albert Chan

What’s the Story?

The apparel specialty sectors worldwide saw strong post-crisis recoveries in 2021 and we expect some momentum to continue in 2022, particularly in the first half.

In this report, we provide updated outlooks for the apparel and footwear specialty retail sectors in the US, the UK and China in 2022 and beyond, building on our report published in May 2021. We also explore key growth drivers, competitive landscapes, notable retail innovators in the space, and opportunities arising from three key specialty apparel and footwear trends.

Market Performance and Outlook

Global Specialty Apparel Sector: 2022 and Beyond

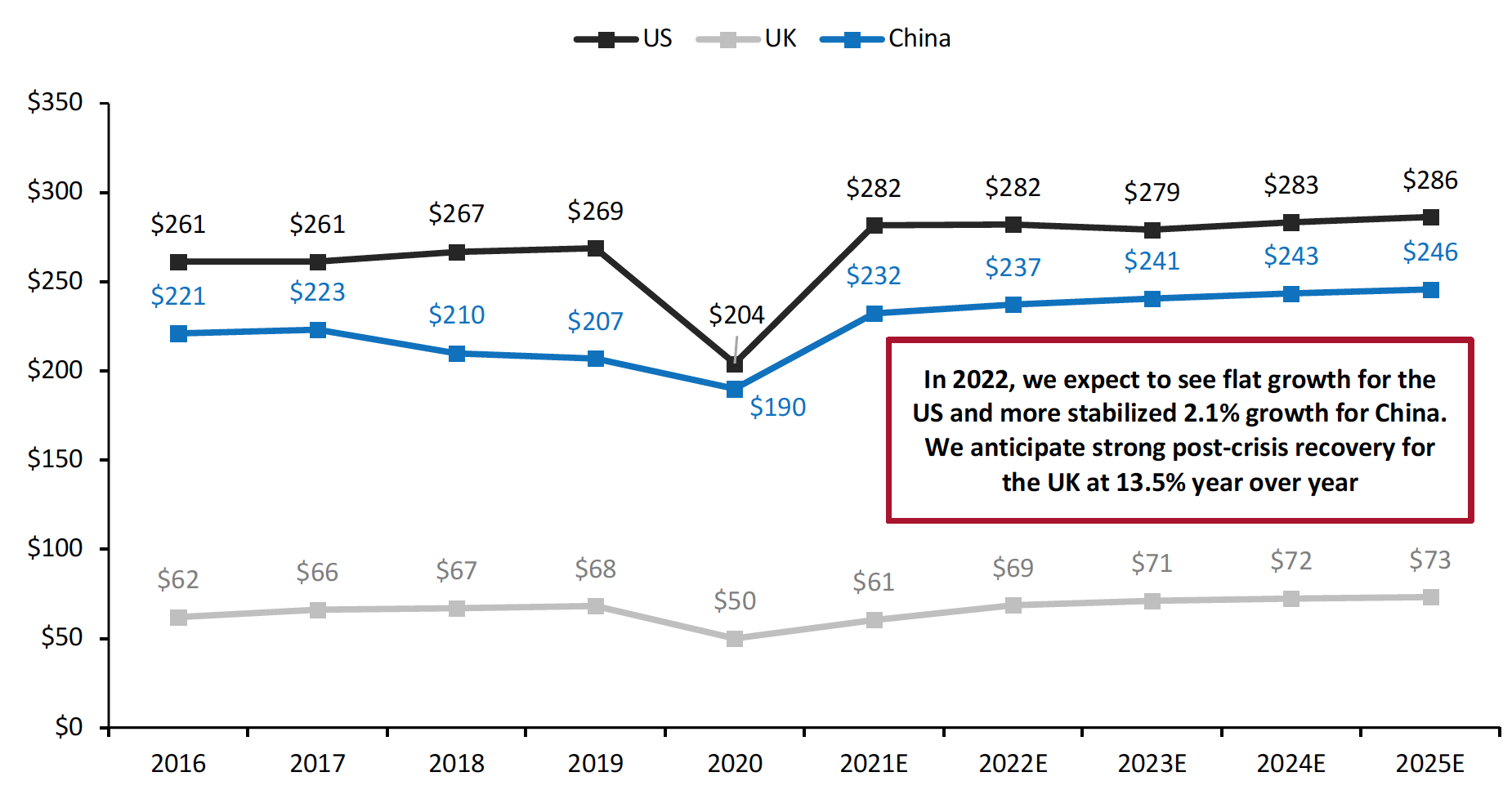

US: In 2021, US clothing and footwear specialists’ sales increased by 38.0% year over year to approximately $282 billion (excluding sales taxes)—around 4.9% above 2019 levels, we estimate using US Census Bureau data. We identify that this was driven by increased vaccinations, economic recovery, stimulus checks and consumers’ return to more normal ways of living and spending. In 2022, against very strong comparatives, Coresight Research estimates that US specialists’ sales will increase by a flat 0.1% growth rate and remain around $282 billion. From 2022 to 2025, we expect the US apparel and footwear specialty sector to witness a sales CAGR of 0.5%.

