=100; not seasonally adjusted

Note: Index Jan 2000=100; not seasonally adjusted

Source: S&P Dow Jones Indices [/caption] Lowe’s Management Change and Reboot Promise Operational Improvements and Modernization Lowe’s experienced a complete change of senior management in 2018, with Chairman, President and CEO Robert Niblock announcing his retirement in March 2018, followed by CFO Marshall Croom in June 2018. Marvin Ellison, the company’s new President and CEO, has more than 30 years of retail experience, including stints as Chairman and CEO of JCPenney (where he is credited with achieving a turnaround), in addition to 12 years at Home Depot, including serving as Executive VP of U.S. stores during 2008–2014. David Denton was named CFO in August 2018. Upon assuming his new position, Ellison undertook a detailed reassessment of the business and started implementing process and technology improvement strategies in the following areas: Note: LTM represents last 12 months through Sept. 30, 2018

Note: LTM represents last 12 months through Sept. 30, 2018

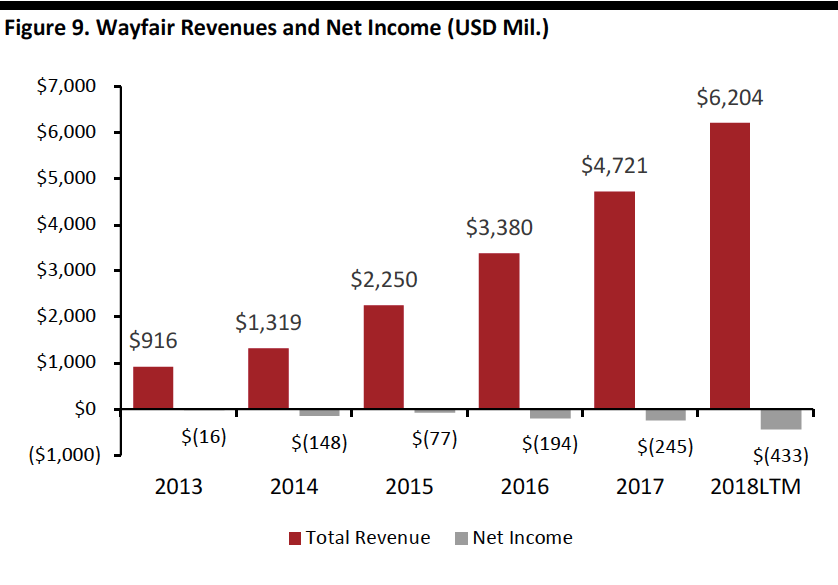

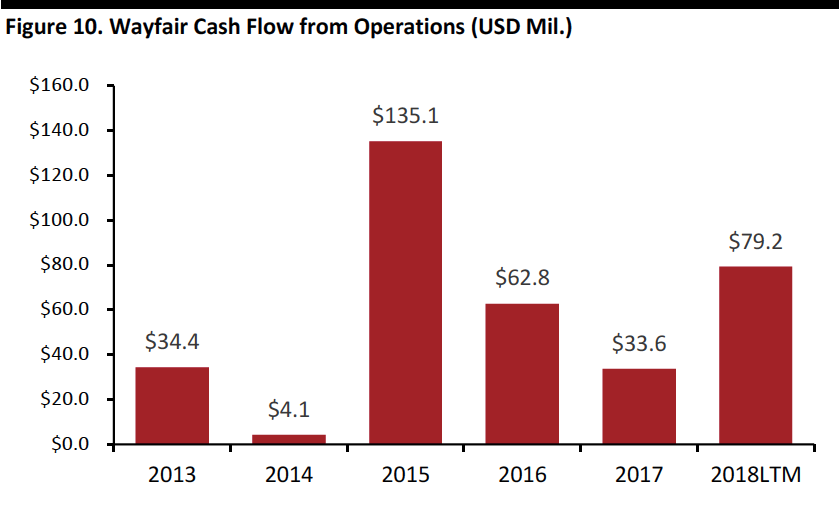

Source: S&P Capital IQ[/caption] The lack of profitability is not an issue itself, though a lack of liquidity could limit the company’s flexibility. That said, capital markets remain open: Wayfair raised $319 million in its IPO and sold $375 million of convertible notes in September 2017. Moreover, there is more to the picture than just net income: Wayfair generated positive cash flow from operations for the past five years and the first three quarters of 2018. [caption id="attachment_72141" align="aligncenter" width="580"] Note: LTM represents last 12 months through Sept. 30, 2018

