DIpil Das

Introduction

This report presents the results of Coresight Research’s latest weekly survey of US consumers on the coronavirus outbreak, undertaken on May 13. This report explores the trends we are seeing from week to week, following prior surveys on May 6, April 29, April 22, April 15, April 8, April 1, March 25 and March 17–18.Looking Beyond Lockdown

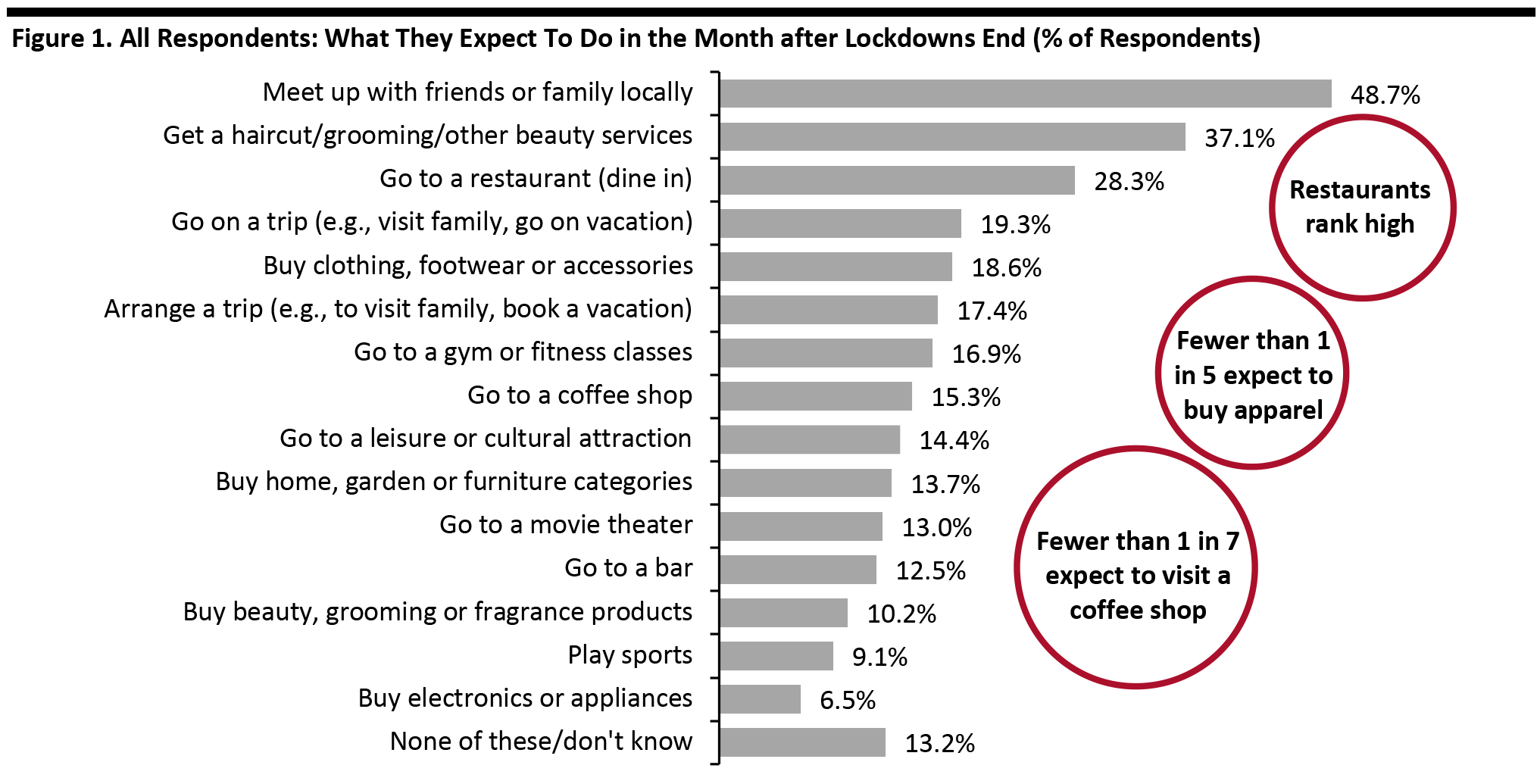

A Haircut Is Top of Many Consumers’ Wishlists This week, we asked what consumers would do in the month after lockdowns end, giving them a choice of 15 options (and none/don’t know). The ranking: Of the options related specifically to spending, getting a haircut or other grooming/beauty treatment is top, followed by dining in a restaurant—which we think ranks relatively high, given it may be perceived to be higher-risk than a number of other options (such as shopping). The ranking of discretionary retail purchases, such as for apparel, beauty or home goods, are mixed. Absolute numbers: The absolute percentages are low—despite weeks of lockdowns and our question asking about a full month after lockdowns, only a little over one in three respondents expect to get a haircut (or other treatment) and around one in five to buy apparel. Few will be turning to coffee shops, with fewer than one in seven expecting to do so in the whole month after lockdowns. This is despite around 87% overall stating that they would do at least one of these things post lockdown—suggesting that consumers do not expect to remain in full lockdown mode but to return to regular activities very selectively. The figures add weight to expectations of a very gradual recovery post lockdown, with shoppers taking tentative steps back to leisure activities and discretionary spending. [caption id="attachment_109768" align="aligncenter" width="700"] Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