UK: Apparel and footwear specialists’ sales increased by 21.1% year over year to $60.5 billion (including sales tax and on a constant currency basis) in 2021, but remain 11.0% below 2019 levels, we estimate using Office for National Statistics (ONS) data. We estimate that the sector will see 13.5% growth in 2022, reaching $69 billion, 1.0% above 2019 levels. This will be driven by increased vaccinations and easing of pandemic-related restrictions (which we discuss further in the market drivers section). We anticipate that most of the UK recovery will be in the first half of 2022. The UK apparel and footwear specialty sector will grow at a more stabilized rate, at 2.2% CAGR between 2022 and 2025, we estimate.

China: In 2021, total apparel and footwear specialists’ sales increased by 22.2% to $232 billion (excluding sales tax and on a constant currency basis), we estimate using National Bureau of Statistics of China data, with recovery driven by increased vaccination rollout and consumers returning to more normal ways of living. We forecast that the specialty apparel sector’s growth rate will substantially moderate in 2022, with more stabilized 2.1% growth in 2022—reaching $237 billion. From 2022 to 2025, we expect the China apparel and footwear specialty sector to see a sales CAGR of 1.2%.

Figure 1. US, UK and China: Apparel and Footwear Specialists’ Sales (USD Bil.) [caption id="attachment_137598" align="aligncenter" width="700"]

Source: US Census Bureau/Bureau of Economic Analysis (BEA) /UK ONS/ National Bureau of Statistics of China/Coresight Research[/caption]

Source: US Census Bureau/Bureau of Economic Analysis (BEA) /UK ONS/ National Bureau of Statistics of China/Coresight Research[/caption]

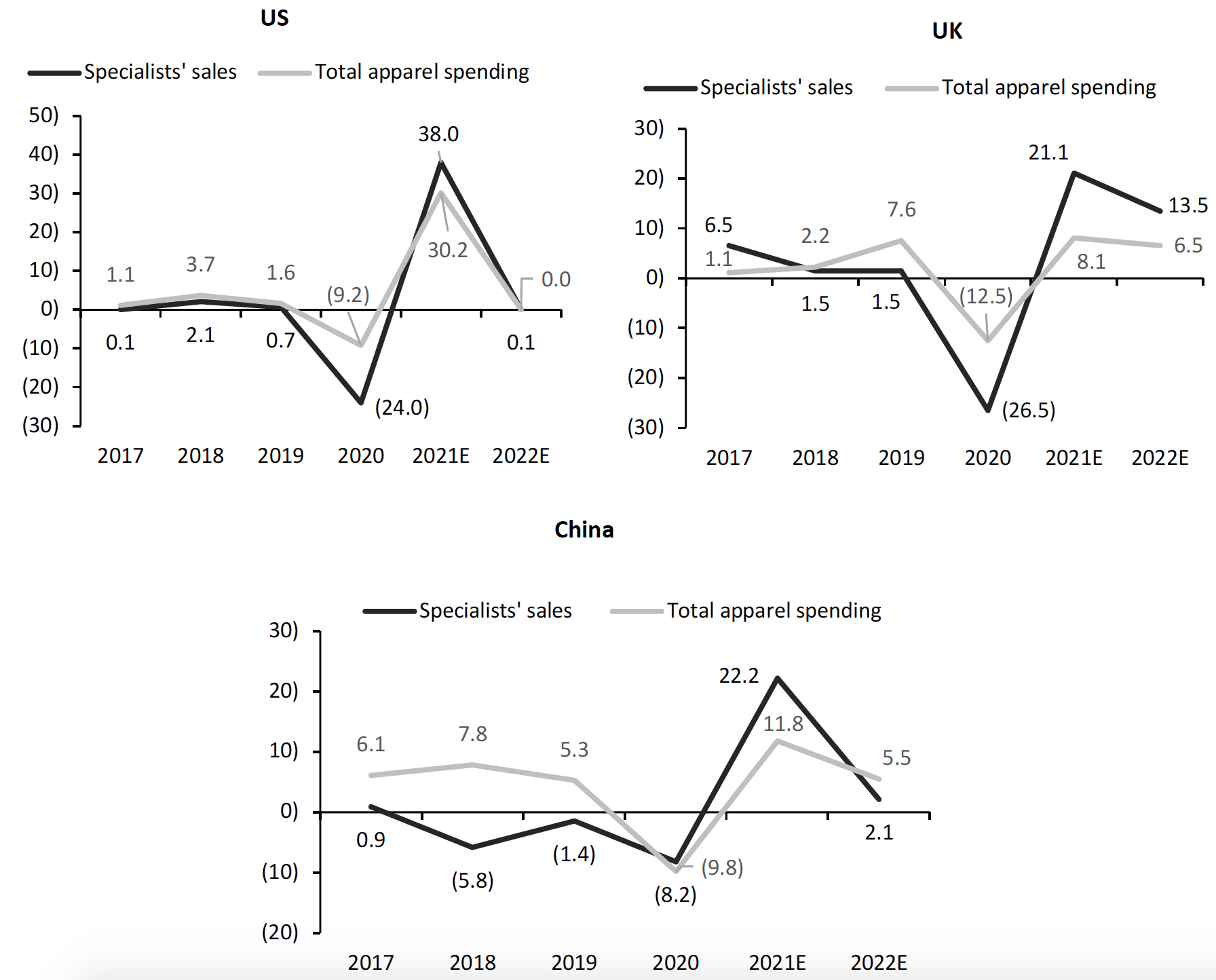

Growth Analysis: Specialists’ Sales Versus Total Consumer Spending on Apparel and Footwear