Note: LTM represents last 12 months through Sept. 30, 2018

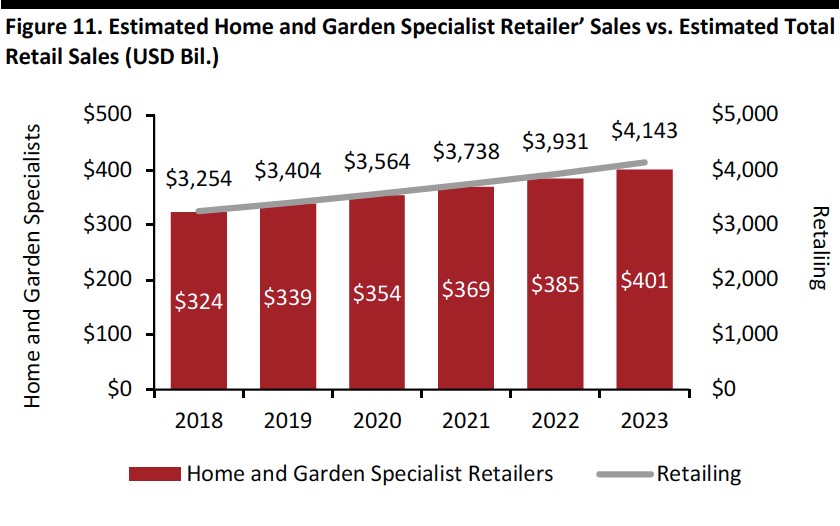

Source: S&P Capital IQ[/caption] Sector Momentum Sector Size and Growth The U.S. retail market was estimated at $3.3 trillion in 2018 and is expected to grow at a 4.9% CAGR during 2018–2023, with internet-based retail raising the aggregate average, according to data from Euromonitor International. During this period, the home and garden specialist sector is forecast to grow at a slightly slower 4.4% CAGR. [caption id="attachment_72144" align="aligncenter" width="580"] Source: Euromonitor International/Coresight Research[/caption]

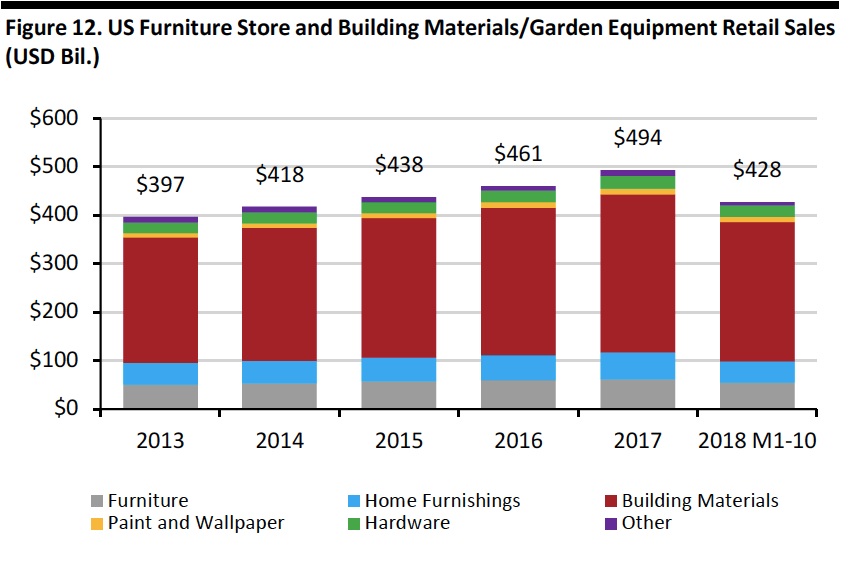

The graph below includes data for U.S. furniture store and building materials/garden equipment retail sales, which together amounted to nearly $500 billion in 2017 and grew at a 5.6% CAGR during 2013–2017. For 2018, we show data for the first 10 months.

[caption id="attachment_72146" align="aligncenter" width="580"]

Source: Euromonitor International/Coresight Research[/caption]

The graph below includes data for U.S. furniture store and building materials/garden equipment retail sales, which together amounted to nearly $500 billion in 2017 and grew at a 5.6% CAGR during 2013–2017. For 2018, we show data for the first 10 months.

