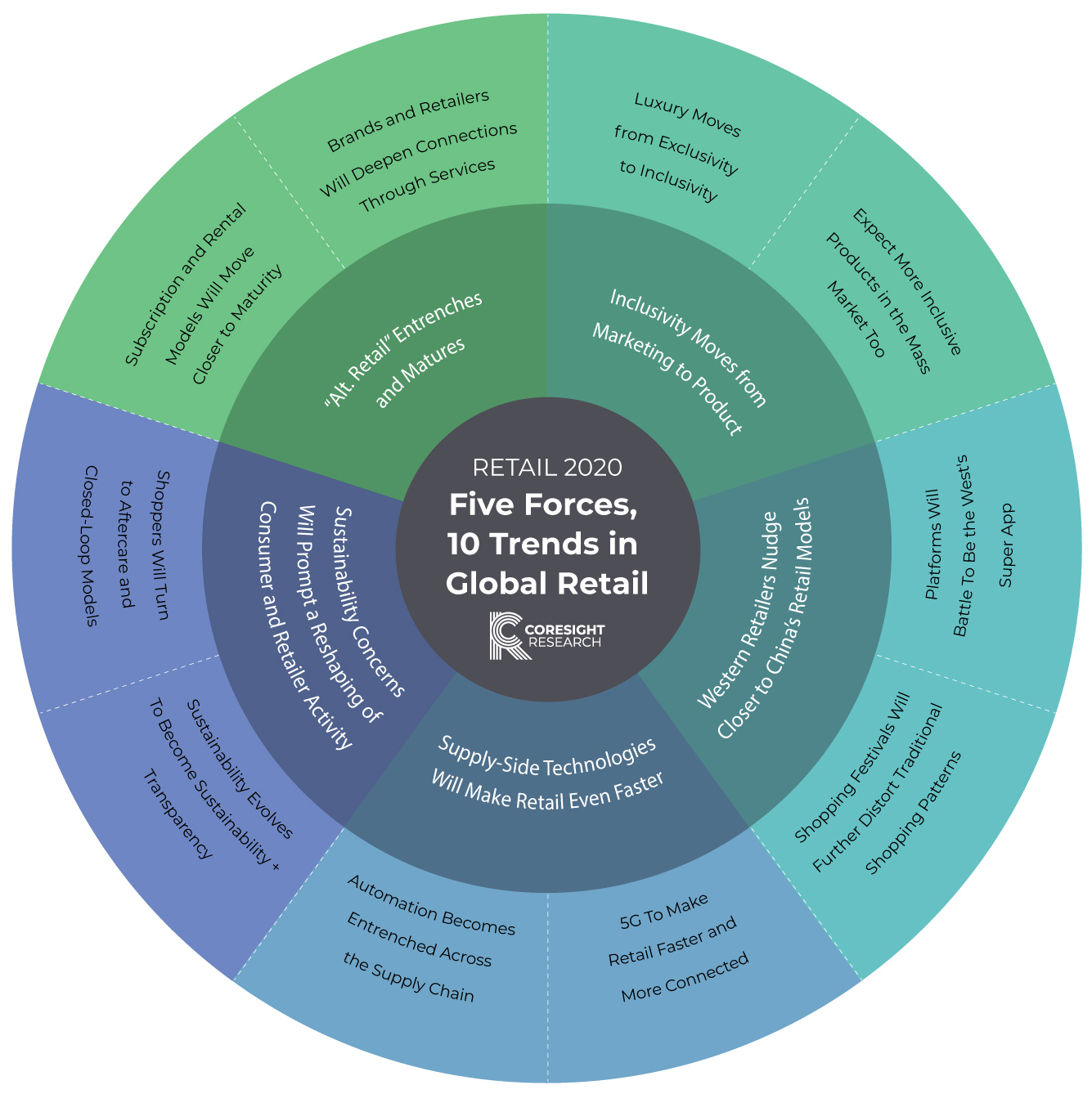

Introduction: 10 Trends for 2020

In 2020, evolving consumer preferences, shifting retail models and improved technical capabilities will drive change in global retailing. In this report, we identify five forces and 10 trends that will help reshape the future of retail in the year ahead.