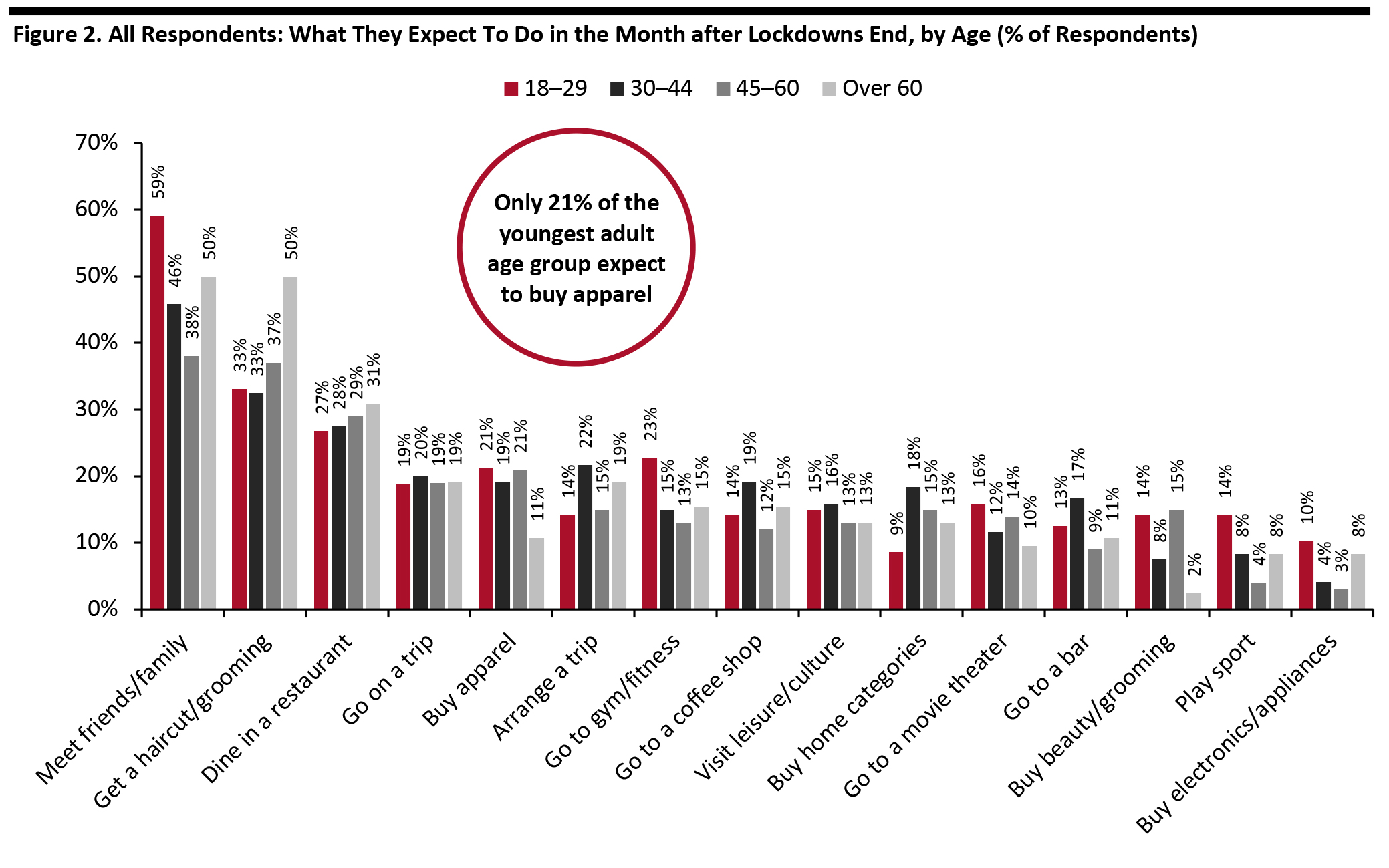

Source: Coresight Research [/caption] Younger consumers are more likely than average to meet friends or family and go to the gym, while getting a haircut or dining out peak among older age groups. Younger consumers are more likely than the oldest age group to buy apparel—but the proportion expecting to do this being broadly similar among all age groups under 60. Young consumers drive a great deal of fashion spending, so this finding may prove disappointing to apparel retailers. [caption id="attachment_109802" align="aligncenter" width="700"]