[caption id="attachment_72146" align="aligncenter" width="580"] Source: U.S. Census Bureau/Coresight Research[/caption]

Headwinds and Tailwinds

Sector Headwinds

Source: U.S. Census Bureau/Coresight Research[/caption]

Headwinds and Tailwinds

Sector Headwinds

Source: U.S. Bureau of Labor Statistics/University of Michigan/U.S. Energy Information Administration/S&P Dow Jones/U.S. Bureau of Economic Analysis/Coresight Research[/caption]

Consumers continue to show a preference for experiences, and particularly upgrading living conditions, as shown in Figure 3. This trend has existed for several years and is likely to persist, as it aligns with the preferences of millennials, whose incomes are increasing and therefore having an increasing influence on the consumer economy.

Competitive Landscape

Market Shares

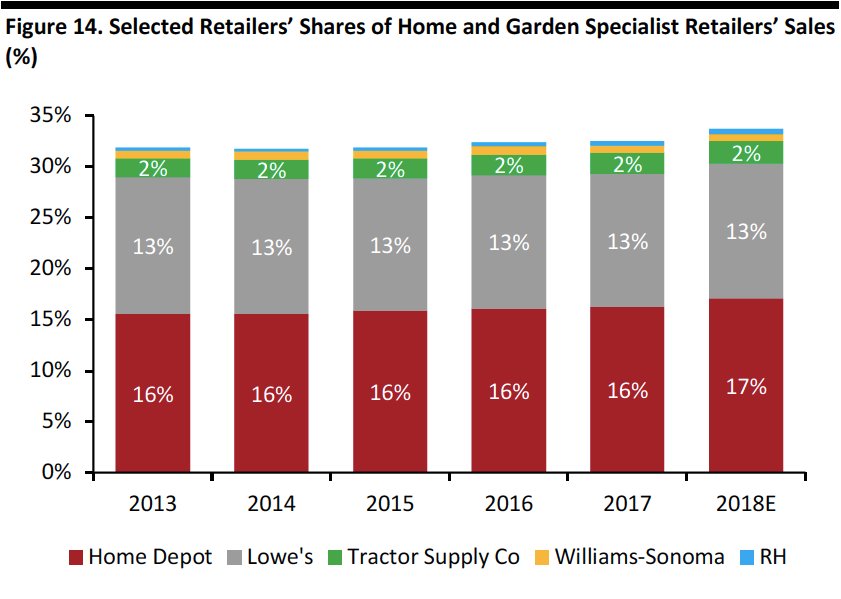

The graph below shows changes in market share during 2013–2018E for selected major retailers in the home and garden specialist sector, according to Euromonitor.

The graph shows the dominance of the top three retailers — Home Depot, Lowe’s and Tractor Supply — with Home Depot the largest and gaining share.

[caption id="attachment_72156" align="aligncenter" width="580"]

Source: U.S. Bureau of Labor Statistics/University of Michigan/U.S. Energy Information Administration/S&P Dow Jones/U.S. Bureau of Economic Analysis/Coresight Research[/caption]

Consumers continue to show a preference for experiences, and particularly upgrading living conditions, as shown in Figure 3. This trend has existed for several years and is likely to persist, as it aligns with the preferences of millennials, whose incomes are increasing and therefore having an increasing influence on the consumer economy.

Competitive Landscape

Market Shares

The graph below shows changes in market share during 2013–2018E for selected major retailers in the home and garden specialist sector, according to Euromonitor.

The graph shows the dominance of the top three retailers — Home Depot, Lowe’s and Tractor Supply — with Home Depot the largest and gaining share.

[caption id="attachment_72156" align="aligncenter" width="580"] Source: Euromonitor International/Coresight Research[/caption]

