Noting the Impacts of Three Beauty Market Trends

Ahead of the July 29 kickoff of the Cosmoprof North America 2018 beauty trade show, where Coresight Research CEO and Founder Deborah Weinswig will be presenting, we take a concise look at the impacts and implications of three specific developments in the US beauty market:

- The K-beauty boom could be fading as consumers turn their attention to J-beauty, and the shift could impact acquisition targets and innovation cycles.

- Growing demand among male consumers for beauty categories such as skincare suggests that adoption of subtle color cosmetics by younger male consumers could present a substantial opportunity for beauty brands.

- Influencers have established their positions as anchors for collaboration in the beauty market, and we see opportunities for these collaborations to migrate from the mass-market beauty segment to the luxury beauty segment.

J-Beauty Trend Could Slow Product Innovation Cycles as Manufacturers Pursue Quality

K-beauty has been a dominant market trend in recent years, as South Korean brands have flooded beauty stores worldwide with trend-driven, highly innovative and often quirky skincare products. These products have become favorites of beauty shoppers in many countries, not least the US, and the trend has also fueled

acquisitions such as Unilever’s purchase of skincare firm Carver Korea in 2017.

This year, the beauty world has pivoted its attention from Korea to Japan, showing renewed interest in J-beauty, which is less about rapid innovation and creating trends and more about proven efficacy and quality. J-beauty skincare and cosmetics products often incorporate natural or traditional ingredients: they are “not about gimmicks,” Marcia Kilgore, founder of the Beauty Pie brand, told the

Financial Times earlier this year, but “about solid, well-considered, extensively tested technology that stands up to anything.”

- Korea exported $4.2 billion worth of cosmetics in 2016 (latest available data), a 61% increase year over year, according to South Korea’s Ministry of Food and Drug Safety.

- Japan exported $2.6 billion worth of cosmetics (excluding fragrances and haircare products) in 2017, per Japan’s Finance Ministry. Some 90% of these exports went to other Asian countries, suggesting that J-beauty brands have scope to grow demand in the US and other countries outside Asia.

Japanese beauty firms have long held a prominent position in the global beauty market, led by names such as Shiseido, Kosé and Kanebo Cosmetics. Names such as Decorté (owned by Kosé) and Shiro have moved into the US and UK markets only recently, through either distribution deals or by opening their own stores.

We see a couple of notable implications for beauty firms, should there be a sustained market shift away from K-beauty toward J-beauty:

- First, major beauty brand owners would likely turn their eyes from Korea to Japan for acquisition opportunities. We have already likely passed “peak K-beauty,” and brand owners should begin to shift their acquisition focus accordingly, in our view.

- Second, J-beauty implies a slower product development process, and one that focuses on quality, authenticity and efficacy rather than on trends. Should J-beauty become as popular as K-beauty has been, we could see the emergence of “slow beauty.”

Korean beauty products at a Sephora store

Source: Coresight Research

Male Consumers’ Adoption of New Beauty Categories Suggests Incremental Progression Toward Color Cosmetics for Men