We have been watching some of these forces—such as sustainability and alternative retail models—for some time. While they are not new, what is new is that they have reached new stages of maturity: We see 2020 as a potential inflection point for some of these medium-term or slow-burning forces in retail.

These are our five forces and 10 trends:

[caption id="attachment_102487" align="aligncenter" width="700"]

Retail 2020: Five Forces and 10 Trends in Global Retail by Coresight Research[/caption]

Plus Four Rollovers from 2019

We also note four trends that we identified for 2019 that we expect to continue to be highly relevant in 2020:

- Expect to see more spectacular retail, with brand-building flagshp stores.

- Physical retail will see more fast retail, with short leases and more pop-up stores.

- Expect more frictionless retail: Retailers will turn to technologies that remove the traditional pain points of brick-and-mortar retail.

- Artificial intelligence will remain retailers’ go-to technology.

1. “Alt. Retail” Entrenches and Matures

Alternative retail models such as rental, resale and service-driven formats are moving retail beyond its traditional focus of selling (new) products. Collectively, we term these “alt. retail.” In 2020, we expect these models not only to expand their reach to more consumers, but also to mature. In particular, we expect to see these two trends:

Subscription and Rental Models Will Move Closer to Maturity

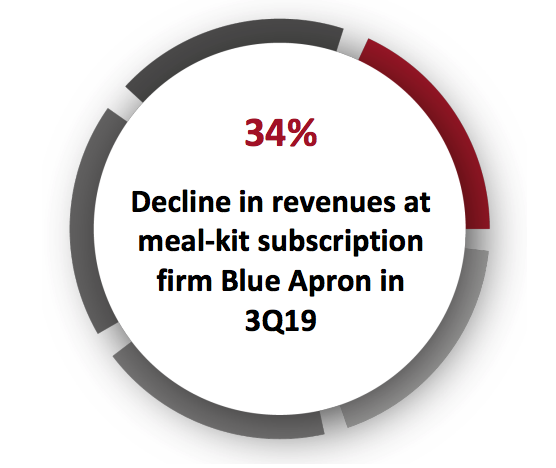

In 2020, we expect rental and subscription models to reach a new level of maturity. That could mean consolidation of the market through a shakeout, mergers and acquisitions, or retailers that are currently dabbling in subscription or rental to exit. High customer acquisition costs related to customer churn, investments in scaling up, and the costs associated with fulfillment call into question the sustainability of subscription models in particular.

Subscription is already seeing signs of difficulty. In the meal-kits subscription sector, unprofitable Blue Apron has seen sales growth turn deeply negative. And in beauty, Birchbox investors saw their stakes wiped out when the company put itself up for sale in 2018. Given specialist players operating subscriptions at scale have encountered problems, we think retailers that add a subscription service to their regular offerings are likely to confront similar difficulties.

We have seen a number of established apparel retailers launch rental services, but we retain some skepticism that legacy firms will be able to “tack on” a new rental business successfully without major investment in logistics and supply chain. The rental model is fundamentally different than traditional retail—and will require meaningful investment in operations that may, in the end, never scale up.

Given the complexity and cost, we believe it’s more likely established retailers will partner with established rental firms instead of trying to develop their own rental models in house. These partnerships could see rental specialists provide services on a white-label basis for retailers or serve as marketplaces that enable brands and retailers to tap rental demand.

