Executive Summary

In the US, younger consumers appear to be driving shifts in the beauty retail landscape.

- Lower-price retailers such as Walmart and Target have grown their share of beauty shoppers, according to surveys by Prosper Insights & Analytics, and younger shoppers are much more likely than older generations to shop for beauty products at Target.

- Specialist chains Sephora and Ulta have grown sales fast, too. They are increasing their store footprints and have upped their share of beauty shoppers—and young shoppers significantly overindex at these chains.

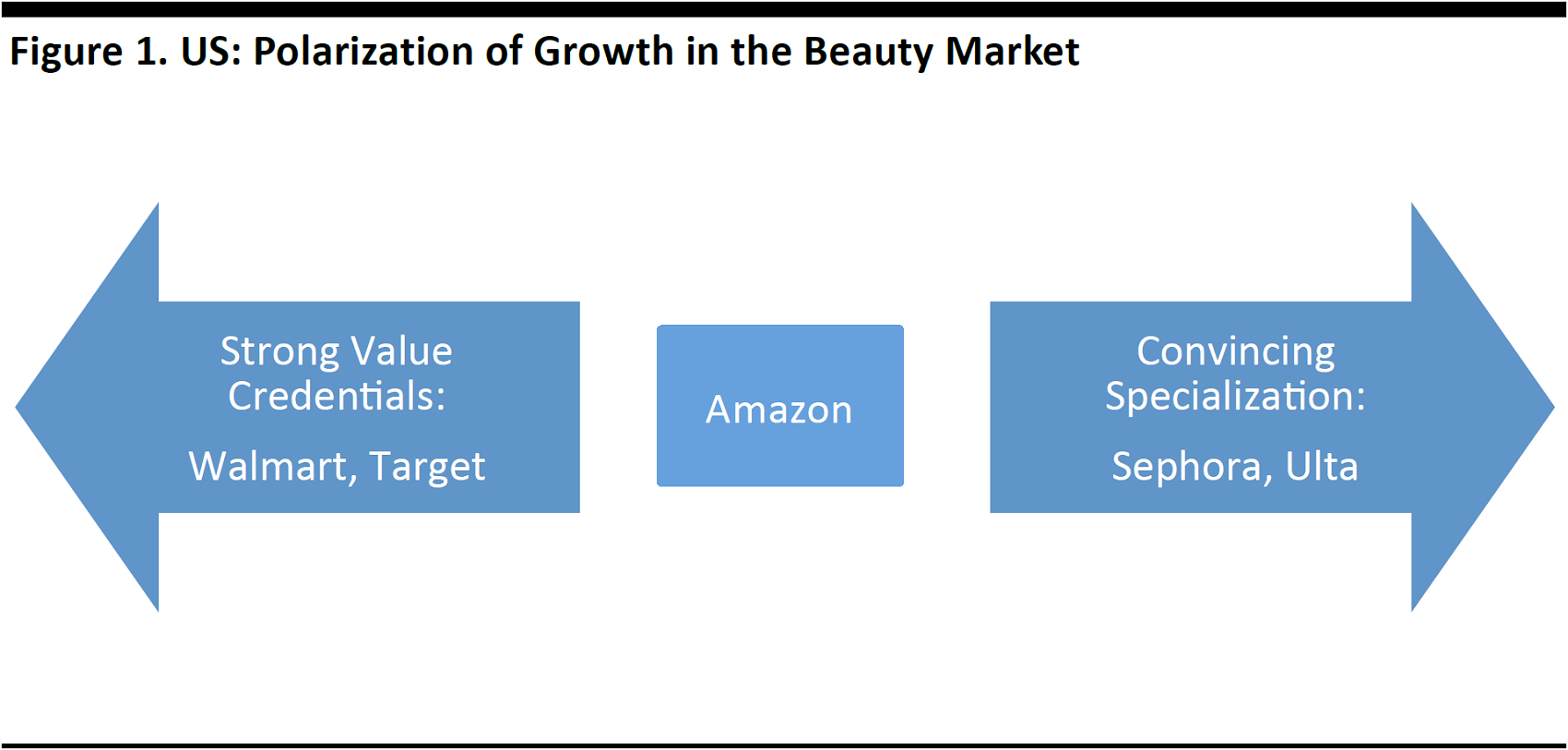

These shifts suggest a polarization of growth in the US beauty retail market.

According to Prosper surveys, lower prices are a strong motivator for shopping for health and beauty products at Walmart, Target and Amazon, and price is the most important factor overall when consumers are deciding where to buy such products. By contrast, the top three reasons consumers shop for health and beauty items at Ulta are selection, quality and promotions and the top reasons they shop at Sephora are quality, selection and brands available, according to Prosper surveys.

The strong price appeal of Amazon suggests that it could, in time, disrupt the growth in shopper numbers that lower-price, store-based retailers have enjoyed. By shopper numbers, Amazon is the fifth-most-popular retailer for skincare and cosmetics purchases, according to Prosper, and it is the most popular online retailer for beauty, per A.T. Kearney.

Survey data suggest that some drugstores and department stores overindex among older shoppers. To attract younger shoppers, these retailers could consider strengthening their entry-level beauty ranges, introducing or bolstering beauty loyalty programs and, where practical, offering in-store beauty services.

Source: iStockphoto

Introduction: Changing Shopping Habits

Consumers are changing where they shop for beauty products—and not just because e-commerce has grown and provided them with more choices. In this report, we outline the polarization of growth in store-based beauty retailing, which is similar to the trend we have seen in other segments, such as fashion. Consumer surveys indicate that value-positioned retailers such as Target have picked up shoppers, while specialized retailers such as Sephora have grown sales strongly.

A key takeaway for those retailers selling beauty products is a concept that is applicable across categories: either specialize convincingly or focus on low prices—because the middle ground is increasingly served by Amazon.

Source: FGRT

We perceive younger consumers as driving these shifts toward value-positioned and specialist retailers, for two main reasons:

- Millennials tend to be frugal shoppers, shopping around, looking for deals and cutting coupons to save money. As a result, they typically spend less per person on beauty and personal care products than do older generations. At the same time, many younger consumers appreciate quality shopping experiences, and Sephora engages very successfully with younger consumers. We covered these issues in a previously published report, Millennials Series: Millennials and Beauty.

- Drugstores such as CVS and Walgreens remain prominent retailers for beauty products, but older consumers are much more likely than younger ones to buy beauty items at these stores.

In the following sections of this report, we analyze the channel shifts we have seen in terms of beauty purchases, examine where consumers shop for beauty products and why, explore the growth of Sephora and Ulta, and discuss the rise of e-commerce and Amazon in beauty.

Charting Channel Shifts: Specialist Retailers Overtake Department Stores as America’s Favorite Beauty Stores