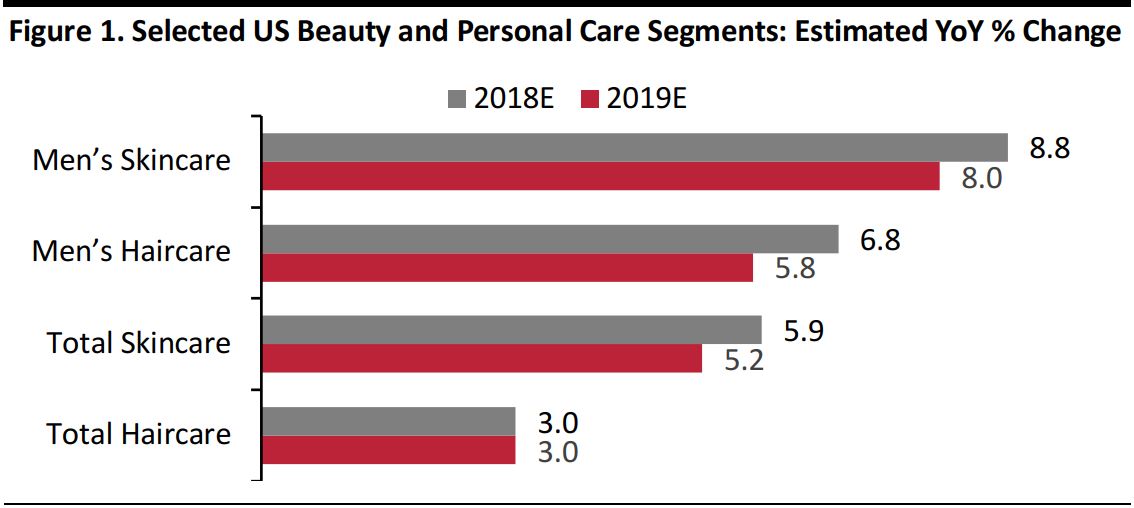

The men’s beauty category is often cited as a high-growth market ripe for beauty brands to tap, as image-conscious male consumers have shown increasing enthusiasm for grooming and beauty product categories. Two pockets of opportunity are the men’s skincare and haircare categories, which look set to grow much faster than the overall skincare and haircare markets, according to data from Euromonitor International. The firm predicts that US men’s skincare sales will grow by a substantial 8.8% this year and that men’s haircare sales will grow by a solid 6.8%.

Source: Euromonitor International

But not all men’s beauty and personal care categories are sure-fire hits— and for every high-growth category, there is a less impressive counterpart. In 2018, Euromonitor expects the US men’s fragrance market to grow by low single digits year over year, the men’s bath and shower products market to grow by only around 5%, and the men’s shaving products market to decline by around 5%. These segments are expected to pull down total growth for the US male grooming market to a mediocre 2.3% for the year.

The general expectation is that saturated, traditional men’s grooming categories, such as soap and shaving products, will grow modestly at best, while categories that have been adopted by men more recently and that function as part of an overall beauty regime, such as skincare, will grow more rapidly.

This trend suggests that men’s makeup is also likely to be a future high-growth category, albeit from a very small base. After all, once men have adopted traditional women’s beauty categories such as moisturizers, antiagers and self-tanners, the next natural step is using corrective or complexion-enhancing color cosmetics. Our own conversations with beauty retail contacts suggest that that color cosmetics that offer subtle enhancements, such as tinted moisturizer, are seeing growing demand from men.

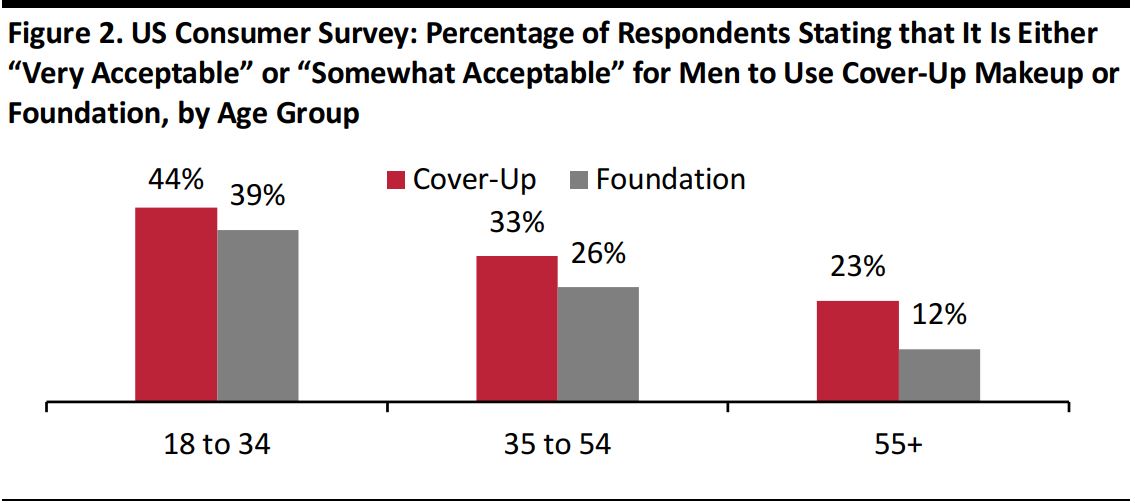

Moreover, a generational shift suggests growth in demand among younger demographics. A YouGov survey carried out in late 2016 confirmed a difference in generational attitudes about men’s makeup: almost half of younger consumers surveyed thought it acceptable for men to wear cover-up makeup, compared with less than one-quarter of those ages 55 or over.