US: In 2021, specialists saw substantially higher estimated growth than total apparel and footwear spending growth as shoppers returned to stores and specialty retailers recovered ground lost to rival channels in 2020, such as online retailers and mass merchants. In 2022, we expect clothing and footwear specialists to see flat growth, in-line with the growth of total apparel and footwear spending.

UK: Like US apparel specialists, we saw UK specialty retailers’ estimated sales recover at a faster rate than total apparel and footwear spending in 2021. In 2022, we expect specialists’ sales growth momentum to continue and substantially outpace the growth of total apparel and footwear spending.

China: Specialty retailers in China outperformed versus total apparel and footwear spending in 2021. We estimate that clothing and footwear specialists’ sales growth will underpace total clothing and footwear spending growth in the country in 2022.

Figure 2. US, UK and China: Apparel and Footwear Specialists’ Sales Versus Total Apparel and Footwear Consumer Spending (YoY % Change)

[caption id="attachment_137599" align="aligncenter" width="700"] Source: US Census Bureau/BEA/UK ONS/National Bureau of Statistics of China/Coresight Research[/caption]

Source: US Census Bureau/BEA/UK ONS/National Bureau of Statistics of China/Coresight Research[/caption]

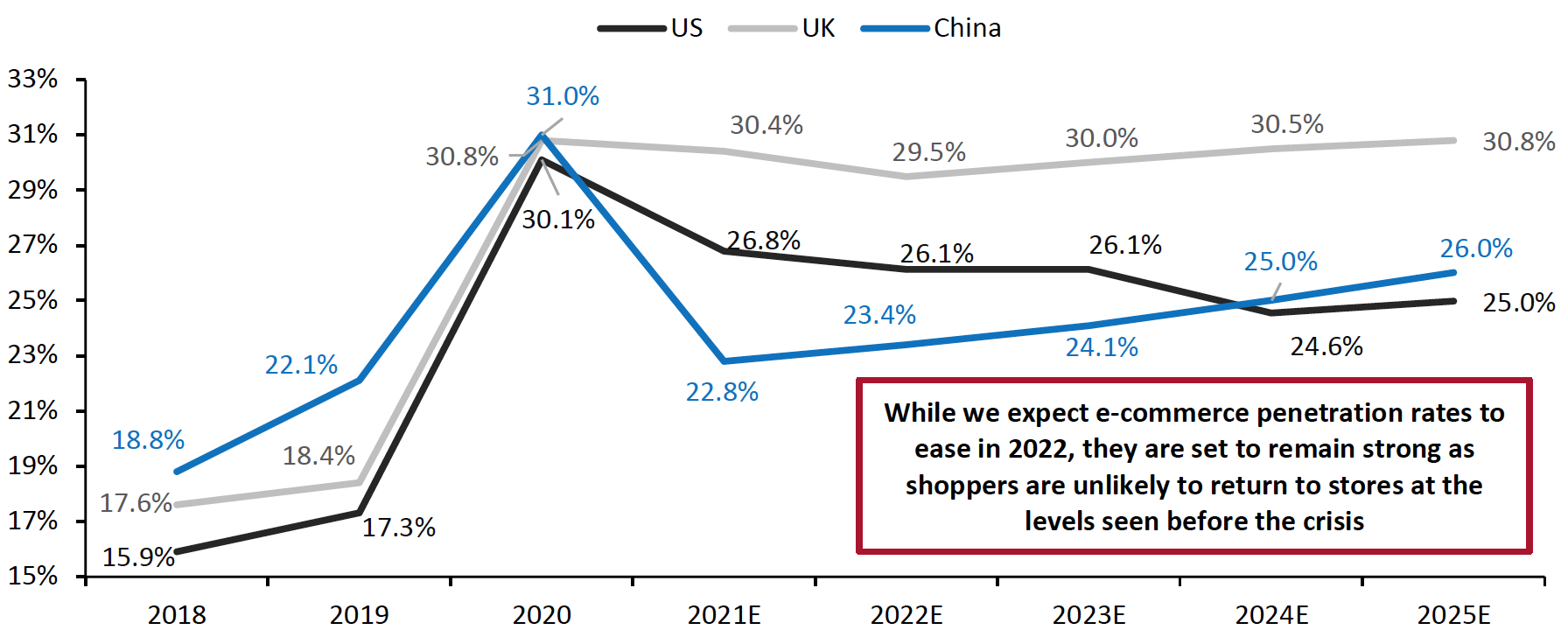

Online Sector Sales

There has been an unprecedented online channel demand surge for apparel and footwear across the globe amid the Covid-19 pandemic. While the 2020 shift to online slightly consolidated in 2021, we expect many apparel consumers to retain the habit of online shopping even after the crisis. We discuss e-commerce penetration for the US, the UK and China in 2021 and our outlook for 2022 and beyond.

