DIpil Das

Introduction: Price-Conscious Consumers are Underserved by Off-Price Retailers

The German apparel market is famously price sensitive, with a number of domestic discounters being joined by international lower-price retailers such as Primark and H&M. Yet, off-price remains an underdeveloped segment of the market, with only one major player: T.K. Maxx, owned by US-based The TJX Companies and known as T.J. Maxx in the US. In 2019, a potential rival emerged in Karstadt’s Dress-for-less banner. Zalando is increasingly taking its outlet offering offline, too, with six new outlet stores planned by 2020, in addition to its existing five.

Off-price refers to retailers selling a range of branded apparel and other categories (such as homewares or luggage) below regular prices. In Europe, T.K. Maxx is the biggest player in the off-price space.

The Value Apparel Spectrum

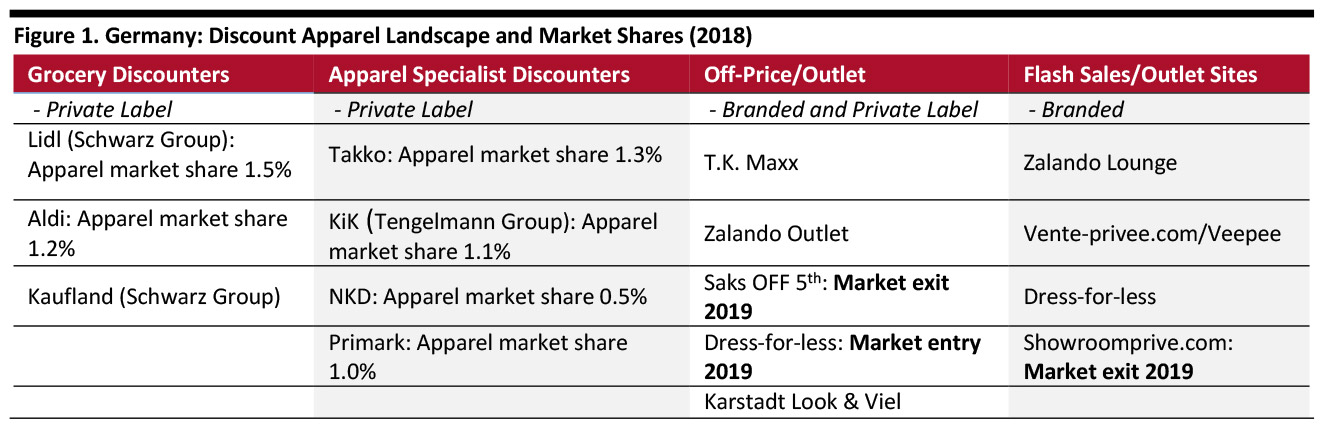

Off-price sits on the spectrum of value apparel options. In Germany, this includes grocery discounters Aldi and Lidl, which feature changing selections of apparel items in their nonfood special buys; domestic and international apparel discounters; and, flash-sales/outlet websites, which, like off-price, provide a channel for excess inventory.

T.K. Maxx’s most significant competitor in brick-and-mortar off-price retail has been Saks OFF 5TH, which entered the German market in 2017 – then exited in 2019 following the combination of Hudson Bay Company’s (HBC’s) department store chain Galeria Kaufhof with rival Karstadt.

[caption id="attachment_93910" align="aligncenter" width="700"] Market share data is for apparel and footwear and represent the share of sales held by retailers’ private labels. Where no figure is provided, market share is not available.