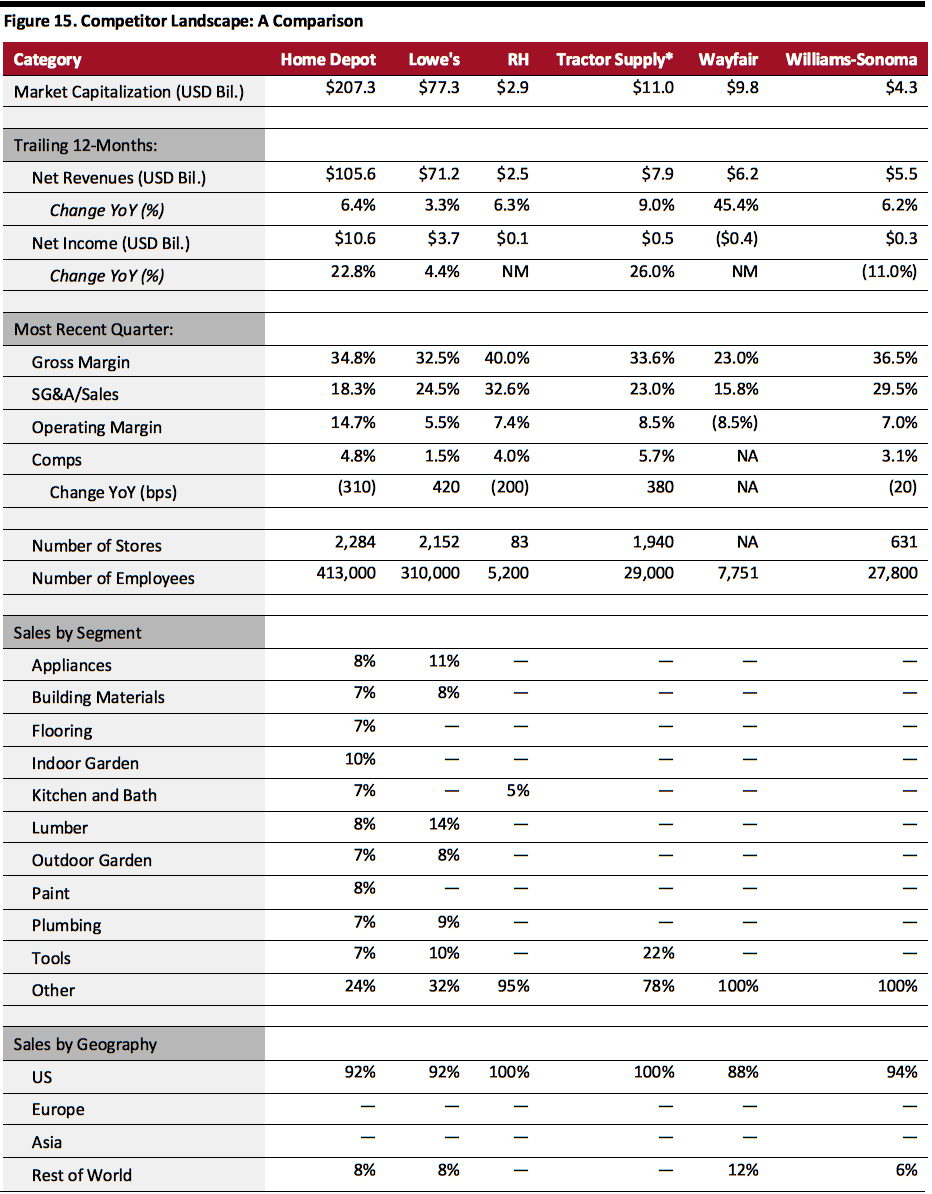

The table below evaluates retailers covered in this report based on revenues, margins, net income, comps and compares their sales by segment and geography.

Company Summaries

[caption id="attachment_72158" align="aligncenter" width="800"]

Source: Euromonitor International/Coresight Research[/caption]

The table below evaluates retailers covered in this report based on revenues, margins, net income, comps and compares their sales by segment and geography.

Company Summaries

[caption id="attachment_72158" align="aligncenter" width="800"] *Quarter ended December 29, 2018; other companies have not reported.

*Quarter ended December 29, 2018; other companies have not reported.

Source: Company reports/S&P Capital IQ/Coresight Research[/caption] Innovators and Disruptors While a public company, Wayfair is a disruptor in the furniture market with its online business model. As in many other sectors, large e-commerce companies such as Amazon are aggressively increasing furniture offerings, and other large retailers with a substantial online presence are expanding online furniture offerings as well. Other potential competitors include:

- A discussion of key sector themes.

- A review of retail sector momentum.

- A summary of the sector landscape, including market shares for the top retailers in their respective categories.

- Outlook for the sector.

Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

Has US Consumer Confidence Peaked?

The University of Michigan Consumer Sentiment Index has been on the rise, after dipping to a relative trough of 55.8 in August 2011. However, the index appears to have peaked, having declined for the last three consecutive months and has failed to set new highs following a relative high of 101.7 in October 2017.