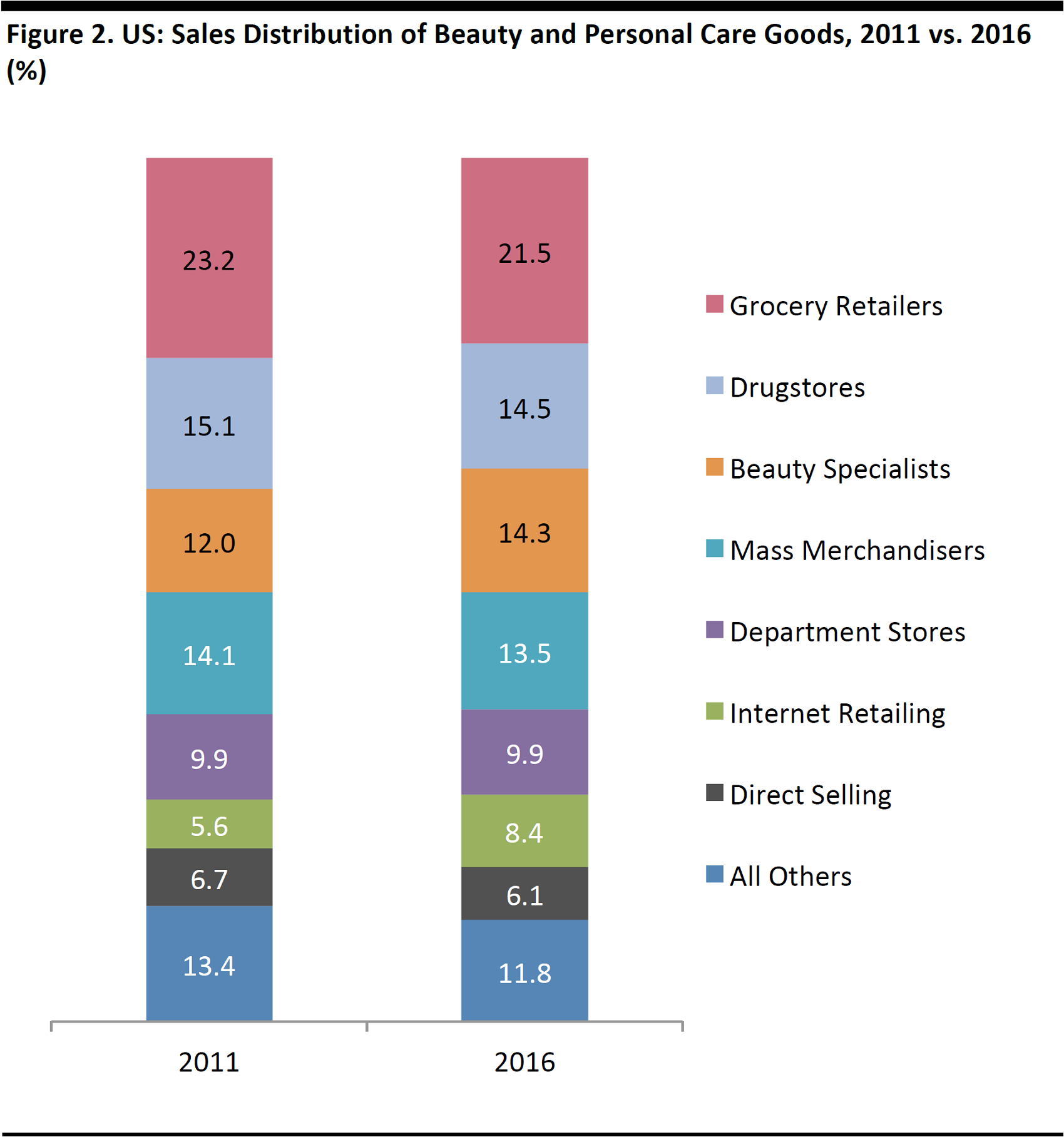

We begin by charting the broad view of sector share in the US beauty and personal care market. This illustrates the growth of e-commerce, but also the rise of specialist retailers, such as Sephora and Ulta, between 2011 and 2016.

- Beauty specialist stores grew their total market share from 12.0% to 14.3% between 2011 and 2016. The specialist sector looks to be on the cusp of overtaking drugstores to become the second-biggest channel, behind supermarkets.

- Internet retailing’s market share grew from5.6% to 8.4% over the same period. This figure includes beauty and personal care e-commerce sales made by all types of retailers. The data for the various other channels charted below represent offline sales only.

All Internet retail sales are included in the Internet retailing figures.

Source: Euromonitor International

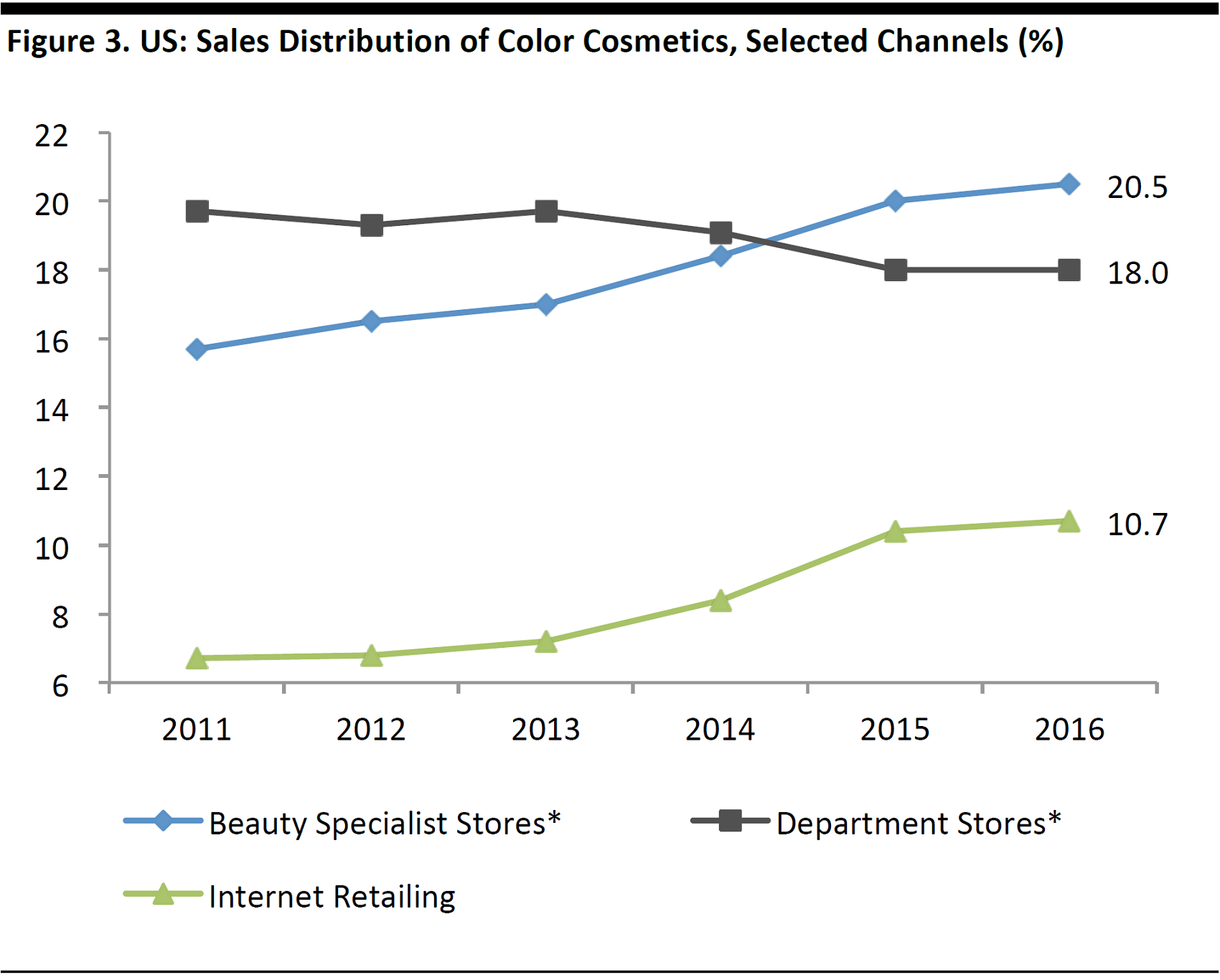

Drilling down to the core beauty category of color cosmetics, beauty specialist retailers grew share consistently in the five years ended 2016. The specialist sector overtook department stores in terms of sales values in 2015 and now accounts for more than one-fifth of color cosmetics sales.

All Internet retail sales are included in Internet retailing.