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

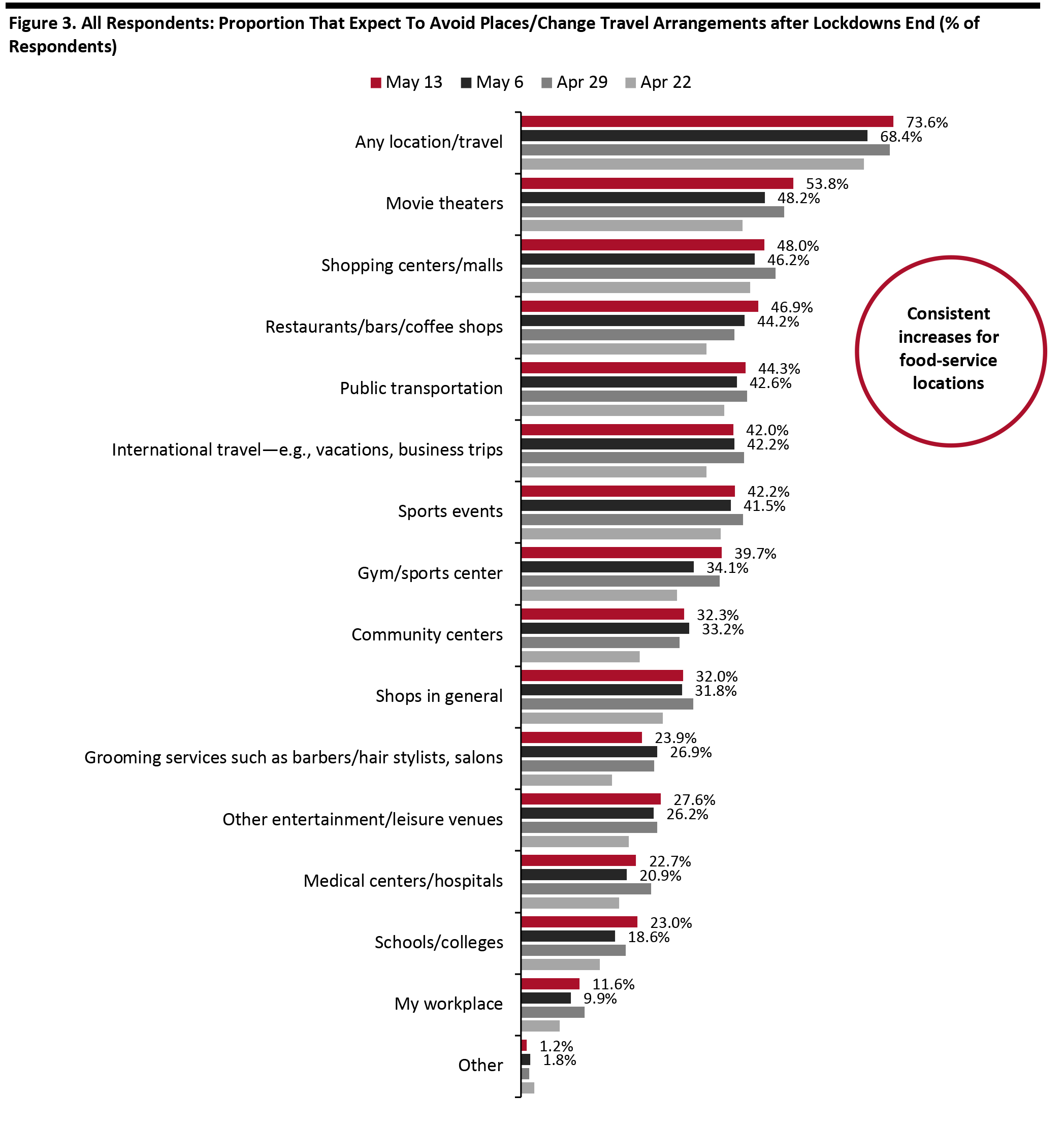

Source: Coresight Research [/caption] Almost Half Expect To Avoid Shopping Centers This week, 73.6% of all respondents anticipated avoiding some kind of public place or travel after lockdowns end. This compares to 68.4% last week, continuing a yoyoing pattern we have seen week to week. The significant swings this week were in expected avoidance of movie theaters or gyms/fitness centers—each of which saw an increase of over five percentage points. Shopping centers/malls saw a 1.8-percentage-point increase, week over week, which is within the margin of error; around half of all consumers continue to expect to avoid shopping centers/malls. The one consistent pattern in this data set has been the upward trend for avoidance of food-service businesses. [caption id="attachment_109770" align="aligncenter" width="700"]

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption] By age, we saw significant increases in expected avoidance across all age groups, week over week, with the exception of the 45–60 age group. Some 69% of those aged 45–60 expect to avoid any public place or travel post lockdown; across all other age groups, avoidance rates were at 75% this week. More Shoppers Expect Long-Term Impacts We asked three questions in which respondents were required to estimate the timescale of coronavirus impacts.