[caption id="attachment_72119" align="aligncenter" width="580"] Source: University of Michigan[/caption]

Home Improvement Leads Retail Growth

In the first 10 months of 2018, two of the three strongest retail sectors year over year were furniture and building materials and garden equipment, according to data from the U.S. Census Bureau, as shown in the figure below.

[caption id="attachment_72124" align="aligncenter" width="580"] Source: U.S. Census Bureau[/caption]

Data on Housing Permits, Starts and Completions Are Mixed but Remain at a High Level

Data on new housing permits, starts and completions offer mixed results, with housing permits up year over year and starts and completions down year over year. Still, this is relatively good news, since permits are the gating factor for a housing start or completion.

Authorized housing permits increased 5.0% month to month in November and 0.5% year over year, according to U.S. Census Bureau data. Housing starts increased 3.2% month to month but declined 3.6% year over year. Similarly, housing completions increased 0.4% month to month but declined 3.8% year over year.

[caption id="attachment_72126" align="aligncenter" width="580"] Source: U.S. Census Bureau[/caption]

Growth Rate of Spending on Home Improvement Is Expected to Slow

Annual growth in national spending on home improvement and repair is expected to decelerate in 2019, due to rising mortgage interest rates and flat home sales activity, according to the Joint Center for Housing Studies of Harvard University. Despite this deceleration, other indicators such as home prices, permit activity, and retail sales of building materials are expected to continue to strengthen and drive continued increases in spending in 2019.

[caption id="attachment_72127" align="aligncenter" width="580"] Source: Joint Center for Housing Studies of Harvard University[/caption]

Total Home Equity Loans Still Declining from Peak in 2009

Total U.S. home equity loans are down 43% from the peak of more than $611 billion in May 2009, reflecting lower debt levels among U.S. homeowners but offering additional firepower for future home improvements. Total U.S. home equity loans are shown in the figure below.

[caption id="attachment_72130" align="aligncenter" width="580"] Source: Board of Governors of the Federal Reserve System (U.S.)[/caption]

Slowdown in US Existing Home Sales Accelerates

Following nine consecutive months of declines, the fall in pending new home sales deepened further in the last months of 2018. The slide is likely due to high home prices and higher mortgage rates, keeping potential buyers on the sidelines. This could also dampen demand for home renovations and improvements.

[caption id="attachment_72134" align="aligncenter" width="580"] Source: National Association of Realtors[/caption]

US Home Prices Exceed Pre-Global Financial Crisis Levels

In the first 11 months of 2018, U.S. home prices, based on the S&P/Case-Shiller index, were up 5% and exceeded the pre-Global Financial Crisis (GFC) peak in January 2017.

[caption id="attachment_72136" align="aligncenter" width="580"] Note: Index Jan 2000=100; not seasonally adjustedSource: S&P Dow Jones Indices [/caption] Lowe’s Management Change and Reboot Promise Operational Improvements and Modernization Lowe’s experienced a complete change of senior management in 2018, with Chairman, President and CEO Robert Niblock announcing his retirement in March 2018, followed by CFO Marshall Croom in June 2018. Marvin Ellison, the company’s new President and CEO, has more than 30 years of retail experience, including stints as Chairman and CEO of JCPenney (where he is credited with achieving a turnaround), in addition to 12 years at Home Depot, including serving as Executive VP of U.S. stores during 2008–2014. David Denton was named CFO in August 2018. Upon assuming his new position, Ellison undertook a detailed reassessment of the business and started implementing process and technology improvement strategies in the following areas:

- Engage customers

- Drive merchandising excellence

- Deliver a seamless, omnichannel experience

- Maximize operational efficiency

- Total sales growth of 2% (versus 4% in 2018)

- Comp growth of 3% (compared to 2.5%)

- Operating margins to increase 235–250 basis points (compared to a decrease of 135–150 basis points)

- Adjusted EPS of $6.00–$6.10 (versus $5.08–$5.14), an increase of 17%–20%

Note: LTM represents last 12 months through Sept. 30, 2018Source: S&P Capital IQ[/caption] The lack of profitability is not an issue itself, though a lack of liquidity could limit the company’s flexibility. That said, capital markets remain open: Wayfair raised $319 million in its IPO and sold $375 million of convertible notes in September 2017. Moreover, there is more to the picture than just net income: Wayfair generated positive cash flow from operations for the past five years and the first three quarters of 2018. [caption id="attachment_72141" align="aligncenter" width="580"]