*Offline sales only

Source: Euromonitor International

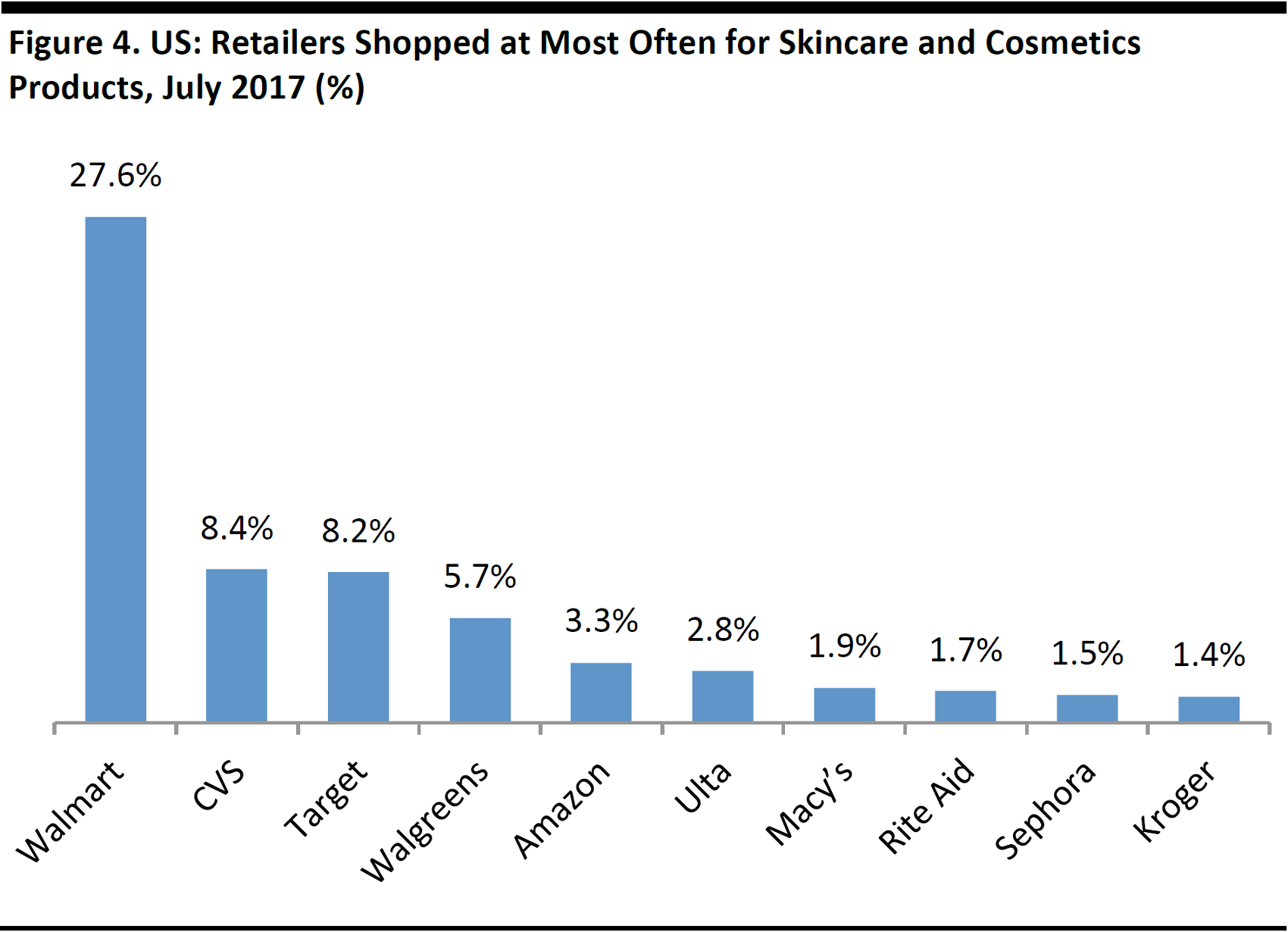

Where Consumers Shop: Walmart, Target and Amazon Are Highly Popular

In this section, we turn to specific retailers, and we chart data from Prosper Insights & Analytics that show where consumers say they shop most often for skincare and cosmetics products. It should be noted that respondents could choose only one option and so these data do not take into account secondary destinations used for additional or top-up shopping.

- Walmart is by far the top retailer among consumers asked by Prosper where they shop most often for skincare and cosmetics.

Source: Walmart.com

- Drugstores are popular skincare and cosmetics shopping destinations, too, although they are more popular among older consumers.

- Neither Sephora nor Ulta feature in the top five retailers named by those asked where they shop most often for skincare and cosmetics, perhaps suggesting that they are a secondary destination for some consumers. As we show later, these average figures conceal significantly higher rates of shopping at Sephora and Ulta among younger consumers.

Base: 7,266 US Internet users ages 18+. Respondents could select only one option.

Source: Prosper Insights & Analytics

Source: iStockphoto

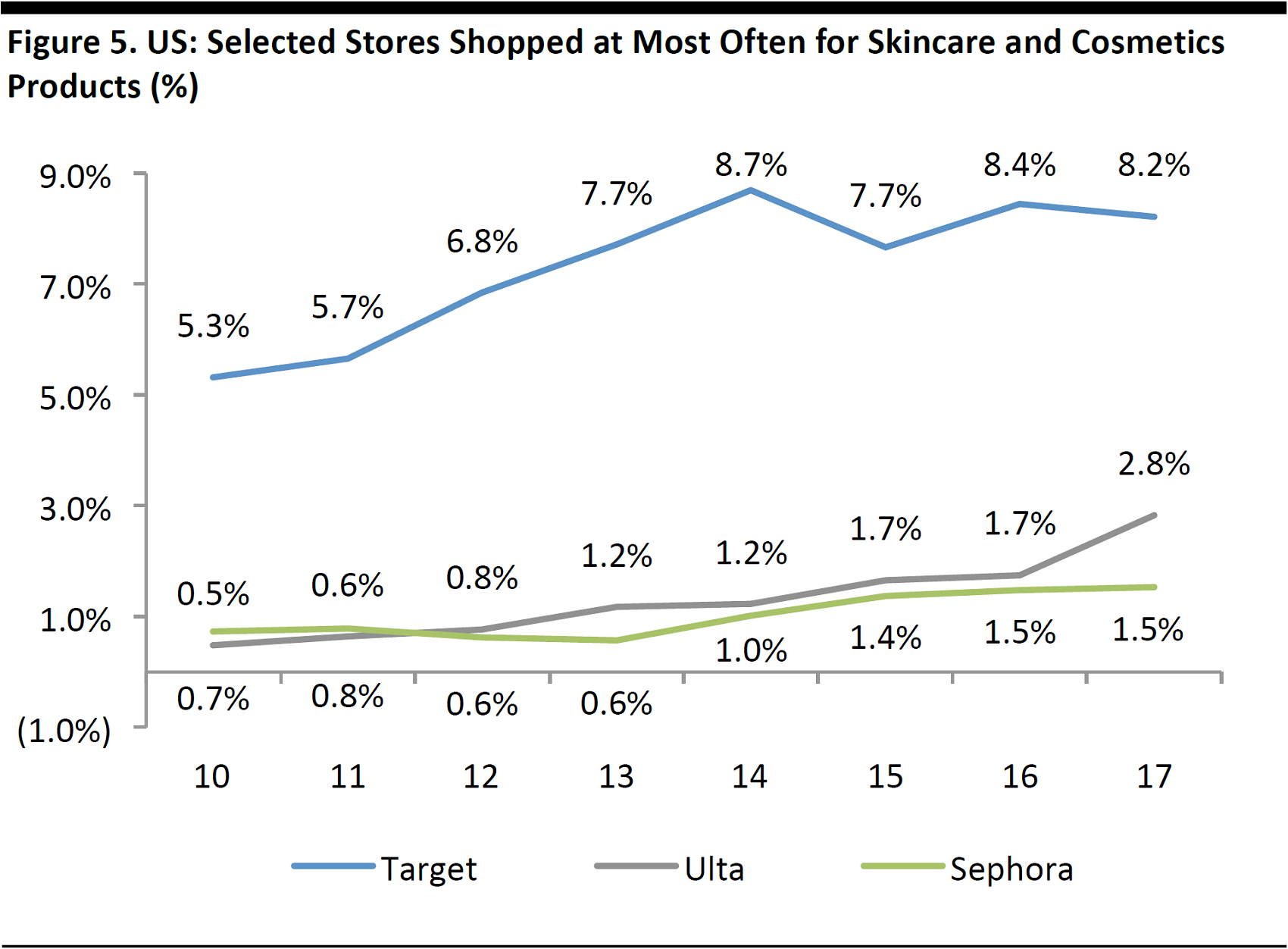

Trend data for the 2010–2017 period bear out the concept of a polarization in US beauty retailing, with lower-price players and specialists seeing general upward trends: Target, Sephora and Ulta have each seen their shopper numbers grow significantly, according to Prosper. We exclude Walmart from the graph below because its scale relative to the other retailers shown proves overbearing, but, according to survey data, Walmart grew from being the most-often-shopped store for skincare and cosmetics for 24.3% of consumers in 2010 to 27.6% in 2017.

Base: Between 5,653 and 9,009 US Internet users ages 18+ surveyed in July of each year. Respondents could select only one option.

Source: Prosper Insights & Analytics

The nature of general merchandise retailers such as Walmart and Target means that we do not have robust category-level sales data for them. In the absence of such indicators, we think consumer survey data such as those shown above are the best guide to performance at general merchandisers. However, according to TABS Analytics data published in March 2017, Walmart enjoyed a 19.4% share of the personal care market and Target a 12.8% share.

