Nitheesh NH

What’s the Story?

Convenience is now more of a retail concept than a retail channel. No longer does a consumer need to walk or drive to their local convenience store to grab last-minute essentials; instead, convenience store selections (and more) come to them via quick-commerce operators. Not only has the quick-commerce sector expanded in terms of geographic coverage and product offerings, but the number of players has boomed. The explosion in industry participants is heavily concentrated on the vertically integrated segment, where players promise deliveries from their own fulfillment centers to urban consumers in as little as 10–15 minutes. We explore the spectrum of business models in this space and examine the differences in their economic operations. We also discuss key players in the market. Our coverage of quick commerce focuses on two segments:- Third-party delivery platforms—such as DoorDash, Instacart, Shipt and Uber Eats. These companies deliver products (largely grocery items) from third-party retail stores. In some cases, these delivery firms pick the orders while in others they only fulfill delivery. The promise has traditionally been for “same-day” delivery, although options now range from 30 minutes to several hours.

- Vertically integrated models—such as Gopuff, Fridge No More and 1520. These companies pick from a range of essential items in their own dark stores and courier them to shoppers, typically within 10–30 minutes.

Why It Matters

The online grocery boom in 2020 supported the emergence of a micro-industry of instant-need players, competing with more established operators that typically offer longer delivery windows for share of the expanding market grocery delivery market. Investors are betting big on instant needs, with a host of companies securing significant seed or sequential financing rounds since the beginning of 2021. Coresight Research estimates that retail sales (predominantly grocery/essentials) by major players in the overall quick-commerce market will total $20–25 billion in the US this year. This equates to a 10%–13% share of our estimate for US online CPG sales, which we expect to total around $191 billion in 2021. We factor in management commentary by public companies such as DoorDash and Uber, third-party data and our own estimates; which reflect the value of sales (gross merchandise volume) rather than revenues for delivery platforms, and exclude Amazon rapid delivery, such as Prime Now.From Quick Commerce to Instant Needs: Coresight Research Analysis

In the below sections, we establish the quick-commerce landscape and explore business model differences and economics. We also discuss key players in the market. 1. From Same-Day to 10-Minute Delivery: The Quick-Commerce Landscape In 2011 and 2012, respectively, Postmates (now Uber Eats) and Instacart established the quick-commerce, or hyperlocal, delivery model. Their model is built on working with third-party retailers (or restaurants) for the product itself. These quick-commerce firms are fulfillment intermediaries, traditionally promising “same-day” delivery, although the lower ranges of this (offered at a premium) have been pushed down to 30–45 minutes. Postmates collects orders from restaurants and retailers and brings them to the customer while Instacart picks and delivers from partner stores on behalf of the customer. Established in 2013, Gopuff took quick commerce and turned it into instant needs, carving out the abovementioned vertically integrated segment, offering delivery in an average of 30 minutes. Following its move into third-party grocery in 2018, DoorDash entered the vertically integrated instant-needs space in August 2020. It has established its own DashMart convenience stores offering delivery of essentials in 30 minutes or less. More recently, 15-minute commerce operators have intensified instant needs in terms of speed promises. Operators such as Fridge No More, JOKR and 1520 have entered the market, borrowing the vertically integrated model to promise delivery in as little as 10–15 minutes. In Figure 1, we provide a comparison of vertically integrated firms with delivery platforms. We have added in a comparison with meal delivery platforms and the traditional e-commerce model, too. We offer a full break-out of details by company at the end of this report.Figure 1. Overview of Online Fulfillment in the US

Quick Commerce in Retail

[wpdatatable id=1406]Source: Company reports/Coresight Research

We have seen a boom in funding in the vertically integrated instant-needs segment, which we calculate totals $5.9 billion to date. Gopuff has captured over half of that: Its valuation jumped to $15 billion after a July 2021 $1 billion fundraiser—equating to a quadrupled value in less than a year and taking its total funding to $3.4 billion. Istanbul-based Getir is valued at $7.5 billion following three funding rounds between January and June 2021.Figure 2. Recent Funding Raised by Instant-Needs Companies in the US, as of September 2021 [wpdatatable id=1407]