[caption id="attachment_102457" align="aligncenter" width="420"]

Source: Company reports

Source: Company reports[/caption]

Brands and Retailers Will Deepen Connections Through Services

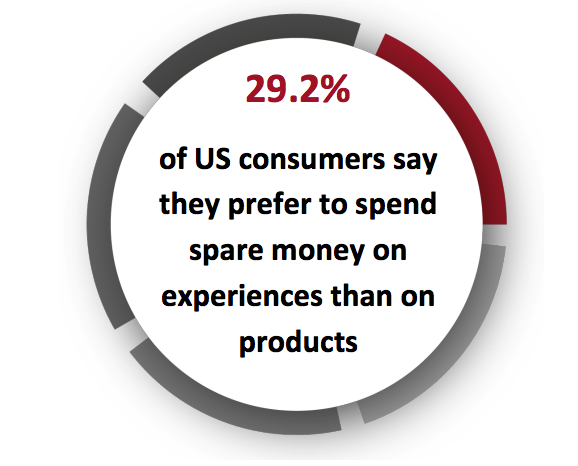

Physical retail is no longer simply about moving product: Today, evolved brands view the store as a marketing channel for brand building. And services are one part of that brand building.

The boundary between retailers and service providers will become even more blurred in 2020. This is about more than legacy retailers adding in-store experiences and leisure services to regain relevance and tap shopper demand for “experiential retail.” The change is about strong brands and monobrand retailers in categories such as apparel, sportswear and beauty cementing their resonance with consumers by moving into adjacent markets.

We have seen a glut of aspirational sportswear brands broaden their offerings—think TorySport offering fitness classes, Lululemon moving into the restaurant business, SweatyBetty hosting wellness discussions and NIKE organizing fitness events. We see opportunities for this trend to trickle down to less elevated brands and to transfer across to brands in other sectors from beauty to food to home goods.

[caption id="attachment_102458" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

2. Inclusivity Moves from Marketing to Product

Brands’ and retailers’ pursuit of greater inclusivity is no longer about just marketing: we’ll see it will manifest in product offerings in 2020. We see this playing out in both luxury and the mass market:

Luxury Moves from Exclusivity to Inclusivity

Luxury is transforming from a culture of exclusivity and uniqueness to one of inclusivity, transparency and egalitarianism. We are seeing this play out not only in marketing but in the types of products being launched by luxury houses. Social values expressed through luxury products now include gender equality, size inclusion, design diversity and selection of ambassadors—although the exclusivity associated with a high price remains.

Diversity is represented in sizes. Online platform 11 Honoré and direct-to-consumer brand Reformation are only two examples of brands pursuing plus-size luxury shoppers.

Gender diversity is in evidence, too, with a number of high-end luxury designers, such as Chanel and Salvatore Ferragamo, designing unisex clothes and products.

In cultural terms, inclusivity includes the moves into streetwear by luxury brands to connect with a younger and more diverse customer base, grooming the next generation of loyal luxury customers. In 2020, we expect luxury brands to continue taking style inspiration from streetwear and skateboard trends, and to incorporate more sporty and casual urban aesthetics into designs.

[caption id="attachment_102459" align="aligncenter" width="420"]

Source: Bain & Co.

Source: Bain & Co.[/caption]

Expect More Inclusive Products in the Mass Market, Too

In 2020, more mass-market brands and retailers will see inclusion not as a marketing add-on, but as shaping the product offering. We envisage growth in niche and tailored segments within apparel and beauty.

Adaptive apparel—clothing and footwear designed for those with disabilities—is one such opportunity. Kohl’s, Target, ASOS and Marks & Spencer have launched dedicated offerings for consumers with disabilities. We expect more retailers to join them in 2020.

Larger women, once marginalized, are now courted by designers, retailers and brands—and plus-size offerings are moving beyond the core apparel staples of jeans, tops and dresses. We have seen companies build out offerings in sportswear, intimates and bridal dresses. These and other niche areas present opportunities for retailers to cater to a still-underserved consumer segment, and capture share in a market that we estimate will be worth around $32 billion in the US in 2020.