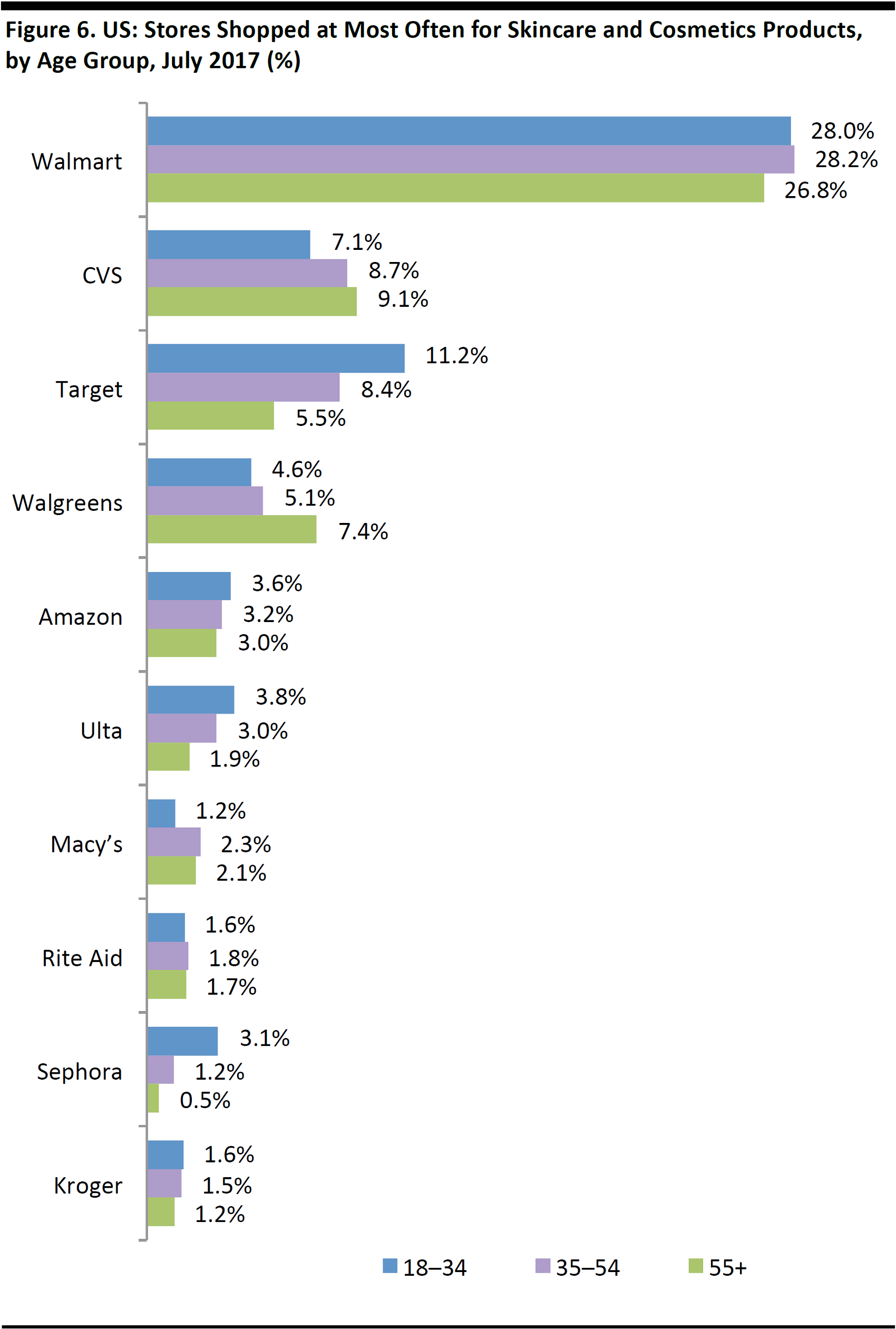

Young Consumers Overindex at Value and Specialist Retailers

Younger consumers look to be driving the switch to value retailers and specialists. Prosper’s data show that 18–34-year-olds are much more likely than older consumers to shop most often for skincare and cosmetics at Target, Sephora and Ulta. In addition:

- Younger consumers are turning to Macy’s in smaller numbers than older age groups are.

- Yet it is apparent that younger consumers are not switching away from general merchandise retailers overall: Walmart and Target are very popular among 18–34-year-old beauty shoppers, confirming that many millennials opt for low-price retailers in the beauty category.

- Older consumers are more likely than younger consumers to shop most often for skincare and cosmetics at drugstore chains such as CVS and Walgreens.

Base: 7,266 US Internet users ages 18+. Respondents could select only one option.

Source: Prosper Insights & Analytics

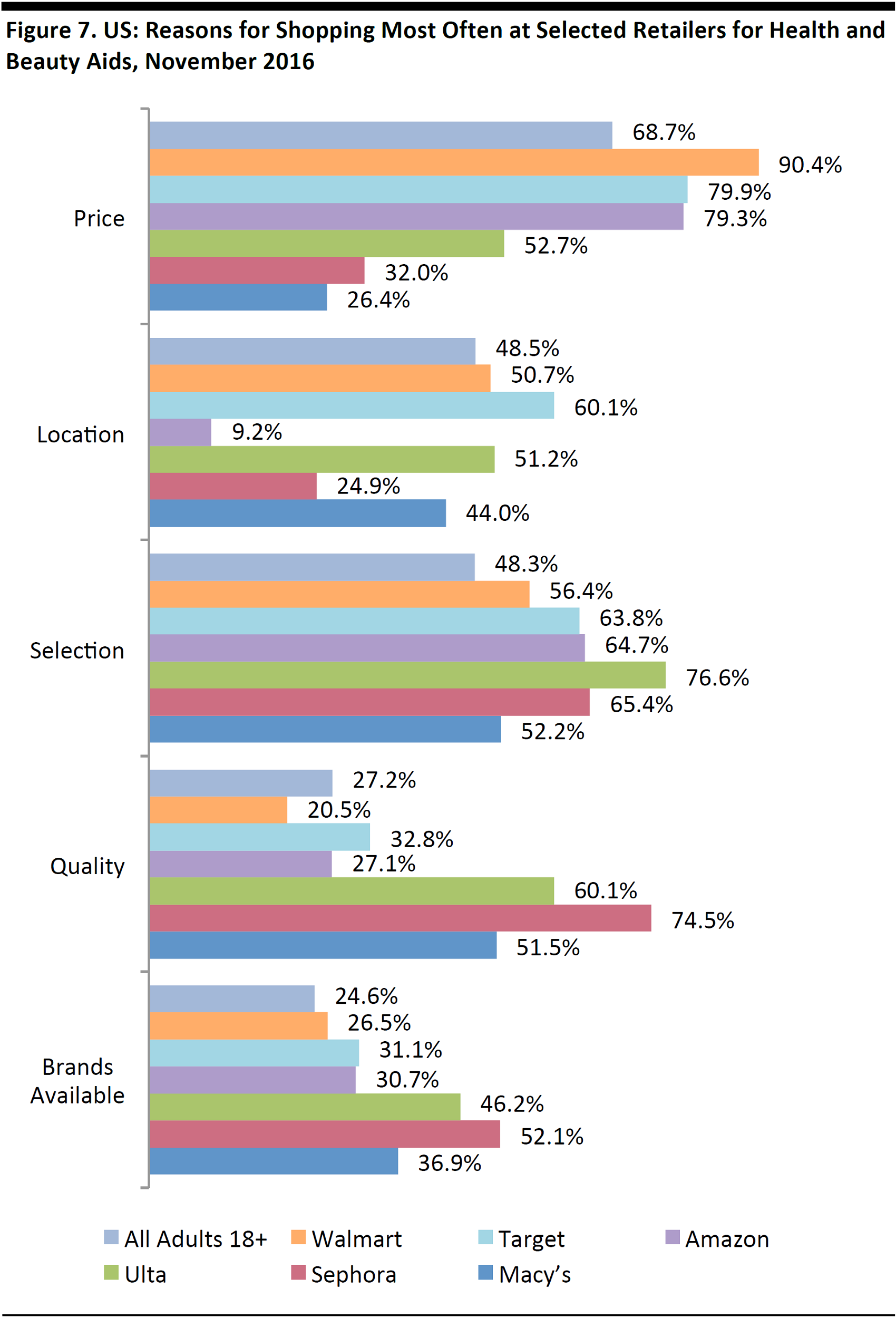

So, why do consumers choose these retailers? Below, we chart the top five reasons shoppers cite when asked why they shop most often for health and beauty products at various selected retailers (note that this question covers a broader category than the beauty survey cited above):

- Price is a strong motivator for shopping at Walmart, Target and Amazon, and it is the most important factor overall.

- The strong appeal of price at Amazon suggests that it could, in time, disrupt the growth in shopper numbers that lower-price, store-based retailers have enjoyed.

- Selection is a major driver for shoppers at Target, Amazon, Ulta and Sephora.

- Only Ulta and Sephora stand out in terms of the “brands available” option.

- We chart fuller data later in this report for Ulta, Sephora, Amazon and Walmart.

Base: 7,206 US Internet users ages 18+

Source: Prosper Insights & Analytics

In Focus: Ulta and Sephora Dominate Specialist Retailing

The US beauty specialist sector is highly concentrated, with Ulta and Sephora holding dominant positions. L Brands’ Bath & Body Works is in third place, but its offering focuses more on toiletries and personal care than on beauty categories.

We estimate that Sephora generated between $4.4 billion and $4.9 billion in US revenues in 2016. These estimates are based on company filings and 2016 statements by LVMH management (LVMH owns Sephora) that Sephora contributed “around 40%” and “about 45%” of the company’s total US revenues. At the upper end of these estimates, Sephora would be broadly in line with Ulta, which generated $4.85 billion in revenues in the year ended January 2017.