Market share data is for apparel and footwear and represent the share of sales held by retailers’ private labels. Where no figure is provided, market share is not available. Source: Euromonitor International/company reports/Coresight Research [/caption]

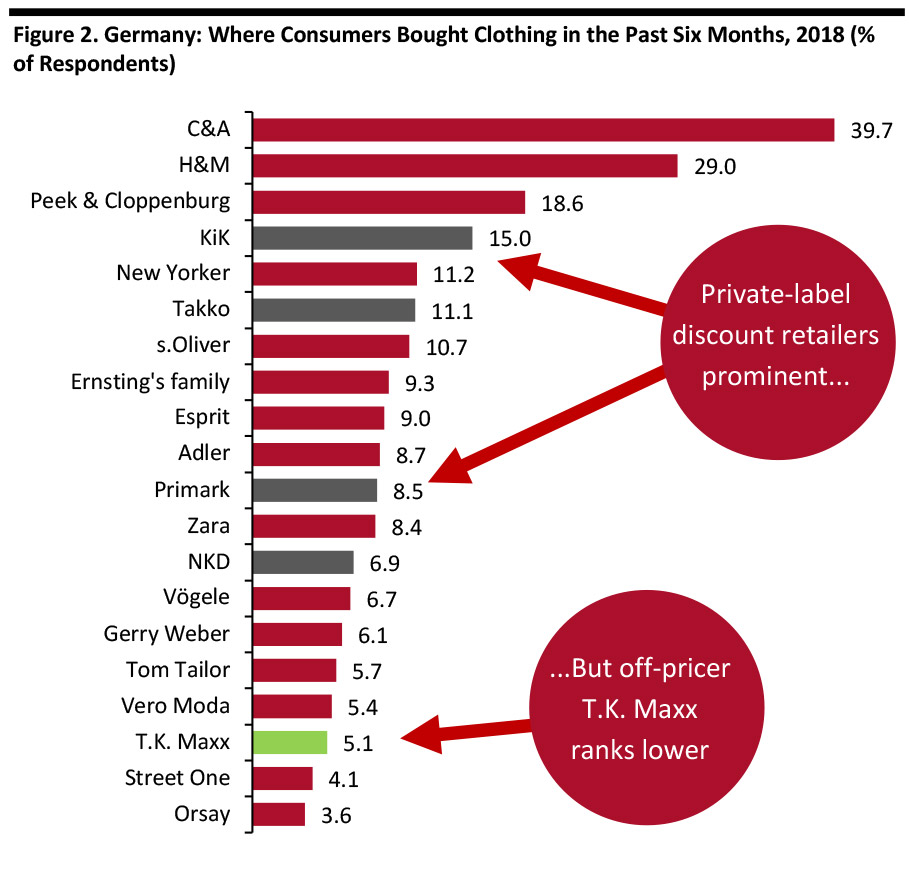

Low-price players are among the most-shopped formats. As shown below, discounters KiK, Takko, Primark and NKD rank prominently by number of shoppers. T.K. Maxx is (just) within the top 20 most-shopped apparel retailers, though only around 5% of consumers have shopped there in the past six months.

[caption id="attachment_93911" align="aligncenter" width="700"] Base: 23,086 respondents ages 14+

Base: 23,086 respondents ages 14+ Source: IFAK/Ipsos/GfK Media and Communication Research [/caption]