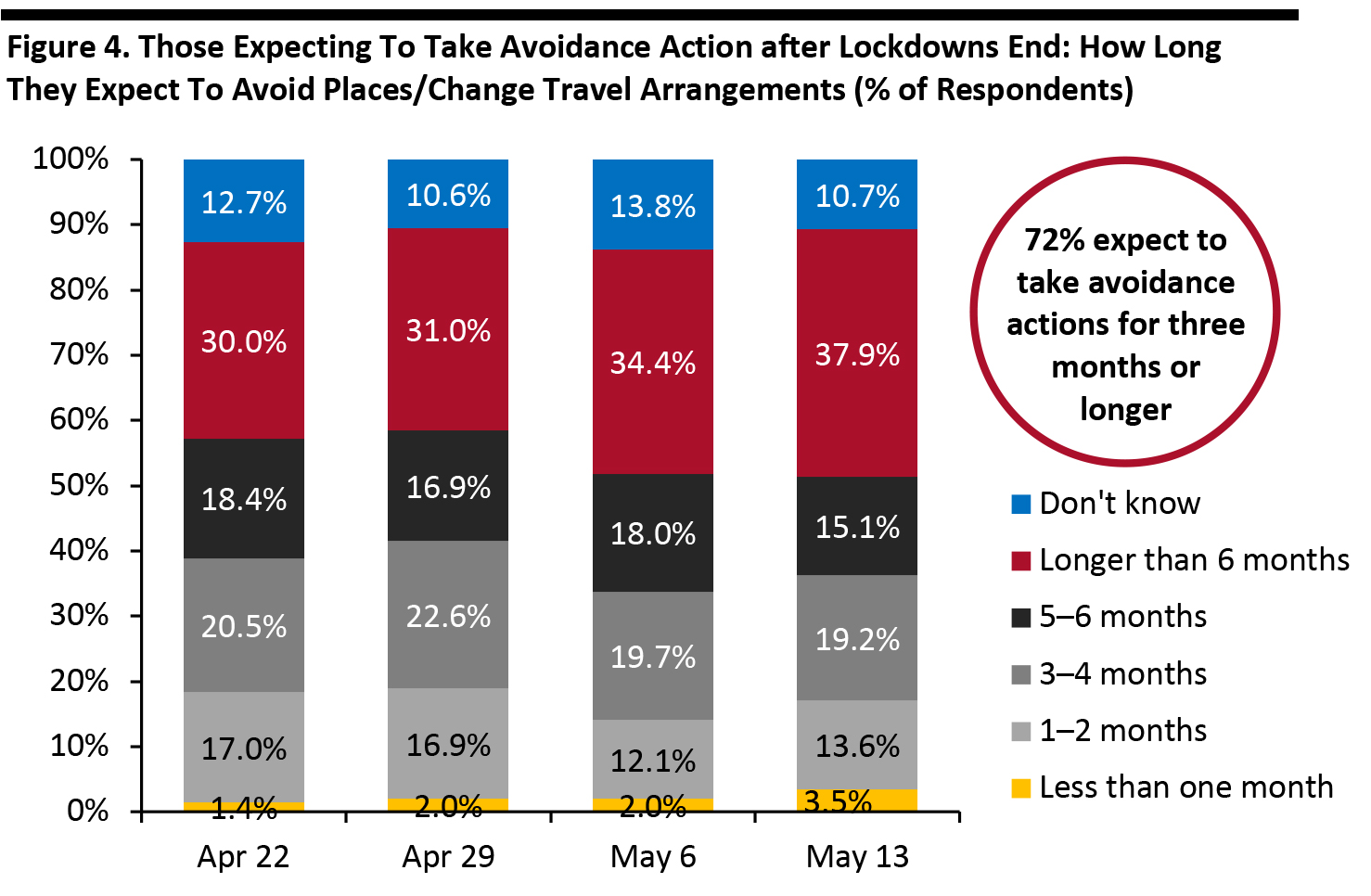

- We asked those respondents who expect to take avoidance action how long they expect to be doing so for.

- We asked those making fewer or more purchases of any categories how long they expect it will be before their spending bounces back to normal levels.

- We asked all respondents how long they think the severe effects of the outbreak will impact life in the US.