Source: YouGov

The amount of time and money that men of younger generations spend on their personal appearance is growing incrementally, and younger men are embracing grooming and beauty products that older men tend to eschew. Therefore, we think it is only a matter of time before men’s use of subtle corrective or complexion-enhancing makeup becomes relatively mainstream.

Influencers Look Set to Grow Their Impact on the Prestige Beauty Market

Movie stars were traditionally the most powerful group of beauty product endorsers, but social media influencers now hold much sway over the beauty market. The influencers look set to consolidate their power as their impact creeps beyond the mass market and into the luxury segment. Self-made celebrity stylists, bloggers, street-style stars, models and makeup artists who have found fame and built a following through Instagram and YouTube continue to endorse established beauty brands and create new ones in their own name, taking on a role that was traditionally filled by Hollywood stars.

Established and even luxury brands are now working with celebrity and social media influencers to attract younger consumers such as Gen Zers—usually defined as those born in the late 1990s or early 2000s—a demographic group that is highly influenced by social media endorsements.

Activate, a tool for influencers operated by fashion blog aggregator Bloglovin’, surveyed 100 marketers in February 2017 to understand their attitudes toward influencer marketing. Nearly one-third of those surveyed said that they considered influencer campaigns an essential part of their marketing strategy, and 41% said that they had seen more success with an influencer-marketing campaign than they had with traditional campaigns. Approximately 63% of surveyed marketers said that they had increased their influencer-marketing budgets in 2017, and 44% said that they had planned to do so by up to 24%.

According to market research firm The NPD Group, in 2016, prestige makeup launches that involved influencer collaborations generated, on average, twice the sales volumes in their first month as launches that involved traditional celebrity collaborations.

Influencers collaborate with brands in many retail categories, including fashion, but they are most prevalent in the beauty space. Beauty influencers often specialize in a particular product niche, such as makeup or skincare, and often provide educational information about products as well as application tutorials. Influencers’ product mentions in tutorials and social media posts can be either sponsored or organic, and many influencers present certain products as suggested alternatives to prestige products.

Among the notable beauty influencer collaborations are:

- Laura Mercier: Aimee Song, whose Instagram page has 3.6 million followers, was reported to be paid $500,000 in a partnership with beauty brand Laura Mercier.

- Becca Cosmetics: In 2016, a face palette collection launched by influencer and makeup tutor Jaclyn Hill for the Becca Cosmetics brand generated $1 million in sales in 90 minutes, according to Women’s Wear Daily. Hill also won a celebrity makeup artist of the year award.

- BareMinerals: BareMinerals partnered with beauty influencer Ingrid Nilsen, who reportedly received over $500,000 to promote a makeup launch for the brand in 2017.

- Frederic Fekkai: Haircare and hair salon brand Frederic Fekkai has partnered with influencer Teni Panosian to promote its salons and products.

- Maybelline: The L’Oréal-owned Maybelline brand has partnered with one of YouTube’s most-watched beauty influencers, Nikkie de Jager, to host a 10-episode YouTube series for Maybelline’s channel.

Traditionally, high-end designer beauty brands were less keen on being associated with influencers than mass-market brands were, but some are now embracing the marketing strategy. For instance, some Dior product sales have benefited from the support of beauty influencers Manny Gutierrez and Jaclyn Hill, and Dior management acknowledged that there is a highly engaged, highly visible consumer audience for influencers.

We expect to see more premium and luxury beauty brands follow the mass market in working with influencers. After all, millennials and Gen Zers—generations for whom social media is an entrenched part of everyday life—contributed fully 85% of global luxury market growth (all categories) in 2017, according to consultants Bain & Company. Upscale beauty brands will increasingly shift their focus to court and cater to these generations, and they are likely to leverage the power of influencers as part of their efforts.

Key Takeaways

- Any sustained shift in consumer interest away from K-beauty toward J-beauty will likely prompt a change in acquisition targets and slower, more quality-focused product innovation cycles.

- Within the men’s grooming market, the beauty categories that male consumers have adopted more recently, such as skincare, are the categories that are growing the fastest. The progressive adoption of beauty products by men in recent years, coupled with changing attitudes among younger consumers, suggests that we may soon see substantial adoption of selected “low-profile” men’s color cosmetics.

- Social media influencers look set to entrench their strong position in beauty endorsement. In the luxury market, the growing spending power of younger generations that have grown up with social media will likely prompt greater collaboration between upscale beauty brands and influencers.