In beauty, companies are building out niche categories around life-stage and “age inclusivity,” for example, a new segment in skincare for menopausal women. A 2019 survey by AARP found 70% of women aged 40 and older want more beauty and personal grooming products tailored to perimenopausal or menopausal women, showing there is unmet demand from this demographic.

[caption id="attachment_102460" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

3. Western Retailers Nudge Closer to China’s Retail Models

China leads the world in digitalized retailing, in Alibaba’s “New Retail” model and beyond. Tencent’s WeChat app provides an all-in-one engagement and commerce tool while Alibaba makes online retailing spectacular through its Singles’ Day event. We see these trends and other elements of “New Retail” permeating the West, including through the following two trends:

The Battle to be the West’s Super App

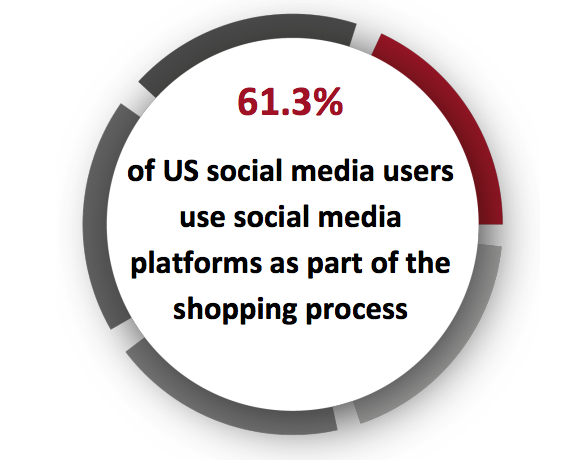

WeChat is China’s super app, enabling instant messaging, posting photos of what users are up to for their contacts to see, making audio and video calls, engagement with brands through WeChat stores, digital payments, sending gifts—and more. In 2020, we expect social platforms in the West to move closer to this model, with social and communications platforms moving closer to the super-app model.

Facebook looks to have a headstart, supported by its ownership of WhatsApp and Instagram. These brands have both been adding features to enable social commerce: WhatsApp now offers a catalog or storefront feature and Instagram now includes a checkout function. Facebook has launched Facebook Pay across its platforms. Meanwhile, Alphabet-owned YouTube has launched shoppable ads.

When Coresight Research surveyed US consumers in November, some 61% of social media users said they use social media platforms as part of the shopping process. In descending order, Facebook, Instagram, YouTube and Pinterest are the top platforms used as part of the shopping journey, according to our survey.

[caption id="attachment_102461" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

Shopping Festivals Will Further Distort Traditional Shopping Patterns

Existing shopping festivals are likely to get bigger, better, more entertaining and more engaging in 2020. Digital-first retailers will continue to take festivals into the “real world” with pop-ups, entertainment events, marketing campaigns and tie-ups with physical stores. For e-commerce retailers that focus more on functional shopping than fun shopping, shopping holidays are an opportunity to build relationships with customers in the real world.

The impact of bigger, more engaging shopping holidays will not only be a short-term boost for the retailers operating the festivals (and possibly a hit to their rivals), but we expect the gravitational pull of festivals to continue the incremental distortion of established shopping patterns. In the US, we have already seen the importance of the traditional holiday season diluted as consumers increasingly shop for the holidays year-round and as events such as Prime Day and Black Friday in July pull forward spending from the year-end peak.

The biggest retailers can create their own shopping holidays, and “own” them the way Amazon owns Prime Day and Alibaba owns Singles’ Day. We also see opportunities to grow existing events, such as Black Friday in July, which is still an emerging event in the US. And, retailers can piggyback on festivals making their way from one region to another: For example, Amazon launched on China e-commerce platform Pinduoduo for Black Friday in 2019—still an emerging event in China.