Off-Price Sector Momentum and Landscape: T.K. Maxx Retains Market Dominance

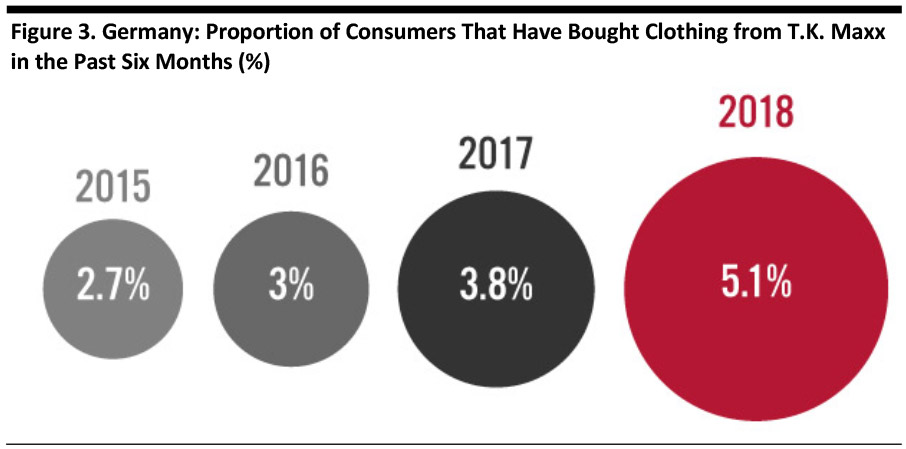

While only around 5% of German consumers had bought clothing from T.K. Maxx in the past six months in 2018, the retailer has been gaining more shoppers: It roughly doubled its apparel shopper penetration rate between 2015 and 2018.

[caption id="attachment_93912" align="aligncenter" width="700"] Base: 23,000+ respondents aged 14 and above in each year Source: IFAK/Ipsos/GfK Media and Communication Research [/caption]

Base: 23,000+ respondents aged 14 and above in each year Source: IFAK/Ipsos/GfK Media and Communication Research [/caption]

Reflecting this, TJX Deutschland, the parent company of T.K. Maxx in Germany, has reported rapid revenue growth. In the four years ended January 31, 2018, the company grew revenues by an average annual rate of almost 17%.

Underpinning this has been an increase in store numbers:

[caption id="attachment_93914" align="aligncenter" width="700"] Fiscal years end in late-January or early-February of the following year. Sales per store is calculated on average annual store numbers.

Fiscal years end in late-January or early-February of the following year. Sales per store is calculated on average annual store numbers. *CAGR is 2013–17 for revenues and sales per store, and 2013–18 for number of stores.

Source: Company reports/Coresight Research [/caption] In TJX’s May earnings call for the first-quarter of fiscal 2020, CFO Scott Goldenberg said:

We are very pleased with the consistency in our comp sales increases throughout all of our UK regions and across Europe. We are convinced that we're capturing significant market shares as other major retailers across Europe report slower sales growth and close underperforming stores.

On the same call, CEO Ernie Herrman said Germany was “very helpful” to the company’s international performance in the first quarter of fiscal 2020.

In the 2020 fiscal year, ending January 2020, TJX plans to open approximately 40 stores in Europe. The company’s European operations now span Germany, the UK, Ireland, Poland, Austria and the Netherlands. As shown above, the company added 11 stores in Germany in the year ended February 2, 2019. The company has previously indicated that it sees potential for 250-300 stores in Germany.

Competitors in Value Apparel

Germany’s substantial value apparel sector includes domestic and international competitors.

Off-Price

HBC launched its Saks OFF 5TH off-price format in Germany in June 2017, representing only the second meaningful off-price banner in Germany. The inaugural German store was a converted Carsch-Haus department store in Düsseldorf. At the same time, HBC management announced further openings in Frankfurt, Wiesbaden, Heidelberg and Stuttgart (all of which were to be converted Sportarena shops) and broached the possibility of opening up to 40 Saks OFF 5TH stores in Germany.

However, in April 2019, the company announced it would close six Saks OFF 5TH stores by June 30, 2019. This followed the merger of HBC’s European business (mainly consisting of Galeria Kaufhof department stores) with the Karstadt department store chain, owned by investment firm Signa.

According to news website Handelsblatt, stores will be converted to a new Dress-for-less format; however, other reports suggest most of the stores will be converted to Karstadt sports stores and Dress-for-less departments will be opened only in existing Karstadt or Kaufhof department stores. Dress-for-less is an online outlet owned by Signa Holding, whose Karstadt department store merged with HBC’s Galeria Kaufhof department store in 2018.

Since September 2017, Signa’s Karstadt has operated Look & Viel outlet departments in Karstadt stores, and these departments will also be converted to the Dress-for-less banner. Dress-for-less will focus less on luxury than Saks OFF 5TH, and more on premium and mainstream brands, according to Handelsblatt.