Base: US Internet users aged 18+ who expect to avoid places/change travel arrangements after lockdowns end

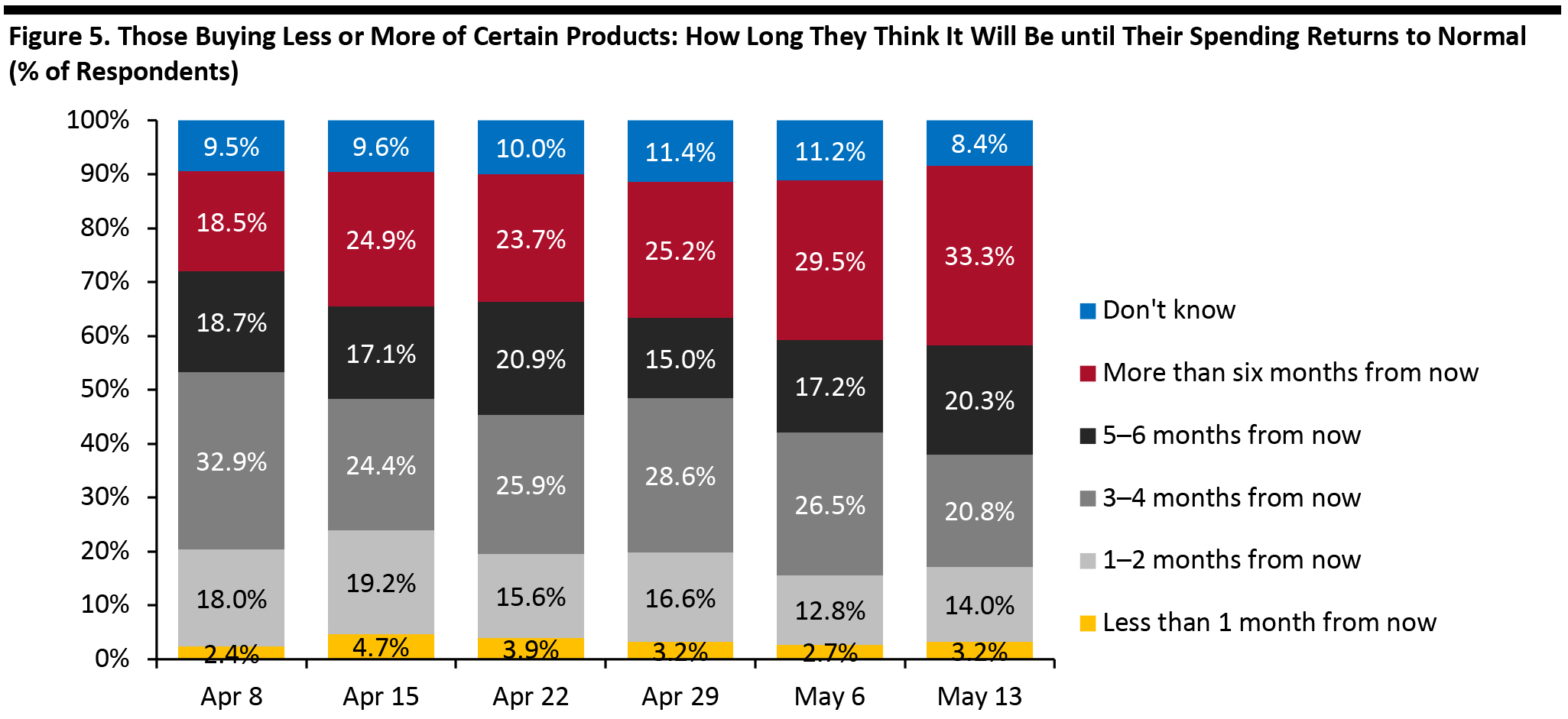

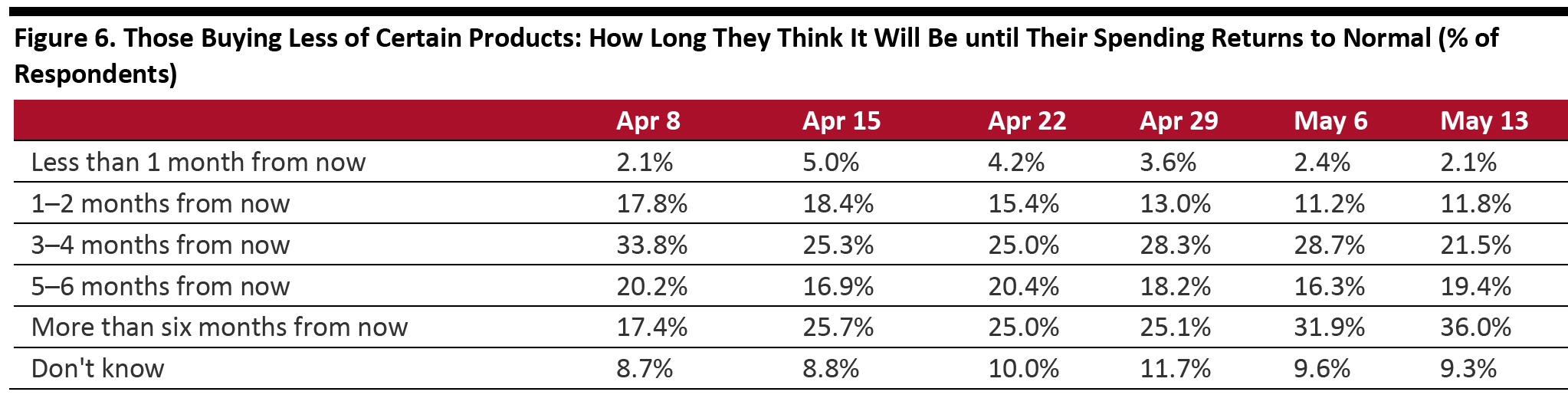

Base: US Internet users aged 18+ who expect to avoid places/change travel arrangements after lockdowns end Source: Coresight Research [/caption] Spending Bounce Back: One-Third Expect To Retain Changed Spending Patterns for More Than Six Months Similarly, we continue to see a steady increase in the proportion of respondents anticipating longer-term impacts on their spending. Among those who have changed their spending levels—either buying more or less of any categories—exactly one-third expect it to be more than six months from now before their spending patterns return to normal, up from just under 30% last week. That six-month-plus window takes us up to the second half of November at the earliest—the start of holiday season. A total of 74% expect to keep changed purchasing levels for three months or more, versus 73% last week. We see slightly higher expectations of a long-term impact among those making fewer purchases: 36.0% of this group expect to return to pre-crisis spending patterns only in more than six months’ time (Figure 6).

- We show what consumers are buying more of and less of in a separate section, later in this report.

Base: US Internet users aged 18+ who are purchasing any products more or less, because of the coronavirus outbreak

Base: US Internet users aged 18+ who are purchasing any products more or less, because of the coronavirus outbreak Source: Coresight Research [/caption] [caption id="attachment_109773" align="aligncenter" width="700"]

Base: US Internet users aged 18+ who are purchasing any products less, because of the coronavirus outbreak Totals may not sum due to rounding