*Fiscal years ended January 2017

Source: S&P Capital IQ/company reports/FGRT

Source: iStockphoto

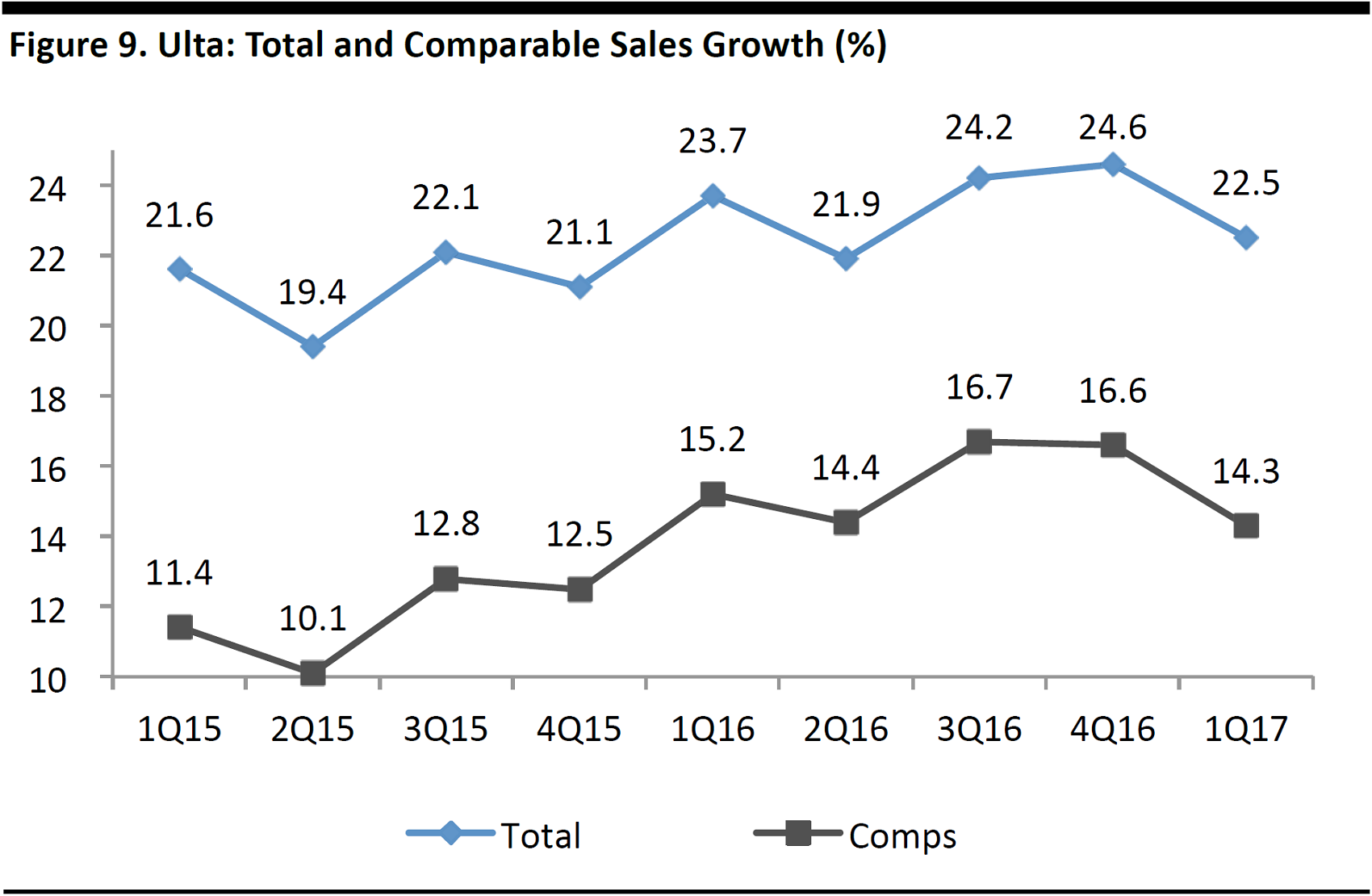

Ulta and Sephora Growing Strongly

As we chart below, Ulta has posted very impressive revenue growth in recent years, with total sales growth supported by double-digit comps and new store openings. The general trend since early 2015 has been for revenue growth to strengthen.

Source: Company reports

Banner-level disclosure is limited for LVMH-owned Sephora, but LVMH has shared the following details:

- In its first-half 2017 earnings call, LVMH management noted double-digit sales growth for Sephora worldwide.

- In the first quarter of 2017, LVMH noted “particular strength” for Sephora in North America.

- LVMH pointed to Sephora’s “particularly remarkable performance” in the US in 2016.

- In its first-half 2016 earnings call, LVMH more specifically noted double-digit comps for Sephora in the US market.

Sephora and Ulta are both capitalizing on growing demand to expand their physical presence:

- Sephora has 357 stand-alone US stores, according to the company’s website (accessed on July 28). In addition, Sephora has 574 shops inside JCPenney stores, again per the company’s website. In April 2017, JCPenney announced plans to open a further 70 Sephora shops in its department stores and to expand 32 existing shops-in-shops.

- Sephora opened a flagship store in Boston in the first half of 2017 and it will open a store at the World Trade Center in New York in the second half of the year.

- Ulta had 990 stores at the end of the first quarter of 2017 (latest); the figure was up 12% year over year. Across 2017, Ulta plans to open around 100 new stores and remodel 11 others.

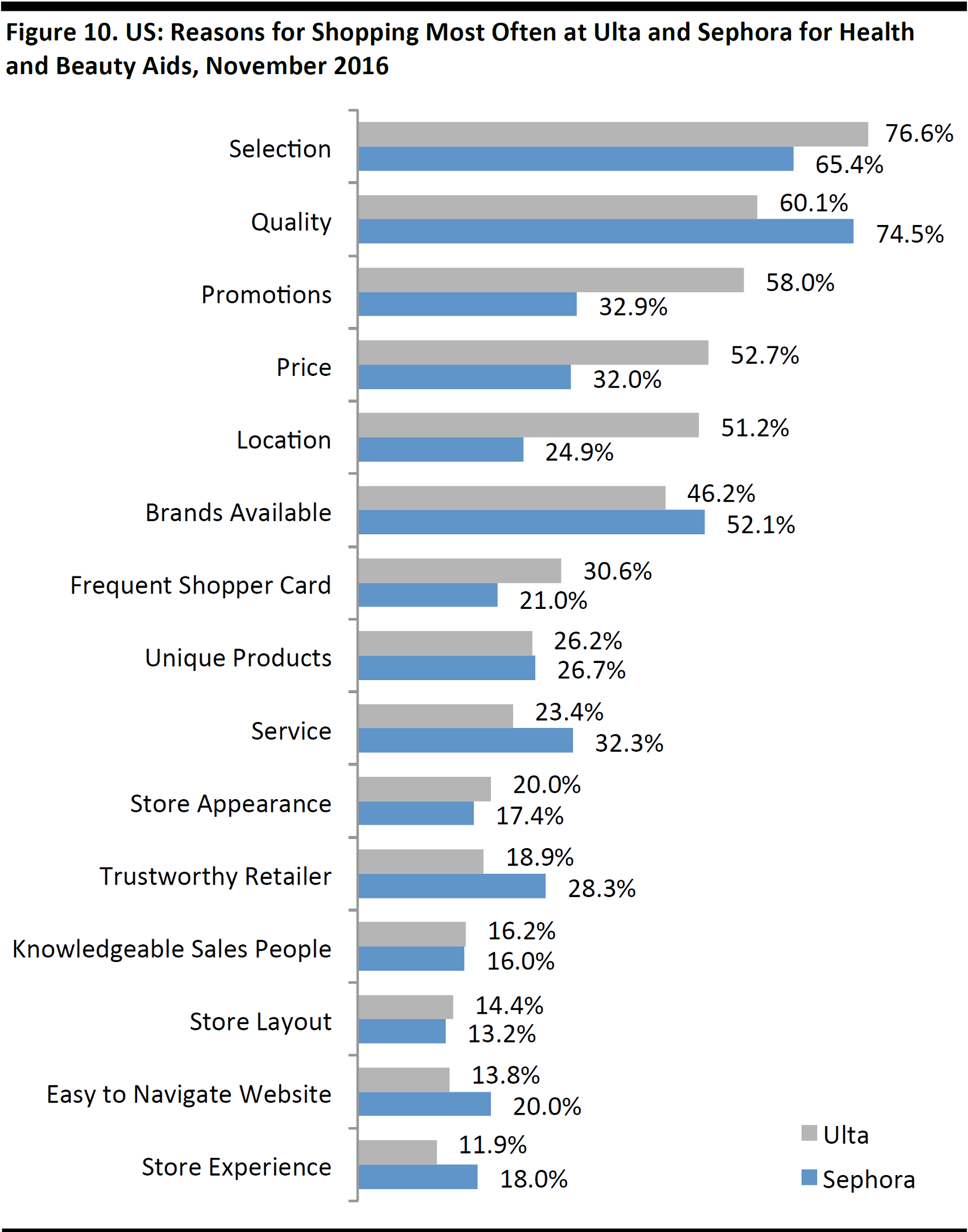

Why Consumers Shop at Ulta and Sephora

Earlier, we discussed the top reasons consumers cite for shopping at a range of beauty retailers. In this section, we look in more detail at the reasons they shop for health and beauty products at Sephora and Ulta, using data from the Prosper monthly consumer survey conducted in November 2016:

- Price ranks relatively low as a consideration for shoppers at each chain, in contrast to it being the top consideration for health and beauty shoppers overall.