Source: Company reports/Coresight Research

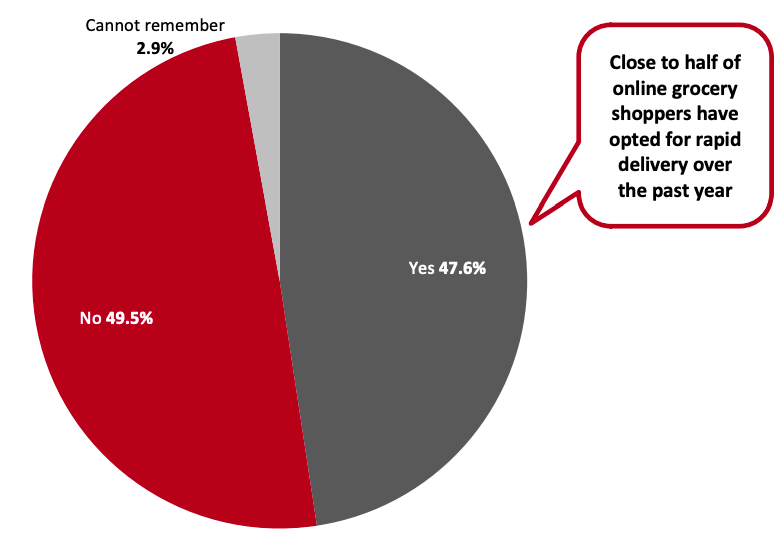

2. Online Grocery Shopping Surge Underpins Quick-Commerce Demand The pandemic acted as a significant catalyst in accelerating online grocery adoption, driving fundamental, lasting changes in consumer behavior. Coresight Research’s US consumer survey on October 18, 2021, found that almost half (48.8%) of respondents had bought groceries online in the past 12 months. We expect the online channel to see permanent gains as consumers retain their online shopping behaviors post pandemic. Delivery time is becoming increasingly important in online grocery shopping experiences. Our abovementioned survey found that around 48% of respondents that had purchased groceries online had selected rapid delivery, which includes same-day, one-hour and 15-minute/30-minute services.Figure 3. Online Grocery Shoppers: Proportion That Had Used Rapid Delivery Services for Groceries in the Past Year* [caption id="attachment_135371" align="aligncenter" width="580"]

*Rapid delivery includes same-day, one-hour and 15-minute/30-minute delivery services

*Rapid delivery includes same-day, one-hour and 15-minute/30-minute delivery servicesBase: 208 Internet users aged 18+ who had purchased groceries online in the past 12 months

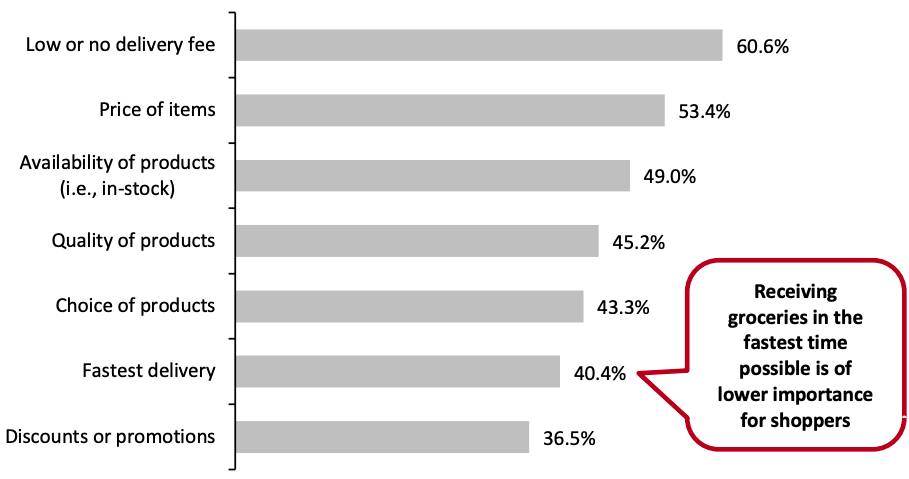

Source: Coresight Research[/caption] We asked online grocery shoppers which factors influence them most in choosing a rapid delivery service.

- The results suggest substantial price sensitivity in this space: Around 61% of respondents said low or no delivery fee is important, followed by 53% reporting that the price of items is key. Potential future increases in delivery fees in the near term therefore look problematic—particularly given the competitive environment—suggesting that operators will need to subsidize free or low-cost delivery, at least until the market has consolidated and competition has diminished.

- Fastest delivery is ranked lower, implying that shoppers are comfortable with slightly longer delivery times, which typically bring lower costs to the service. This relative disinterest suggests that five-minute increments in delivery times are unlikely to be a principal driver of choice among the general population (although we acknowledge that expectations of speed may be higher in large cities such as New York).

Figure 4. Online Grocery Shoppers: Factors That Are, or Would Be, Most Important to Them When Choosing a Rapid Delivery Service (% of Respondents) [caption id="attachment_135372" align="aligncenter" width="700"]

Base: 208 Internet users aged 18+ who had purchased groceries online in the past 12 months

Base: 208 Internet users aged 18+ who had purchased groceries online in the past 12 monthsSource: Coresight Research[/caption] 3. Business Model Differences and Economics There are significant differences between quick-commerce players—in scale, business model and delivery offering—and with these distinctions come differing advantages and economies. In this section, we compare vertically integrated companies with delivery platforms and we discuss economics below. Vertically Integrated These operators build out their own first-party MFCs, akin to dark stores, and engage employees to pick orders as well as couriers to deliver them. Advantages

- Vertically integrated MFCs are optimized for speedy picking and are strategically located as close to customers as possible, enabling instant-needs operators to promise such short delivery times.