[caption id="attachment_102465" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

4. Supply-Side Technologies Will Make Retail Even Faster

New and emerging technology (or new and emerging applications of existing technology) will enable retailers to move faster and operate leaner. These are two trends we expect to see in this space:

5G To Make Retail Faster and More Connected

In 2020, 5G will make retail operations and supply chains faster, and support the migration of browsing and buying to mobile devices.

5G technology promises wireless speeds that rival a wired connection, with more capacity and greater responsiveness (lower latency). 5G will offer peak speeds of 10–20 gigabits per second, plus latency—the amount of time between the command and the related action—of less than 1 millisecond and the ability to connect one million devices per square kilometer (the equivalent of 0.39 square miles).

5G will have a significant impact on retail, improving and expanding existing applications and powering new use cases. Applying the technology to retail operations is expected to translate into additional revenue—particularly from e-commerce operations, in which the enhanced connectivity will lead to more straightforward online shopping journeys, but also from more extensive and efficient use of in-store technology, which should also support sale conversion.

[caption id="attachment_102466" align="aligncenter" width="420"]

Source: Adobe Analytics

Source: Adobe Analytics[/caption]

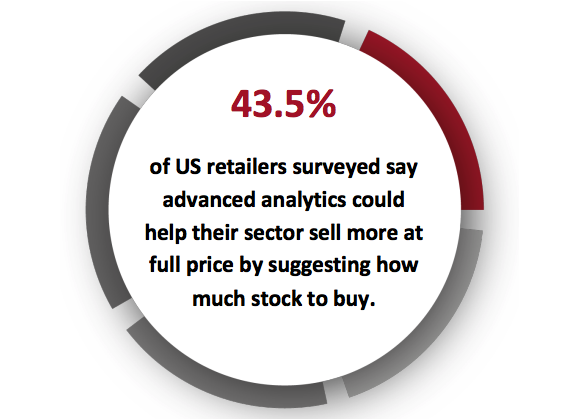

Automation Becomes Entrenched Across the Supply Chain

Analytics, automation and robotics will become more prevalent in manufacturing, logistics and stores, as legacy firms continue to turn to new technologies to move faster and offer greater differentiation. Digitalizing the supply chain is not new, but we will see it at greater scale in 2020.

Manufacturing will become incrementally more automated and data driven, enabling and encouraging greater onshoring and near-shoring of production in industries such as apparel.

Robotics and artificial intelligence will further embed themselves in logistics operations, powering a further acceleration in distribution and delivering operational efficiencies. Advanced analytics will play an increasing role in anticipating and responding to demand across the retail supply chain.

Retailers will continue to embed technology in stores—but selectively. Robotics in stores has gone beyond gimmick-driven customer service-focused trials to focus on bottom-line gains such as in inventory management. And retailers—especially those in nondiscretionary categories such as grocery—will continue to turn to customer-facing technologies to reduce friction in the shopping process, especially at checkout.

[caption id="attachment_102467" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

5. Sustainability Concerns Will Prompt Incremental Reshaping of Consumer and Retailer Activity

We have seen sustainability grow in significance for a few years: it is a slow-burning trend that is incrementally impacting retail. In 2020, we expect awareness of sustainability—by companies and consumers—to continue to impact retail.

These are two of the ways we expect it to play out:

Sustainability Evolves To Become Sustainability + Transparency

In 2020, brands and retailers will provide more detail on the sourcing and composition of products than ever before, as sustainability evolves to become sustainability + transparency. Vague claims about supply chain sustainability will look increasingly insufficient in the eyes of consumers: sustainability will increasingly focus on disclosure.

Already, supply-chain transparency has moved firmly into the mass market, with Amazon publishing details of its private-label suppliers and H&M disclosing information on materials, production country, suppliers and factories for every product it offers.

The implication? Mass-market retailers looking to compete on these terms will need to be equipped with renewed confidence in their supply-chain partners, or risk disclosure backfiring. As mainstream retailers seek to increase disclosure among, they will be prompted to clean up their supply chains and consolidate with best-in-class suppliers.