- Ulta narrowly beats Sephora on selection, promotions and price. Ulta’s strength in promotions may reflect its very popular loyalty program and its bonus points offers, while its strength in price is likely due in part to its entry-level product offerings.

- Sephora enjoys a lead in terms of quality and brands available—perhaps reflecting demand for Sephora’s own brand.

Sample size: Sephora customers: N=101; Ulta customers: N=148

Source: Prosper Insights & Analytics

In Focus: E-Commerce and Amazon

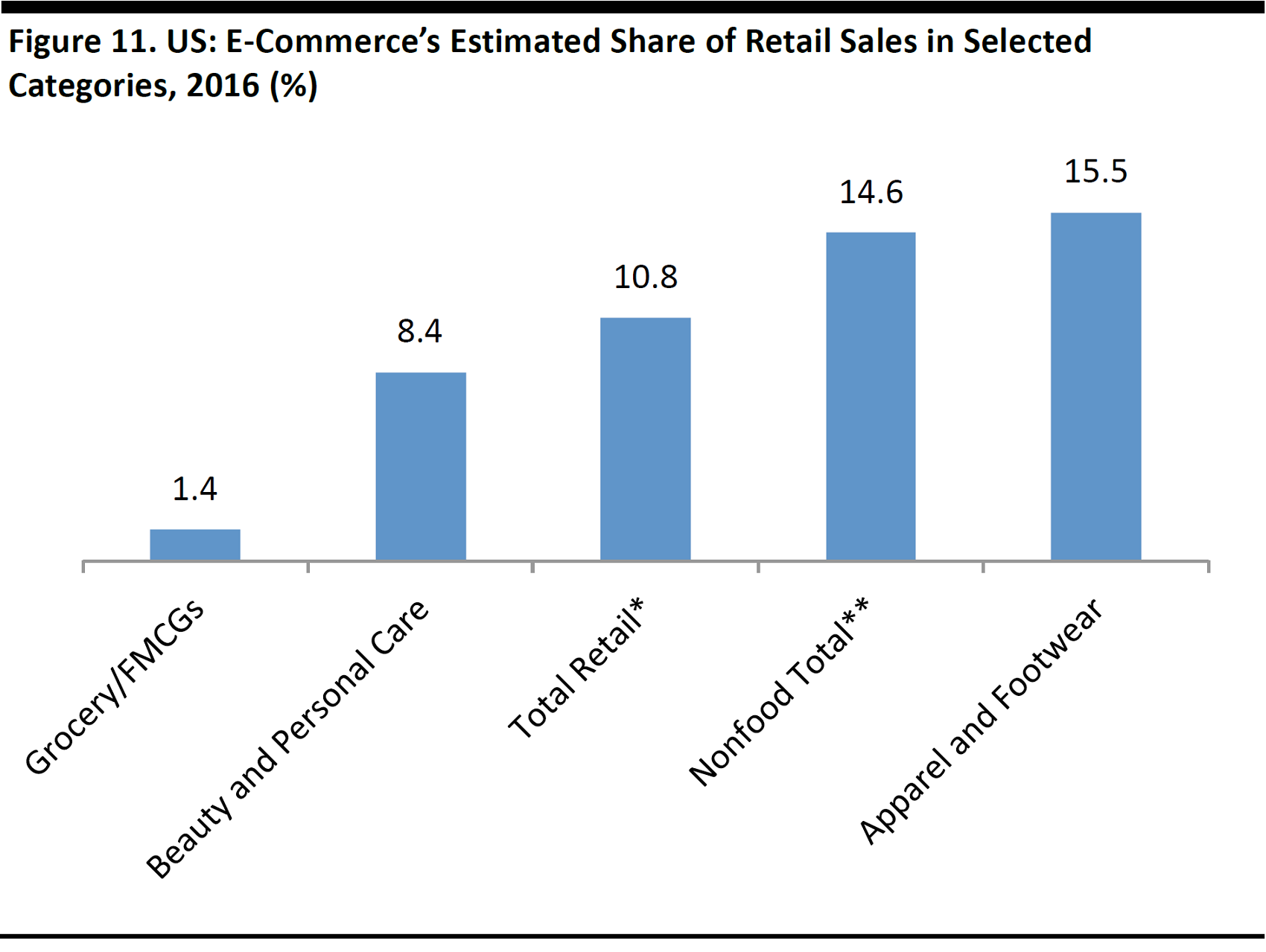

E-commerce’s share of beauty and personal care sales will rise to 8.9% in 2017 from 8.4% in 2016, according to Euromonitor International estimates.E-commerce is a high-growth channel for beauty sales, but it captures a lower share of sales in beauty than it does in apparel, total nonfood retailing and even total retailing. We chart e-commerce penetration data for a number of categories below.

We see beauty under-indexing online due to a number of reasons:

- The low purchase prices for everyday products may not justify shipping costs.

- Consumers may want to test and try beauty products before buying them.

- Some beauty and personal care purchases are made as part of grocery shopping trips—and e-commerce has captured only a tiny share of the grocery market.

Due to this relative underindexing, we see greater long-term growth opportunities in beauty e-commerce than in some more mature e-commerce categories.

*Excluding foodservice, motor vehicles and parts, and automotive fuel

**Based on stripping out food and beverage sales only; other grocery categories were included.

Source: Kantar Worldpanel/US Census Bureau/US Bureau of Economic Analysis/Euromonitor International/FGRT

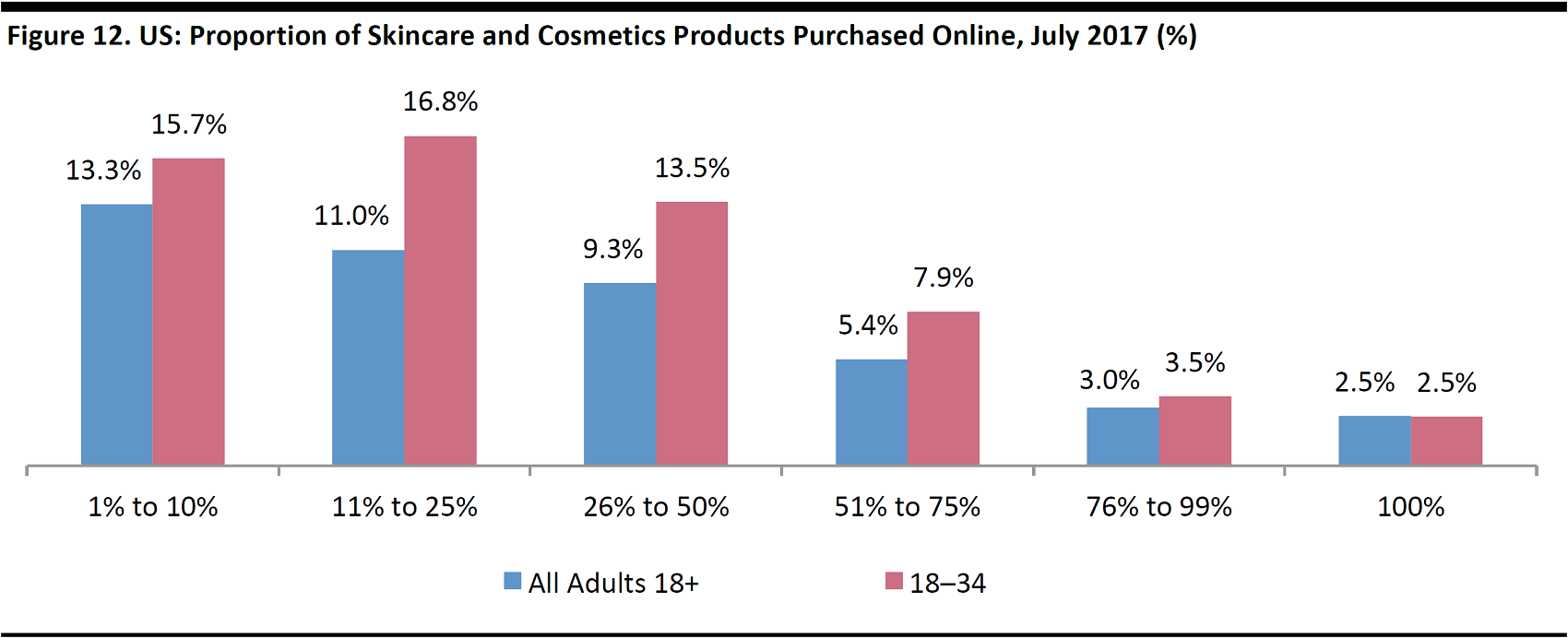

The minor share of beauty category sales captured by e-commerce does not reflect low online shopping participation rates, according to Prosper’s July 2017 survey, as:

- Some 45% of US consumers surveyed said that they buy the core beauty categories of skincare and cosmetics online.