- By owning inventory, vertically integrated players also have greater visibility on product quality, inventory supply and pricing.

- Instant-needs companies typically carry a fast-rotating assortment of 1,000–2,000 goods (although Gopuff offers up to 4,000) that are localized to the neighborhoods they serve. For example, Buyk takes a “hyperlocal” approach to assortment to ensure that its MFCs stock meets the specific needs and desires of shoppers in each particular area it serves.

- Some operators are planning to flex their SKU range. Instant-needs company 1520, which typically carries 1,500 items, said that it is planning to target 3,000 SKUs in the near future, targeting a wider range of consumer needs.

- Instant needs depends on a degree of population density (and moreso when the delivery time is as little as 15 minutes) and as more players enter the market, the risk of increasing rental costs for MFCs in urban locations could drive up upfront investment.

- Setting up MFCs and procuring inventory requires capital investment before entering a new city or market.

- The underlying model of investing in (dark) stores and relying on operational leverage to drive margins has some similarities to traditional brick-and-mortar retail, and comes with similar weaknesses (and strengths), such as volume sensitivity.

- Delivery platforms operate an asset-light model, which does not require fulfillment centers to be deployed or supplier relationships to be established before entering a new city.

- These platforms will usually offer more choice than vertically integrated players, although the overall offer will be driven by the operating hours and the selection of the third-party retailers’ stores.

- The store-pick model employed by delivery operators is more susceptible to out-of-stocks as the platforms do not have full, real-time visibility into the retailer’s in-store inventory. Additionally, delivery platforms surrender pricing power to third-party merchants (retailers) and some retailers raise prices on delivery apps to help offset the merchant fees that they pay to the delivery firm. Some municipalities cap merchant fees, which can push up consumer fees.

- A reliance on per-transaction fees suggests a relatively straight line for costs as sales grow, meaning delivery platforms have a lesser degree of operational leverage than the dark-store model.

Figure 5. A Comparison of Per Order Economics: Instant-Needs Model vs. Delivery Platform Model [wpdatatable id=1408]

Source: Company reports/Coresight Research

All of the vertically integrated instant-needs players discussed are privately owned. Nazim Salur, CEO and Founder of Getir (not yet in the US market), told the New York Times in 2021 that a neighborhood can be profitable after a year or two. Similarly, Gopuff management has stated it has achieved profitability in every market that it has operated in for more than 18 months. Furthermore, German online grocery and restaurant delivery company Delivery Hero has disclosed a profit contribution of €1.3 ($1.5) per order in its DMart dark-store business. Among the delivery platforms, Uber’s “Delivery” segment Uber Eats remains loss-making, with an adjusted EBITDA margin (as a percentage of gross bookings, which is akin to gross merchandise volume) of (1.6)% in the first quarter of 2021 and (1.2)% in the second quarter. Uber’s Delivery gross bookings increased by 85% year over year to $12.9 billion in the second quarter; this is worldwide and largely restaurant bookings—in the second quarter, management commented that “grocery and new verticals” (which includes convenience and alcohol) accounted for about 5%–6% of total gross bookings. At DoorDash, adjusted EBITDA as a percentage of gross order volume stood at 0.4% in the first quarter of 2021 and 1.1% in the second quarter. DoorDash reported $10.5 billion in gross order volume in the second quarter, up 70% year over year, largely comprised of restaurant orders. Management stated that "nonrestaurant orders now are totaling over 7% of our total orders" in the first quarter (latest indication). On a statutory basis, DoorDash’s EBIT margin was (9.2)% in the first quarter of 2021 and (8.0)% in the second quarter. 4. Key Players In Figure 6, we expand on details provided in this report to provide an overview of the operations and offerings of significant players in US quick-commerce retail. Gopuff has a 70+% share of the US vertically integrated instant-needs market, according to data firm YipitData. Buyk is a new entrant and Getir is reportedly soon to launch in the US market. The retail propositions from DoorDash and Uber Eats emerged from restaurant delivery operations and their retail operations contribute only a single-digit share of their order volumes, as discussed above. In September 2021, Kroger partnered with Instacart to launch Kroger Delivery Now, with orders fulfilled from Kroger stores in around 30 minutes. Services offered directly by retailers include 7NOW from 7-Eleven.Figure 6. US Quick Commerce: Key Competitors [wpdatatable id=1409]

Source: Company reports/Coresight Research