The launch of the Dress-for-less banner implies T.K. Maxx will face a sustained competitor in the off-price channel, albeit one with few locations initially. However, the Kaufhof-Karstadt merger has created a department store company with 175 stores (according to Euromonitor) – which means Kaufhof-Karstadt could fairly easily roll out more Dress-for-less banners, should the retailer decide to roll out the format across its estate.

Online (to Offline) Outlet Sites

Like off-price stores, flash sale websites offer brands opportunities to dispose of excess inventory.

Zalando Lounge is Zalando’s member-only outlet site. Zalando also operates five outlet stores in Germany, with a further six to be opened by 2020. Zalando Outlet stores and Zalando Lounge comprise the company’s off-price segment, which Zalando says “offers brands additional growth opportunities by providing access to a discount-oriented customer group while maintaining brand equity.” In 2018, this segment reported revenues of €497.5 million (across all markets), suggesting Zalando’s off-price segment is very roughly half the size of T.K. Maxx (with 2017 revenues of €992.8 million). In the first quarter of 2019, Zalando off-price revenues increased 13.6%.

Dress-for-less, discussed above, is an online outlet retailer that was acquired by Signa Holding in 2016. Euromonitor estimates that Dress-for-less held a 0.3% share of online apparel and footwear sales in Germany in 2018.

In January 2019, France-based flash-sales operator vente-privee.com rebranded itself as Veepee and now operates in 14 countries. It says it achieved turnover (including sales tax) of €3.7 billion in 2018, of which 50% came from markets other than France. Euromonitor estimates the company held a 1% share of online apparel and footwear sales in Germany in 2018.

Rival flash-sales site Showroomprive entered the German market in 2014 and exited in 2019.

Private Label

Takko, Kik and NKD are legacy value retailers that sell private-label apparel. According to Euromonitor International data, Takko grew revenues at an average annual pace of 1.0% in the eight years ended 2018, Kik grew revenues by a CAGR of 4.9% over the same period, while NKD saw a revenue CAGR of (1.9)%.

Primark’s expansion in Germany has added capacity to the value private-label segment. However, Primark owner Associated British Foods pointed to a “difficult German market” for the fashion chain in its January 2019 trading update, and noted a decline in comparable sales in the country when it reported first-half results in April. Primark plans to reduce selling space at a small number of stores in Germany to optimize its cost base. Primark had 27 stores as of its latest year-end, in August 2018, up from 22 one year earlier.

Others

Other lower-price players in private-label apparel include H&M (#1 by apparel and footwear market share in 2018, according to Euromonitor) and New Yorker (#12 by market share).

Off-Price and Beauty

Off-pricers such as T.K. Maxx are best known for apparel but sell adjacent categories such as homewares and beauty, too.

T.K. Maxx’s beauty range spans color cosmetics to electrical beauty appliances, and the company likely has opportunities to grow beauty sales from a low base. T.K. Maxx’s parent company does not break out revenues for the category and the company’s breakdown of revenues by broad category suggests that beauty remains a niche part of its business. For 2018, the company stated only that clothing and footwear accounted for 52% of global sales across all its banners, jewelry and accessories 15% and home fashions 33%.

Nor has TJX management provided details to analysts. For example, on a May 2019 earnings call, TJX CEO, President and Director Ernie Herrman told analysts:

As you can see from in the store, we've taken a pretty good position in [beauty]. [But] we don't like to give out future department strategy in terms of what we're thinking of expanding or not until it's a little bit more in the rearview mirror.

According to Euromonitor International, apparel and footwear specialist retailers — the sector in which companies such as T.K. Maxx are categorized — accounted for just 0.1% of beauty and personal care sales in Germany in 2018. This equates to just €11 million of beauty and personal care sales going through all apparel and footwear specialist stores in 2018 — and the majority of these stores will not be off-pricers.