- Among 18–34-year-olds, that percentage rises to 60%.

- Some 48% of 35–54-year-olds buy skincare or cosmetics products online. The share falls to 29% among those aged 55 or over.

Rather, the overall low share captured by e-commerce reflects the fact that the online channel tends to account for a minority of total spending among online shoppers. The chart below shows how much respondents say they spend online out of their total skincare and cosmetics spending. We pick out the 18–34-year-old age group, as it is the most important segment for online beauty retailing. Almost half of 18–34-year-olds purchase between 1% and 50% of their skincare and cosmetics online. Only 14% of that age group makes more than half of their purchases online.

Source: iStockphoto

Base: 7,266 US Internet users ages 18+

Source: Prosper Insights & Analytics

Focusing on Amazon, the Most Popular Online Destination for Beauty and Personal Care Products

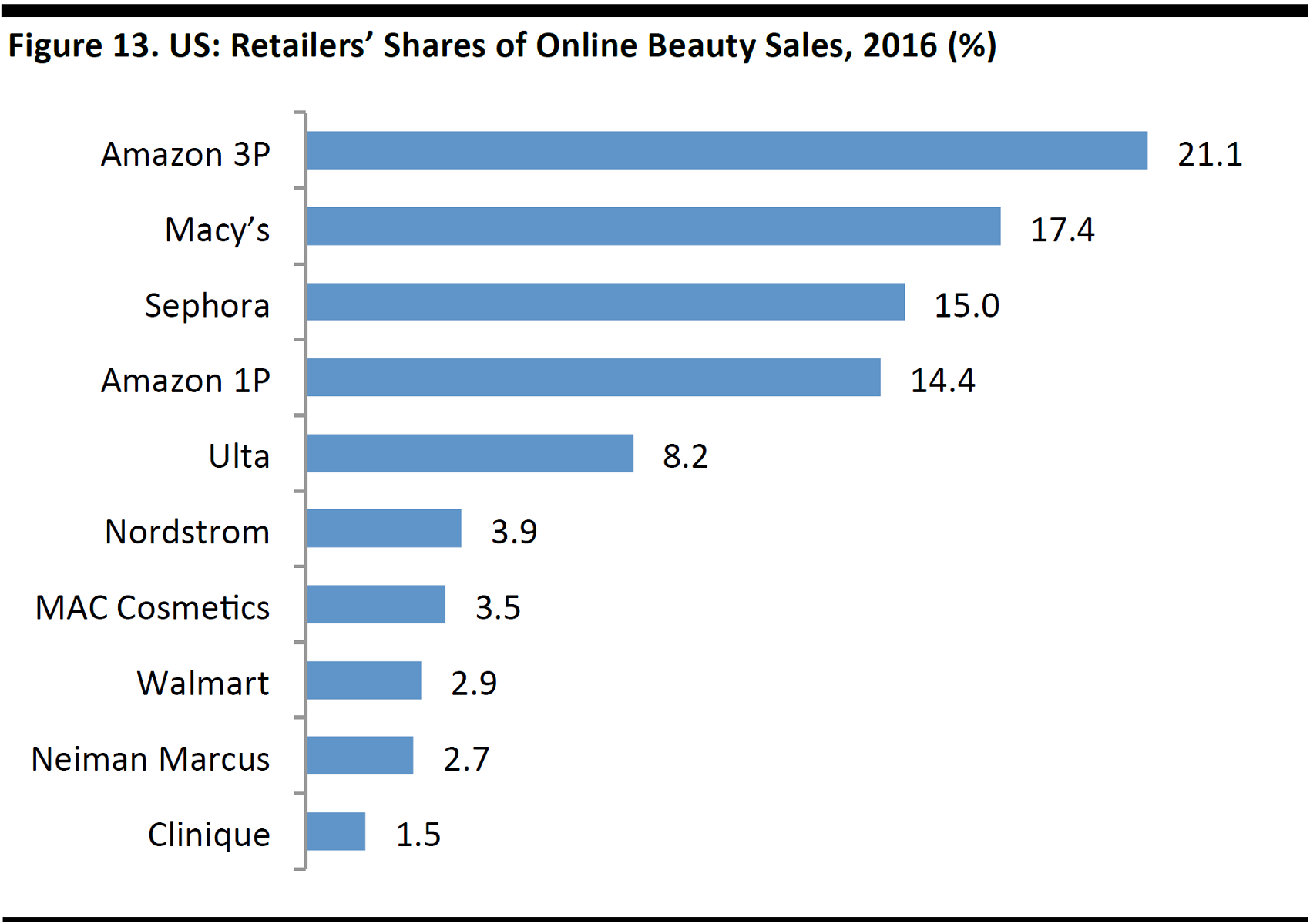

So, how big is Amazon in the online beauty space? It is a question many will want an answer to, but there are few concrete indicators of US retailers’ online market shares. In February 2017, research firm 1010data published its estimates of online beauty market shares, and the research places Amazon’s marketplace of third-party sellers as by far the biggest online seller of beauty products in 2016. The combined online market share for Amazon’s third-party and first-party sales was 35.5% in 2016, according to 1010data. Macy’s and Sephora were in second and third places, respectively.

Market share based on the fragrance, face makeup, eye makeup, lip makeup and nailcare categories.3P=third-party sellers; 1P=first-party sales

Source: 1010data

While these figures may provide some guidance as to retailers’ online market shares, we think that there are reasons for treating them with some caution:

- The stated share for Ulta looks somewhat low to us. 1010data puts the 2016 online beauty market size at $1.2 billion, and Ulta reported total e-commerce sales (including any nonbeauty category sales) of $345 million in 2016. Even if only 50% of Ulta’s online sales were in the categories included in 1010data’s definition of the market, the retailer would have enjoyed an approximate 14% share of the $1.2 billion online market last year. In fact, just over half of Ulta’s total revenues came from cosmetics in the year ended January 2017; further shares came from adjacent beauty categories such as fragrance and skincare.

- Euromonitor pegged US online sales of color cosmetics alone at $1.7 billion in 2016, versus 1010data’s estimation of $1.2 billion for the total online beauty market size.

Indications of category growth rates at Amazon come from analytics firm One Click Retail. For the first quarter of 2017, the firm reported that:

- Amazon grew its US health and personal care sales by 30% year over year.

- The fastest-growing beauty category for Amazon US was skincare, which was up 90% year over year.

- In the UK, shaving and hair removal products were the highest-growth beauty categories, with sales up 90% year over year.