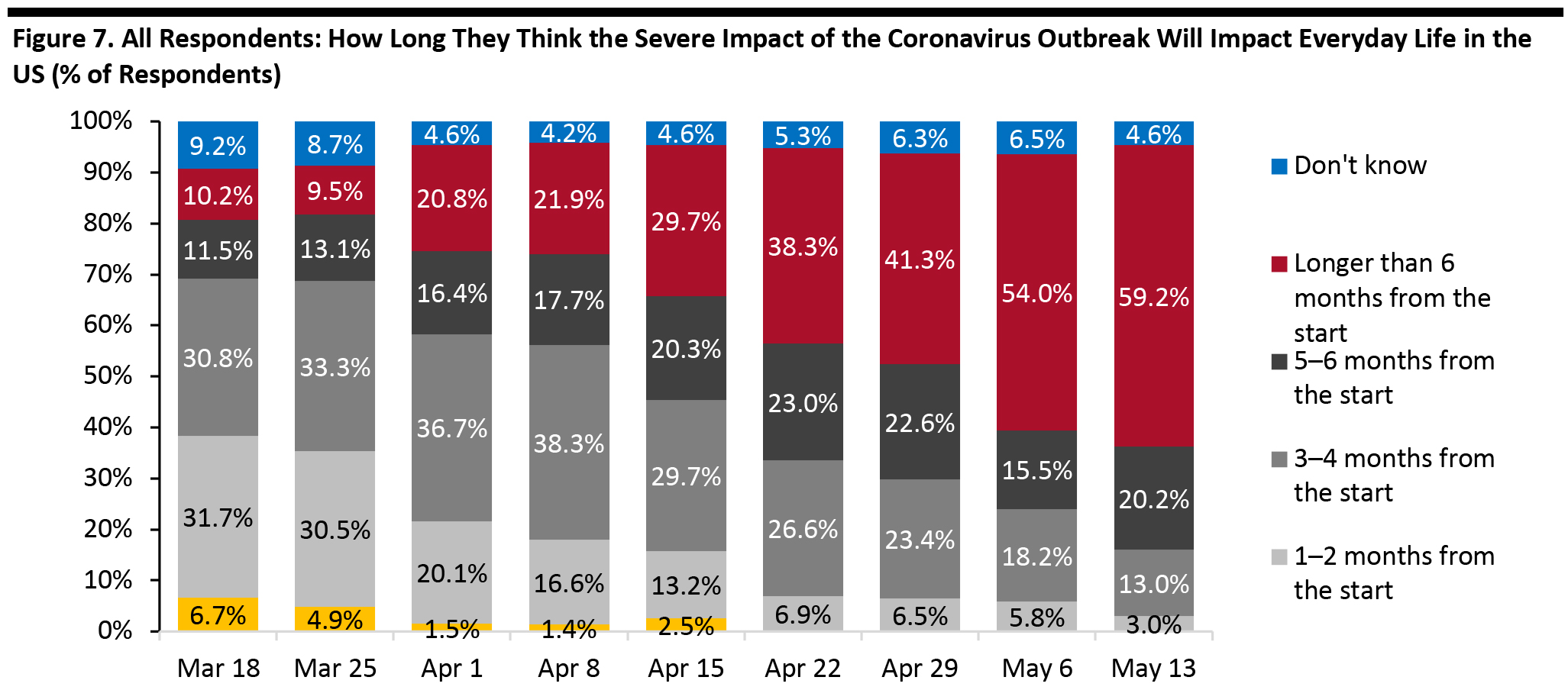

Base: US Internet users aged 18+ who are purchasing any products less, because of the coronavirus outbreak Totals may not sum due to rounding Source: Coresight Research [/caption] Impact on Everyday Life: Over Half of Consumers Expect the Crisis To Last More Than Six Months Echoing the trends noted above, consumers’ expectations of the length of the crisis increased again this week, after jumping last week. Fully 59.2% now expect the severe impact of the outbreak to last more than six months from its start, up from 54.0% last week. Some 92.4% expect the severe impact to last three months or more, broadly level with 87.7% last week. [caption id="attachment_109774" align="aligncenter" width="700"]