Apparel Market Context: Structural Shifts and Cyclical Factors Prompt Soft Demand at Apparel Stores

German spending on apparel has proven generally weak, albeit interspersed with year-over-year upticks in sales. German consumers’ unwillingness to spend big on clothing and footwear suggests opportunities for off-price retailers — at least among those shoppers looking for branded apparel.

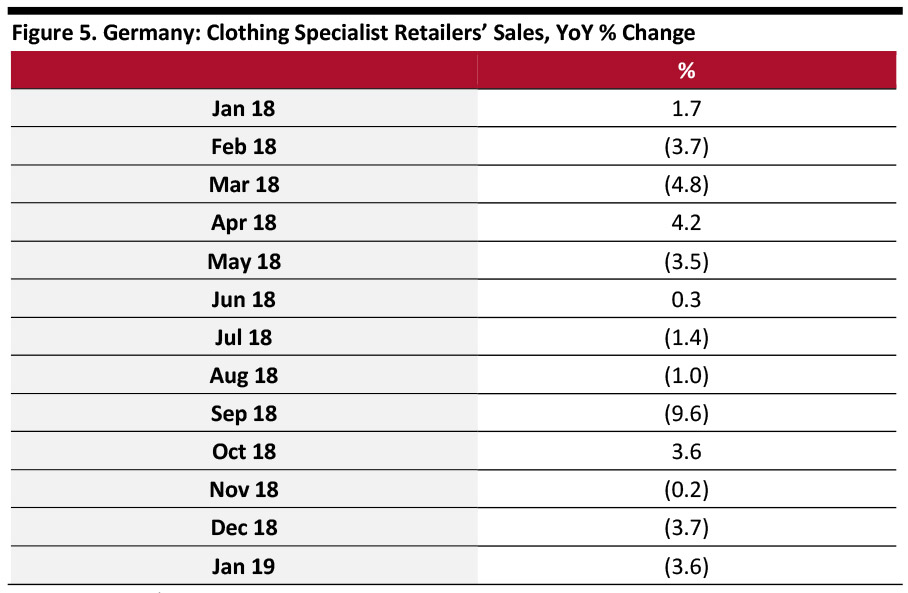

Reflecting soft demand for apparel and structural channel shifts, the clothing specialist sector in Germany has continued to see meaningful declines.

[caption id="attachment_93913" align="aligncenter" width="700"] Source: Destatis/Coresight Research[/caption]

Source: Destatis/Coresight Research[/caption]