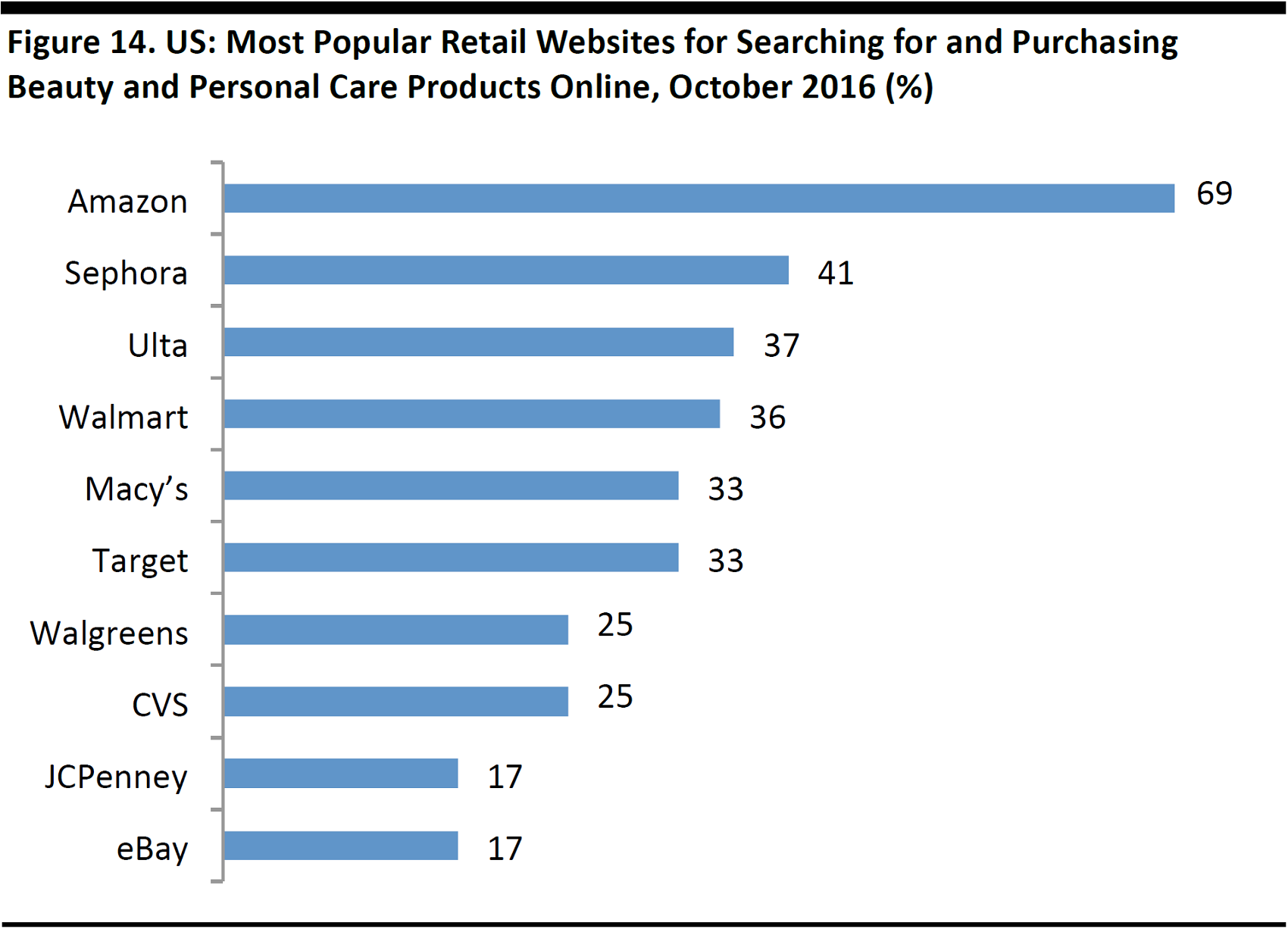

Given the paucity of concrete online market share data, consumer surveys are among the more reliable indicators of various retailers’ popularity. By number of shoppers, Amazon is by far the most popular retailer online for beauty and personal care products in the US, per a 2016 survey by A.T. Kearney, charted below. Sephora and Ulta hold strong positions, too. As noted earlier, Amazon is the fifth-most-popular retailer overall (online or offline) for skincare and cosmetics, per Prosper’s July 2017 survey.

Base: 800 online shoppers

Source: A.T. Kearney

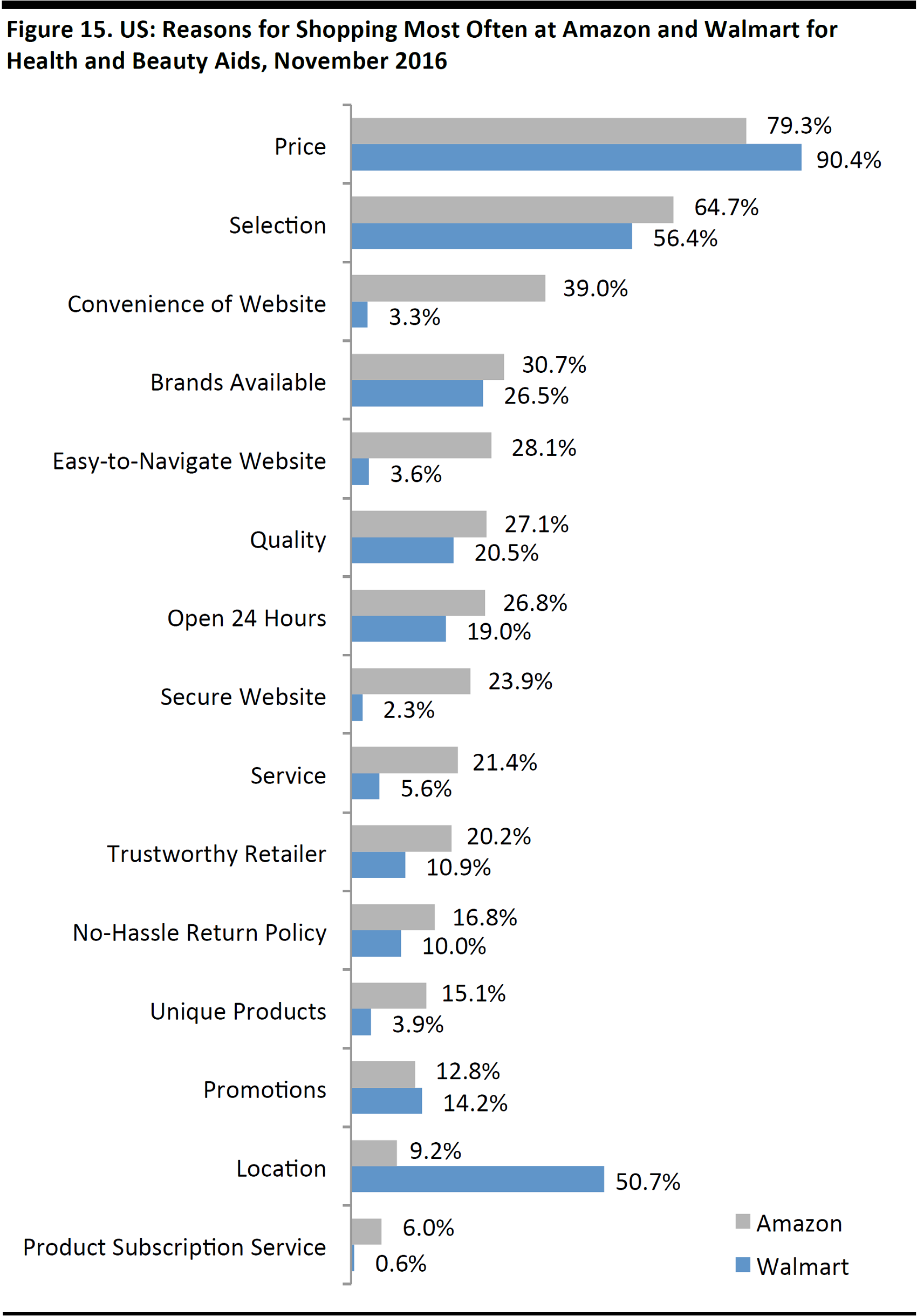

Finally, Prosper survey data can show us the reasons consumers opt to buy health and beauty products from Amazon. For comparison, we include data on Walmart, too. Price, selection and the convenience of its website are the top reasons shoppers choose Amazon. The next-most-popular options cited—brands available and easy-to-navigate website—appear to be similar options to the selection and convenience of website choices.

Source: Amazon.com

Sample size: Amazoncustomers: N=246; Walmartcustomers: N=1,975

Source: Prosper Insights & Analytics/FGRT

Key Takeaways

We have seen an apparent polarization of growth in the beauty market, with survey data and company reports suggesting that low-price retailers and convincing beauty specialists have won share. We see millennials’ thrifty behavior and desire for quality experiences as driving this trend.

Survey data suggest that some drugstores and department stores overindex among older shoppers. If these types of retailers want to draw in millennials, what can they do? We suggest that they consider strengthening their entry-level ranges, bolstering their beauty loyalty programs and introducing, where practical, in-store beauty services.

Further Reading from FGRT

Readers may also be interested in the following reports:

The Millennials Series: Millennials and Beauty

Deep Dive: Gen Z and Beauty—the Social Media Symbiosis

Deep Dive: Global Beauty E-Commerce—a Highly Attractive Market

Deep Dive: Active M&A in the Beauty Space Fuels Future Growth

Beauty Loyalty Programs: Sephora vs. Ulta

The 21st-Century Drugstore: US Drugstores Fighting for Share in a Shifting Beauty Market