Note: LTM represents last 12 months through Sept. 30, 2018Source: S&P Capital IQ[/caption] Sector Momentum Sector Size and Growth The U.S. retail market was estimated at $3.3 trillion in 2018 and is expected to grow at a 4.9% CAGR during 2018–2023, with internet-based retail raising the aggregate average, according to data from Euromonitor International. During this period, the home and garden specialist sector is forecast to grow at a slightly slower 4.4% CAGR. [caption id="attachment_72144" align="aligncenter" width="580"]

Source: Euromonitor International/Coresight Research[/caption]

The graph below includes data for U.S. furniture store and building materials/garden equipment retail sales, which together amounted to nearly $500 billion in 2017 and grew at a 5.6% CAGR during 2013–2017. For 2018, we show data for the first 10 months.

[caption id="attachment_72146" align="aligncenter" width="580"] Source: U.S. Census Bureau/Coresight Research[/caption]

Headwinds and Tailwinds

Sector Headwinds

- The main headwind for the segment consists of the dynamic between interest rates and the U.S. housing market. The data in Figure 4 show a flattening of the housing start market, and the data in Figure 7 show a decline in housing sales, as investors are hesitating to rush in alongside higher home prices and rising interest rates.

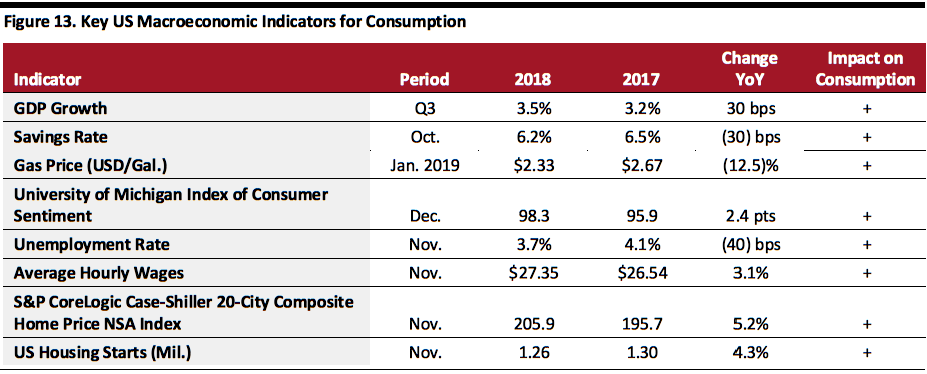

- U.S. macroeconomic drivers remain generally strong for consumption, and the only negative — gasoline prices — is benign as shown by the abundance of positive factors in the table below.

Source: U.S. Bureau of Labor Statistics/University of Michigan/U.S. Energy Information Administration/S&P Dow Jones/U.S. Bureau of Economic Analysis/Coresight Research[/caption]

Consumers continue to show a preference for experiences, and particularly upgrading living conditions, as shown in Figure 3. This trend has existed for several years and is likely to persist, as it aligns with the preferences of millennials, whose incomes are increasing and therefore having an increasing influence on the consumer economy.

Competitive Landscape

Market Shares

The graph below shows changes in market share during 2013–2018E for selected major retailers in the home and garden specialist sector, according to Euromonitor.

The graph shows the dominance of the top three retailers — Home Depot, Lowe’s and Tractor Supply — with Home Depot the largest and gaining share.

[caption id="attachment_72156" align="aligncenter" width="580"] Source: Euromonitor International/Coresight Research[/caption]

The table below evaluates retailers covered in this report based on revenues, margins, net income, comps and compares their sales by segment and geography.

Company Summaries

[caption id="attachment_72158" align="aligncenter" width="800"] *Quarter ended December 29, 2018; other companies have not reported.Source: Company reports/S&P Capital IQ/Coresight Research[/caption] Innovators and Disruptors While a public company, Wayfair is a disruptor in the furniture market with its online business model. As in many other sectors, large e-commerce companies such as Amazon are aggressively increasing furniture offerings, and other large retailers with a substantial online presence are expanding online furniture offerings as well. Other potential competitors include:

- Houzz, which operates a platform that connects homeowners, home design enthusiasts, and home improvement professionals globally. Local businesses and national brands can offer advertising on its platform, and professionals can increase their online presence with professional profiles.

- Thumbtack operates a U.S. online marketplace to hire workers for painting, remodeling and a variety of other tasks.