US: The e-commerce penetration rate of US apparel and footwear specialists’ sales eased to 26.8% in 2021, from 30.1% in 2020, we estimate using US Census Bureau data. We expect the penetration rate to ease further to a still-strong 26.1% in 2022 on the assumption that shoppers will not return to stores at the levels seen before the crisis.

Major retailers including American Eagle Outfitters, Gap Inc. and Lululemon Athletica, exceed the sector average, which is offset by the performance of less digitally agile retailers. We explore this further in Figure 6.

UK: We expect the e-commerce penetration rate of apparel and footwear specialists’ sales to slightly decrease to 29.5% in 2022, from an estimated 30.4% share in 2021, based on our analysis of ONS data. Although the e-commerce penetration rate among apparel and footwear specialists is set to slightly ease, we expect it to remain higher than pre-crisis levels. We base this assumption on the shift in apparel and footwear shopper preferences toward online shopping and the success of UK-based apparel and footwear e-commerce platforms, such as ASOS and Boohoo, which will likely force specialty retailers to reposition their operations to place more emphasis on e-commerce sales and fulfillment.

While some major retailers, such as Next Plc, substantially exceed the UK sector average for e-commerce penetration, apparel specialist giant Primark has confirmed that it does not intend to operate an online channel despite pandemic-related store closures having cost the retailer an expected £1.1 billion ($1.5 billion) between early 2020 and early 2021.

China: In 2021, many Chinese consumers likely returned to their pre-crisis physical store shopping habits and the overall estimated e-commerce penetration rate eased to 22.8% from 31.0% in 2020, according to Euromonitor. (The National Bureau of Statistics of China does not provide online retail sales data for apparel and footwear specialist retailers).

For 2022, Euromonitor forecasts that the share of e-commerce sales within China’s total apparel and footwear market will slightly increase to 23.4%. While this is well below 2020 levels, the anticipated e-commerce penetration rate marks a slight increase from 2019—indicating continued e-commerce opportunities despite easing in the channel.

Figure 3. US, UK and China: E-Commerce Share of Apparel and Footwear Specialists’ Sales (%)

[caption id="attachment_137618" align="aligncenter" width="700"] For the US and the UK, e-commerce market sizes are represented as a proportion of the apparel and footwear specialists’ sales recorded by the US Census Bureau and the UK ONS, respectively (data post-2020 are Coresight Research estimates). For China, the e-commerce market size is represented as a proportion of the total apparel and footwear market size recorded by Euromonitor as the National Bureau of Statistics of China does not provide absolute numbers for apparel and footwear specialists’ online sales.

For the US and the UK, e-commerce market sizes are represented as a proportion of the apparel and footwear specialists’ sales recorded by the US Census Bureau and the UK ONS, respectively (data post-2020 are Coresight Research estimates). For China, the e-commerce market size is represented as a proportion of the total apparel and footwear market size recorded by Euromonitor as the National Bureau of Statistics of China does not provide absolute numbers for apparel and footwear specialists’ online sales.Source: Euromonitor International Limited 2021 © All rights reserved/US Census Bureau/ONS/Coresight Research[/caption]

Market Drivers

We expect sales in the specialty apparel and footwear sectors in the US, the UK and China to be bolstered by continued strong demand for overall apparel and footwear, which will be driven by four key factors in 2022 and beyond, as detailed in Figure 4.

Figure 4. Key Growth Drivers for Apparel and Footwear Specialists’ Sales in the US, the UK and China

[wpdatatable id=1516] Source: H&M/IMF/ThredUP/UK Office for Budget Responsibility/US Congressional Budget Office/Coresight ResearchCompetitive Landscape