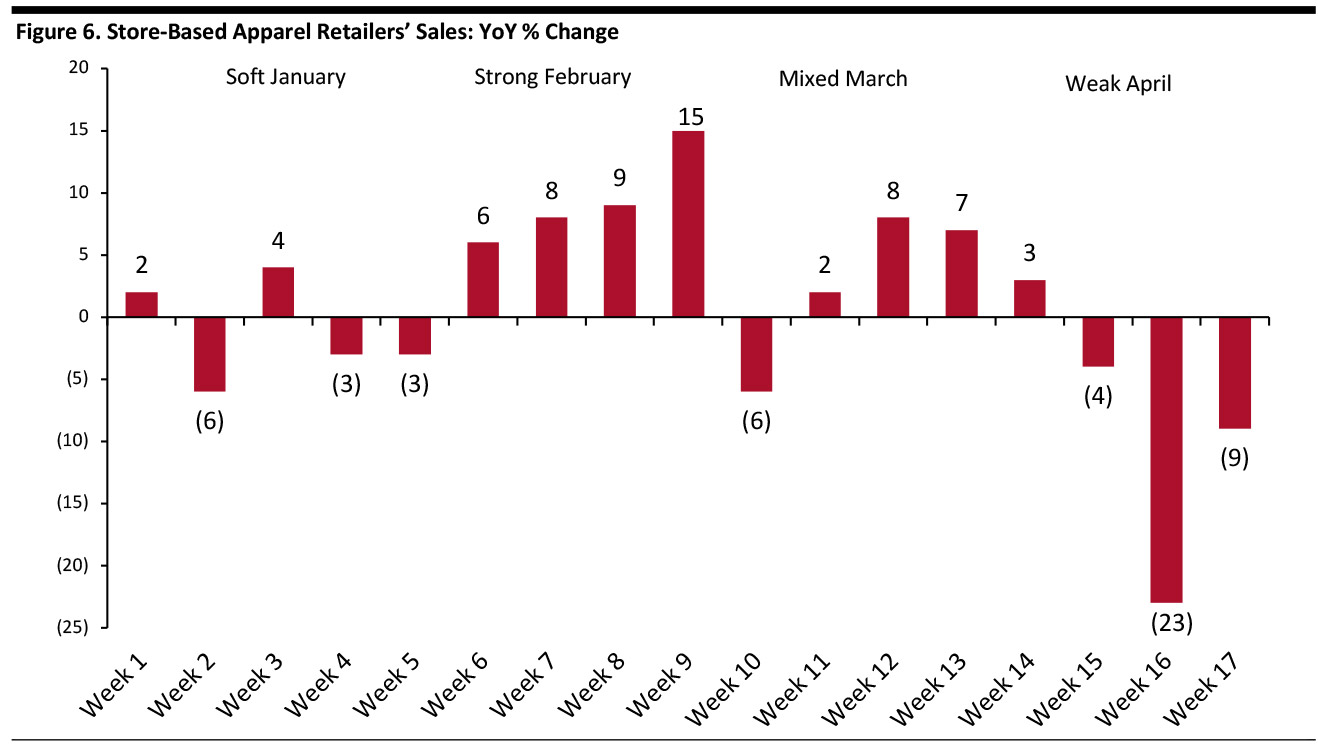

The weekly apparel sales index from trade publication TextilWirtschaft recorded a very weak January in Germany followed by a strong recovery in February (including year-over-year growth of 15% in week 4 of February) followed by a weaker March and April. TextilWirtschaft’s index reflects store-based retailers only.

[caption id="attachment_93915" align="aligncenter" width="700"] Source: TextilWirtschaft[/caption]

Source: TextilWirtschaft[/caption]

High-growth Internet pure plays partially account for this weak sector performance (these pure plays are not included in the sector data for clothing specialists). Yet quarterly consumer spending data confirms sporadic declines in total demand in Germany — as we show below, a year-over-year decline in the third quarter of 2018 was followed by a very modest increase in the fourth quarter.

[caption id="attachment_93916" align="aligncenter" width="700"] Source: Destatis/Coresight Research[/caption]

Source: Destatis/Coresight Research[/caption]

ASOS noted a “challenging performance” in Germany and France in its half-year results, published in April. However, Zalando reported a strong, 20% increase in revenues in the Germany region (which includes Austria and Switzerland) in the final quarter of 2018. As we noted earlier, Primark has pointed to soft German demand.

We do not expect to see a sustained near-term reversal of the weakness in apparel demand for two main reasons: First, many younger consumers in Europe appear to have deprioritized spending on apparel. Second, shoppers have an abundance of price-competitive options, both online and offline, that help them cut spending on clothing.

Euromonitor International estimates total apparel and footwear sales in Germany fell 0.4% in 2018 and forecasts growth of 1.9% for 2019.

Beauty Market Context: A Category with Opportunities

Beauty is a more buoyant category than apparel, providing opportunities for off-pricers. According to Euromonitor, total beauty and personal care sales in Germany climbed 2.9% to €17.1 billion (excluding sales tax) in 2018. Euromonitor estimates the overall category will grow a further 2.6% in 2019. Among core beauty categories, Euromonitor estimates that, in 2018, skincare sales rose 5.4%, color cosmetics sales grew 3.2% and male grooming sales fell 0.1%.

Consumer Context: Caution Amid Macro Uncertainties

Apparently alarmed by world events such as Brexit and tariff wars, and in a context of slowly climbing inflation, German consumers retrenched discretionary spending through much of 2018.