[caption id="attachment_102468" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

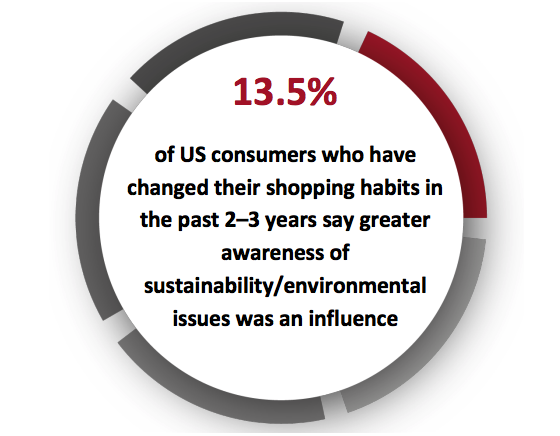

Shoppers Will Turn to Aftercare and Closed-Loop Models

The only truly sustainable shopping behavior is to buy less and, in 2020, we expect more consumers to “walk the walk” by limiting purchases, if even only a little. Just as purchasing preworn apparel has quickly become more mainstream, so we see opportunities for the aftercare segment to grow in scale. In particular, we expect more shoppers to turn to service providers that can revive, mend and restore clothing, footwear and accessories.

Just as retailers have done with clothing recycling programs, resale platforms and a greater focus on sustainable materials, we expect to see retailers partner with service providers to offer apparel aftercare services (tying into our Alt. Retail trend for more service-focused retailing). And the aftercare market dovetails with the adjacent resale market, as shoppers seeking to sell higher-value apparel will see a return on investment in fixing minor problems or restoring luster.

We also expect to see closed-loop models gain in popularity, most notably in apparel. Subscription, membership or leasing programs that let customers return worn clothing for recycling in exchange for fresh garments tap demand for newness and offer a sustainability benefit. And these services will piggyback on growing consumer willingness to adopt “retail as a service” models, where they access products on a subscription basis rather than outright purchase.

[caption id="attachment_102469" align="aligncenter" width="420"]

Source: Coresight Research

Source: Coresight Research[/caption]

And Four To Watch from 2019

We roll over four of our 10 trends from 2019 as we believe they will remain relevant in 2020.

Spectacular Retail

We expect the wave of “spectacular retail” formats to continue. Urban consumers will enjoy access to experience-rich flagship stores offering a huge choice of product and add-ons such as customization and personalization. The emergence of spectacular retail reflects single-brand retailers’ recognition that stores are as much about building the brand as they are about generating sales.

Fast Retail

We think brick-and-mortar retail will continue to become more flexible and faster-changing as retailers and shopping-center owners recognize the need to be more fleet of foot. The “fast retail” trend will manifest as shorter lease terms as retailers seek to avoid being locked in amid a quickening pace of change. We’ll see more pop-up stores—including from digital brands. We’ll also see greater collaboration between retailers, notably sharing space to create traffic-driving synergies, as well as large-stores seeking cotenants to repurpose extra space.

Frictionless Retail

Aiming for frictionless in-store transactions, retailers will turn to technologies that remove the traditional pain points of brick-and-mortar retail. At the vanguard of this shift will be the burgeoning segment of automated, checkout-free convenience stores.

AI Will Continue To Be Retailers’ Go-To Technology

AI will retain its position as the preeminent technological enabler in the retail industry. Retailers will continue to turn to AI—and vendors of services based on AI—to make better decisions on inventory and pricing; to communicate more efficiently and more effectively with customers; and, to personalize offerings. This is not simply about improving customer interactions and data management: AI offers real opportunities to increase operational efficiency through inventory management and price optimization.

For more on what’s coming in retail in 2020, see the Coresight Research reports

Retail 2020: 10 Retail Tech Startup Trends and

Retail 2020: 10 Trends for China E-commerce.