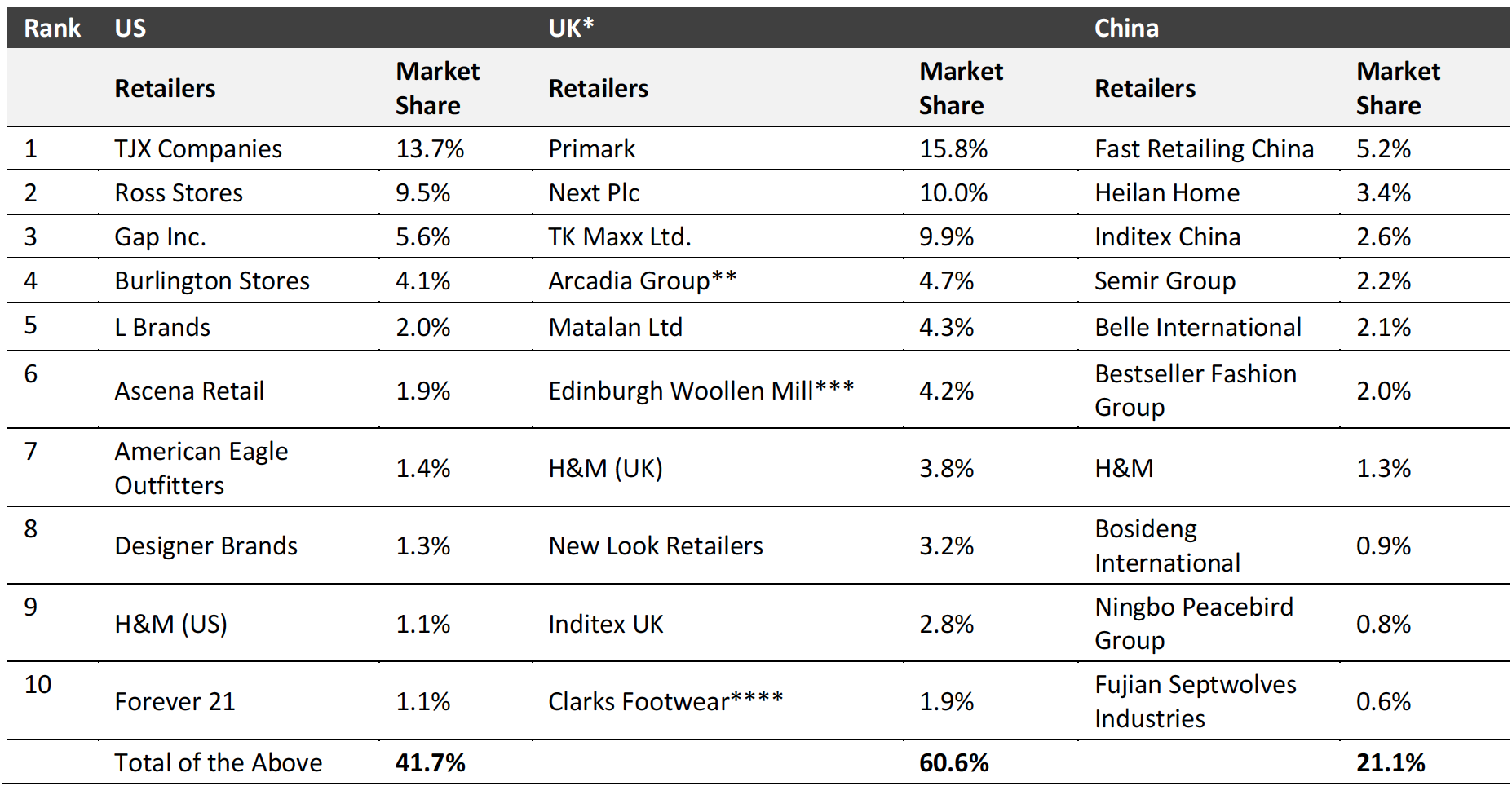

Apparel specialty retail is one of the most competitive industries across the US, the UK and China, with numerous retailers competing for market share. We provide extensive coverage of the key players under our Coresight 100 focus retailers list.

US: The top 10 apparel and footwear retailer specialists accounted for 41.7% of total apparel and footwear specialists’ retail sales in 2020. Off-price apparel specialists, including Burlington Stores, Ross Stores and TJX held dominant positions in the country. International apparel giant H&M was also part of the top 10 apparel specialty retailers in the US by sales in 2020. We provide extensive insight into these retailers under our Coresight 100 coverage.

UK: In 2020, the top 10 apparel and footwear specialty retailers accounted for 60.6% of total sector sales. The UK apparel and footwear retail sector is dominated by both domestic players, such as Primark and Next, as well as international players, including H&M and Inditex.

China: The China apparel retail market is more fragmented than the US and UK markets, with the top 10 apparel and footwear specialty retailers accounting for a 21.1% share of total consumer spending in 2020. International retailers, including Fast Retailing, H&M and Inditex, hold a dominant position in the China apparel retail space, as shown in Figure 5.

Figure 5. US, UK and China: Top 10 Apparel and Footwear Specialty Retailers, by Share of Sector Sales in 2020 (%)

[caption id="attachment_137601" align="aligncenter" width="700"] *Mark & Spencer (M&S) is not included in the UK list because Euromonitor classifies M&S as a department store.

*Mark & Spencer (M&S) is not included in the UK list because Euromonitor classifies M&S as a department store.**Arcadia Group went bankrupt and sold its HIIT, Miss Selfridge, Topman and Topshop brands to ASOS in February 2021 and the intellectual property rights, digital assets and e-commerce rights of its Burton, Dorothy Perkins and Wallis brands to Boohoo.

***Edinburgh Woollen Mill went into administration and was sold to a consortium of international investors in January 2021.

****Clarks Footwear went into administration and sold its majority stake to Hong Kong-based private equity firm Lionrock Capital in November 2020.