In 2018, German GDP rose 1.4%, versus 2.2% in both 2017 and 2016. However, unemployment fell to an annual rate of 3.2% in 2018 versus 3.5% in 2017.

Consumer caution dragged Germany’s economy into a decline in the third quarter of 2018: The country’s gross domestic product contracted 0.2% quarter over quarter in real terms, in part due to a 0.3% contraction in total consumer spending on the same basis. In the fourth quarter of 2018, GDP was flat, quarter over quarter, with the national statistics office noting a slight quarter-over-quarter increase in consumer spending.

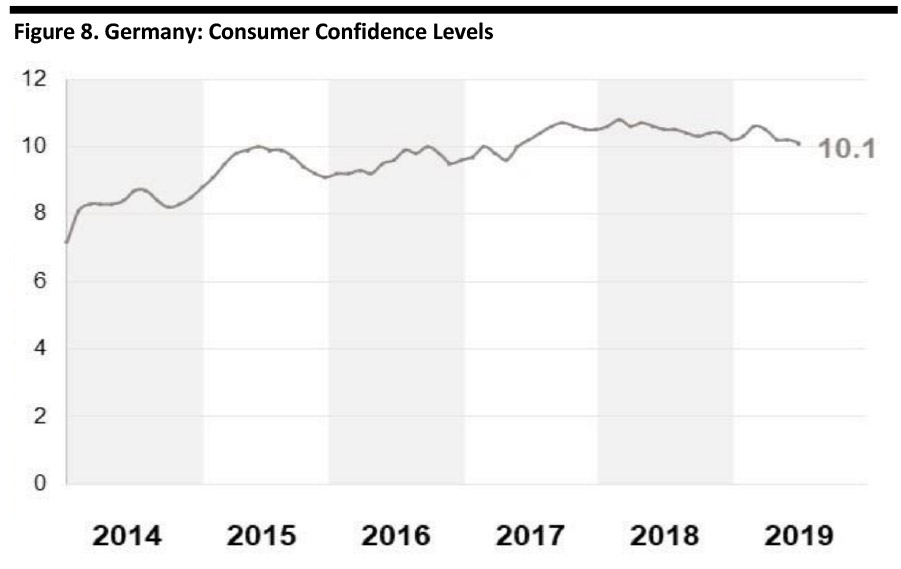

Confirming that shoppers’ caution continues into 2019, research firm GfK has recorded a flatlining, at best, in German consumer confidence so far in 2019. In May, GfK noted that global economic cooling, continued discussions around Brexit, and the risk of an escalation of the trade conflict with the US put a brake on consumer confidence.

[caption id="attachment_93917" align="aligncenter" width="700"] Through May 2019

Through May 2019 Source: GfK, on behalf of the European Commission [/caption]

German consumers are notoriously sensitive to macroeconomic and political events — in fact, the prospect of Brexit appears to be impacting German shoppers’ behavior much more than that of their British peers — and there has been a consequent cyclical pullback in German consumer spending. German retail is likely to remain sluggish until we see greater security and certainty in world and European affairs.

Key Insights

German mass-market apparel retailing is skewed toward value options. Off-price represents a still-nascent part of this market.

The expansion and revenue growth of the T.K. Maxx chain suggest growing demand for this proposition in the German market, and in 2019, TJX management pointed to strong performance in the market.

T.K. Maxx has hitherto enjoyed virtual dominance of in-store off-price formats in the country — although there are many online outlet competitors. In 2019 the company’s only meaningful store-based off-price rival so far, Saks OFF 5TH, left the market, although Kaufhof-Karstadt will launch a new Dress-for-less format. Kaufhof-Karstadt operates 175 stores, suggesting Dress-for-less has room to expand, should the retailer decide to roll out these departments across its estate.

Zalando, too, is moving more into brick-and-mortar outlet formats, apparently confirming German consumer demand for off-price branded apparel.