Source: Euromonitor International Limited 2021 © All rights reserved[/caption]

Apparel and Footwear Specialty Retailers: Latest Quarterly Growth and Outlook Reports

We present recent quarterly growth numbers for major publicly listed apparel and footwear retailers and summarize key commentary on their future outlook.

Figure 6. Selected Leading Apparel and Footwear Specialty Retailers in the US, the UK and China: Quarterly Sales Growth, E-Commerce Growth, Online Penetration (%) and Key Commentary

[wpdatatable id=1517] Source: Company reports/Coresight ResearchRetail Innovators

Technology innovators are emerging as a significant enabler to apparel and footwear retailers’ push into e-commerce expansion. Through technological innovations, these startups are helping retailers to lower inventory levels and improve efficiency, agility and resilience across their supply chains. We discuss three innovators and their impact on the apparel and footwear specialist market.

1. HeartDubFounded in 2011 and based in Beijing, HeartDub innovates in digitalized fabric and textile technology in the clothing industry. Its artificial intelligence (AI)-driven “physics-engine” collects data on physical fabrics and analyzes structural elements, including colors, designs and patterns, to create “virtual fabrics to be worn by virtual models.” The digital clothing try-on tool is programmed so that the virtual model makes realistic movements, demonstrating how clothes would look on a human body in real life.

The innovation reduces the cost of designing and developing fabrics compared to traditional methods—which typically involves making physical samples and getting approval before closing a contract. The software can thus optimize transactions between apparel manufacturers and specialty retailers.

HeartDub’s solution can cut development production costs by 50% while shortening sample delivery time by 90%, according to CEO Huang Jingshi. The company plans to use its technology to connect more players across the supply chain through online clothing design, virtual try-on functions, digital runway shows, and virtual character creation for games and films, contributing to the digitalization of the apparel industry.

More than eight companies currently use HeartDub services, including France-based fashion company SMCP Group and Chinese textile giant Shandong Ruyi, which owns UK-based luxury fashion brand Aquascutum.

2. NewmineFounded in 2011 and based in Massachusetts, US, Newmine’s Chief Returns Officer, an AI-powered platform, enables retailers to holistically view returns data and provides analysis and prescriptive actions across the value chain.

The Chief Returns Officer platform uses anomaly detection and natural language processing to identify the root cause of returns—generating corrective actions that retailers can take to reduce future returns and empower teams in different departments to collaborate seamlessly. This technology offering aims to improve retailers’ bottom lines by minimizing product returns, which are a significant cost driver across retail—and particularly for apparel and footwear specialists.

In January 2021, Newmine launched KeepScore, a success benchmark that enables retailers to quickly identify their most profitable products, suppliers and customers by understanding which products customers chronically return and which they keep.

3. NexiteFounded in 2017 and based in Israel, Nexite collects and provides real-time in-store data to retailers, helping them to identify which of their products generate the most engagement and the highest conversion rates. Furthermore, Nexite provides data-driven store arrangement insights, thus enabling retailers to manage their omnichannel businesses effectively—which will be crucial for apparel and footwear specialists looking to compete with e-commerce platforms.

Nexite is also working to develop in-home smart closets that can recommend apparel outfits, new purchases and resale options by leveraging the same tags and technology that Nexite uses with its retail partners. Currently, Nexite is conducting a pilot test with a global brand in Tel-Aviv, Israel. According to the company, it also has three upcoming projects set to take place in the US and Europe with some of the world’s largest fashion companies.

[caption id="attachment_137597" align="aligncenter" width="550"] Source: Nexite[/caption]

Source: Nexite[/caption]

Themes We Are Watching

We discuss three key themes that we believe present opportunities in specialty apparel and footwear retail.

1. Demand for Activewear, Athleisure and IntimatesWe have seen strong demand for activewear and athleisure in 2021. For 2022, we expect to see different growth trajectories among apparel and footwear specialists by segment—for instance, retailers that focus on activewear and athleisure, such as Bosideng International, Dick’s Sporting Goods, Foot Locker and Lululemon are showing stronger growth than retailers that mostly focus on general apparel, such as American Eagle Outfitters, Gap Inc., Fast Retailing, H&M and Inditex. Nevertheless, within the abovementioned group, American Eagle Outfitters and Gap Inc., are witnessing strong growth in their activewear and intimate apparel offerings and are looking to expand in these categories.

American Eagle Outfitters’ intimates apparel brand Aerie posted a 34% increase in sales in its second quarter, ended July 31, 2021, which marked 27 consecutive quarters of double-digit growth for the brand. The company aims to double its Aerie banner revenue to $2 billion by 2023.

Gap Inc.’s activewear brand Athleta reported a double-digit increase in sales in its second quarter, ended July 31, 2021. The company continues to expand the banner, with the goal of doubling Athleta sales to $2 billion in 2023 from $1 billion in 2019. This equates to 20.0% of the company's total revenues, up from 12.5% in 2019.

We believe that many apparel and footwear specialists will look to optimize their opportunities within the $21 billion US activewear market.

2. Sustainable SourcingWith increasing pressure from environmental organizations and shifting customer values toward companies they consider more environmentally conscious apparel and footwear retailers are taking proactive steps toward sustainability. We discuss sustainability initiatives from apparel and footwear specialty retailers below:

American Eagle Outfitters: On January 21, 2021, the company set out its goal of being carbon neutral in its company-owned facilities by 2030. Moreover, by 2023, American Eagle Outfitters plans to reduce its water use per pair of jeans by 30% and achieve 100% sustainable cotton sourcing. We see this as a positive move for the company in engaging with today’s fashion shopper.

H&M: In December 2020, H&M Foundation, in partnership with The Hong Research Institute of Textiles and Apparel, announced plans to invest $100 million over five years in the Planet First program, an initiative that works toward finding sustainable solutions for the fashion industry. Moreover, in November 2020, H&M reached a multi-year partnership with Swedish textile recycling company Renewcell to supply H&M with thousands of tons of circulose fibers made from unusable textile waste. This comprises part of the company’s 2030 goal that aims at improving sustainability in its material sourcing.

Inditex: In the company’s annual general meeting in July 2021, Inditex’s Executive Chairman Pablo Isla said that Inditex is bringing its net-zero carbon emissions target forward by 10 years to 2040. Furthermore, Isla highlighted the company’s plans to accelerate delivery of other sustainability targets and introduce new ones, including:

- Inditex aims to convert 100% of its stores and e-commerce websites into “sustainability hubs” by 2022, up from the previously targeted 80%. Under the initiative, the company’s stores and online platforms will use renewable energy, eliminate single-use plastic, incorporate more recycled materials and promote garment reuse.

- Inditex plans to use 100% sustainable fabrics in all of its collections by 2023, two years ahead of its initial target of 2025.

- By 2022, more than 50% of all Inditex’s offerings will carry the company’s Join Life sustainability seal.

- By 2025, Inditex aims to reduce the water impact across its entire supply chain by 25%.

In February 2021, Inditex partnered with Asia-based bank DBS to provide finance to over 2,000 Indian organic cotton farmers in the retailer’s supply chain to bolster sustainable farming practices.

Next Plc: On March 4, 2021, Next joined the US Cotton Trust Protocol as part of its goal to source 100% of its main raw materials from sustainable and responsible sources by 2025. The US Cotton Trust Protocol will provide Next with verified data on the practices used on US cotton farms in six important areas of sustainability: energy use, water use, greenhouse emissions, land use efficiency, soil carbon and soil loss.

We believe that strong sustainability goals and initiatives can help apparel and footwear retailers to attract customers, investors and employees.

3. Increase in M&A ActivityWe expect the wave of apparel and footwear retail disruption and consolidation seen in 2021 to continue in 2022 and beyond, particularly among UK-based apparel companies. We discuss apparel giants that have acquired weakened rivals and added new technologies and consumer segments to reclaim market share lost to innovative startups.

ASOS: The company acquired HIIT, Miss Selfridge, Topman and Topshop brands from UK-based apparel and footwear company Arcadia Group for £265 million ($362 million) in February 2021.

Boohoo: In February 2021, Boohoo acquired the intellectual property rights, digital assets and e-commerce rights of Arcadia Group brands Burton, Dorothy Perkins and Wallis out of administration for £25.2 million ($35.2 million). Boohoo expects the acquisition to grow the company’s market share across a broader demographic, such as in menswear. The acquired brands had over 2 million active customers in 2020. Earlier in January 2021, Boohoo acquired UK-based department store Debenhams from the latter’s administrators for £55 million ($75.4 million). The deal included the department store’s brand assets, e-commerce operations, intellectual property, and own-label beauty and fashion products.

Foot Locker: In September 2021, Foot Locker acquired Eurostar (WSS), a US-based athletic apparel and footwear retailer, for $750 million. Foot Locker’s CEO Richard Johnson said, “WSS brings an expanded and differentiated customer base rooted in the rapidly growing Hispanic community, diversifies and enhances our product mix, and strengthens our footprint with a 100% off-mall store fleet located in key markets.”

In August 2021, Foot Locker entered into a definitive agreement to acquire Japan-based digitally led footwear and apparel retailer Text Trading Company, K.K. (atmos) for $360 million. The company has 49 stores globally, including 39 in Japan, operating under the atmos and atmos pink banners. In fiscal 2020, atmos generated $175 million in revenues, of which over 60% was generated through digital channels. Through this acquisition, Foot Locker is looking to accelerate its global reach with a highly strategic foothold in Japan, while extending Foot Locker’s top-tier and premium offering. Foot Locker’s management said that the acquisition is set to be accretive to Foot Locker’s earnings per share (EPS) in fiscal 2021. CEO Johnson said, “atmos is uniquely positioned through its innovative retail stores, high digital penetration and distinctive products that have made it a key influencer of youth and sneaker culture. With atmos, we are executing our expansion initiative in the rapidly growing Asia-Pacific market, establishing a critical entry point in Japan and benefitting from immediate scale.”

JD Sports: In February 2021, UK-based sportswear retailer JD Sports entered into an agreement to acquire US-based athletic apparel and footwear retailer DLTR for £355 million ($495 million). This followed JD Sports’ acquisition of US-based footwear retailer Shoe Palace for £240 million ($325 million) in December 2021.

Next Plc: On March 10, 2021, Next entered into an agreement to acquire a 25% indirect stake in UK-based apparel retailer Reiss Limited through the purchase of shares from existing shareholders. In its fiscal year ended February 1, 2020, Reiss achieved a turnover of £227 million ($300 million), an increase of 22% from fiscal 2019. Reiss currently operates in 14 countries through 79 stores, 104 concessions, and via wholesale and franchises. In the company’s fiscal 2021 earnings conference call held on April 1, 2021, CEO Simon Wolfson stated that Next is more interested in acquiring minority stakes in a number of independently run businesses than acquiring fewer businesses outright. This strategy will help management to focus on Next operations and reduce the risk of getting sucked into the day-to-day management of acquired businesses.

Moreover, in September 2020, Next announced a joint venture partnership with L Brands. The joint venture will acquire the majority stake in the L Brands’ Victoria’s Secret UK business. Next will own a 51% stake in the joint venture, while L Brands will own 49%. In September 2021, Next finalized a joint venture with Gap for the former to manage Gap’s business in the UK and Ireland as a franchise partner; Next will own 51% of the joint venture.

In addition to acquiring other brands and retailers, apparel giants are also acquiring innovative startups as an additive to their current offerings.

For example, in October 2021, Gap acquired AI and machine learning startup Context-Based 4 Casting (CB4), which utilizes predictive analytics and demand sensing to transform retail operations, enhance the customer experience and boost sales. Sally Gilligan, Gap’s Chief Growth Transformation Officer said, “Gap has experience working with CB4’s world-class data scientists, so we understand the impact and the wide applications their science can have across sales, inventory and consumer insights, as well as its potential to unlock value and enhance the customer experience.”

In addition, in August 2021, Gap acquired the e-commerce startup Drapr, which is built on technology that lets shoppers quickly create 3D avatars and virtually try on clothing. Gilligan said, “Fit is the number one point of friction for customers and, through their advanced 3D technology, Drapr has shown it can help shoppers efficiently find the size and fit they need. We plan to leverage Drapr to help Gap Inc. improve the fit experience for our customers and accelerate our ongoing digital transformation.”

Similarly, in July 2020, Lululemon acquired MIRROR, a US-based livestreaming technology company focused on at-home workouts for $500 million. Lululemon expects at-home virtual workouts to be a supplementary component of its athletic apparel and footwear, even as fitness studios reopen, and has installed MIRROR technology in 18 of its over 500 US locations. The company expects to sell products directly through MIRROR in the near future, with anticipated revenue of $150 million from the channel in fiscal 2020.

We expect to see substantial M&A deals in the apparel and footwear market in 2022 and beyond. The main focus of M&A activity will be on apparel and footwear brands that most resonate with younger generations—these brands are popular among new consumer segments and offer quick returns compared to more mature brands.

What We Think

Many apparel and footwear specialty retailers across the US, the UK and China saw solid recovery in 2021—albeit with varying rates across regions and retailers, depending on their key product segments.

For 2022, against very strong comparatives, Coresight Research estimates that specialists’ sales in the US and China will see more stabilized growth. Unlike the US and China, the UK is witnessing a slower recovery—we forecast that the apparel and footwear market will fully recover to above pre-crisis levels in 2022, with 13.5% growth for the year, and we expect to see more stabilized growth from 2023 onward in the country.

Implications for Retailers

- We see e-commerce as a significant opportunity for apparel and footwear retailers to drive sales as we expect a large number of consumers to cement pandemic-driven online shopping habits in 2022 and beyond. We recommend that retailers enhance their digital capabilities, such as with new distribution centers and expanded ship from store capabilities.

- Apparel and footwear specialty retailers should continue to take proactive steps toward sustainability in order to win consumer trust and attract investors and employees in a dynamic retail landscape.

- We expect to see substantial M&A activity in the global apparel and footwear retail industry in 2022 and beyond. Acquisitions present opportunities for apparel and footwear giants to acquire new technologies and expand into new consumer segments to enhance their market shares. For struggling apparel and footwear retailers, M&A activity presents an opportunity to fix what is not working, for instance, long-term strategies could address the core retail business misdirection that led to the initial collapse. Although retailers lose control over their operations, there is upside potential for substantial synergy.

Implications for Technology Vendors

- Innovators have strong opportunities to partner with apparel and footwear specialty retailers to drive the push into e-commerce expansion. Innovators can also support apparel and footwear retailers in lowering inventory levels and improving efficiency, agility and resilience across their supply chains.

- Apparel and footwear retailers may look to acquire innovators with the goal of generating substantial synergy in their new retail models, as exemplified by Gap’s acquisitions of technology startups Context-Based 4 Casting and Drapr, and Lululemon’s acquisition of US livestreaming service provider MIRROR.

Source for all Euromonitor data: Euromonitor International Limited 2021 © All rights reserved