Base: US Internet users aged 18+

Base: US Internet users aged 18+ *Not provided as an option after April 15

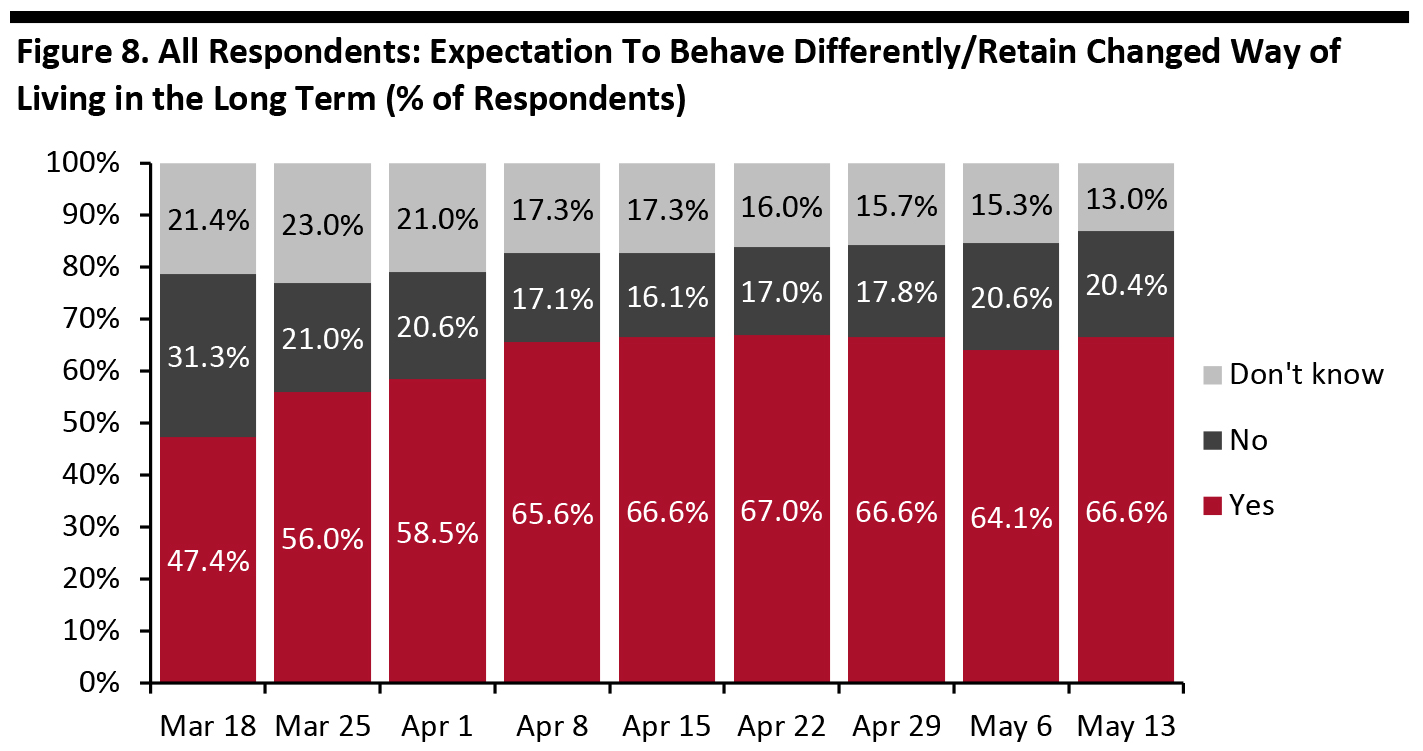

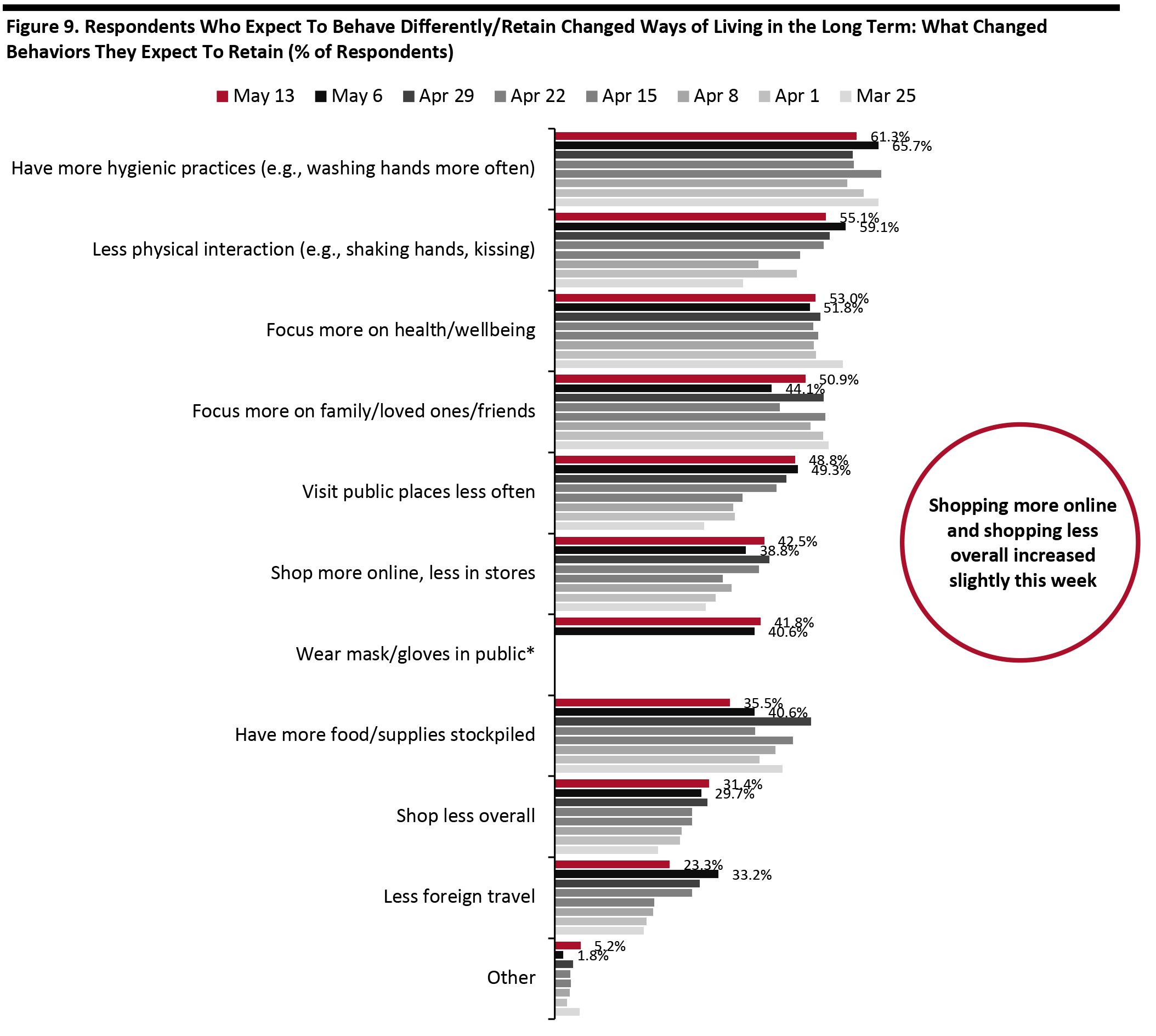

Source: Coresight Research [/caption] Two-Thirds Expect To Retain Changed Behaviors for the Long Term Each week, we ask respondents whether they think they will keep some of the behaviors they have adopted during the coronavirus crisis. In recent weeks, this metric has leveled off at around two-thirds of all consumers expecting to retain some behaviors over the long term. [caption id="attachment_109775" align="aligncenter" width="700"]

Base: US Internet users aged 18+

Base: US Internet users aged 18+ Source: Coresight Research [/caption] Among those expecting to retain changed behaviors, we have seen consistent or near-consistent upward trends in:

- Less physical interaction—although this eased a little this week, the overall upward trend reflects a growing realization that post-lockdown normality will involve physical distancing.

- Visiting public places less often—similarly, this moderated this week, but the general trend again reflects greater awareness that social distancing will be necessary. This is likely to hit shopper traffic to brick-and-mortar retail formats, but could help retailers to enforce social distancing in stores in the near term.

Respondents could select multiple options

Respondents could select multiple options *Not provided as an option before May 6

Base: US Internet users aged 18+ who expect to behave differently in the long term/retain changed ways of living from the outbreak

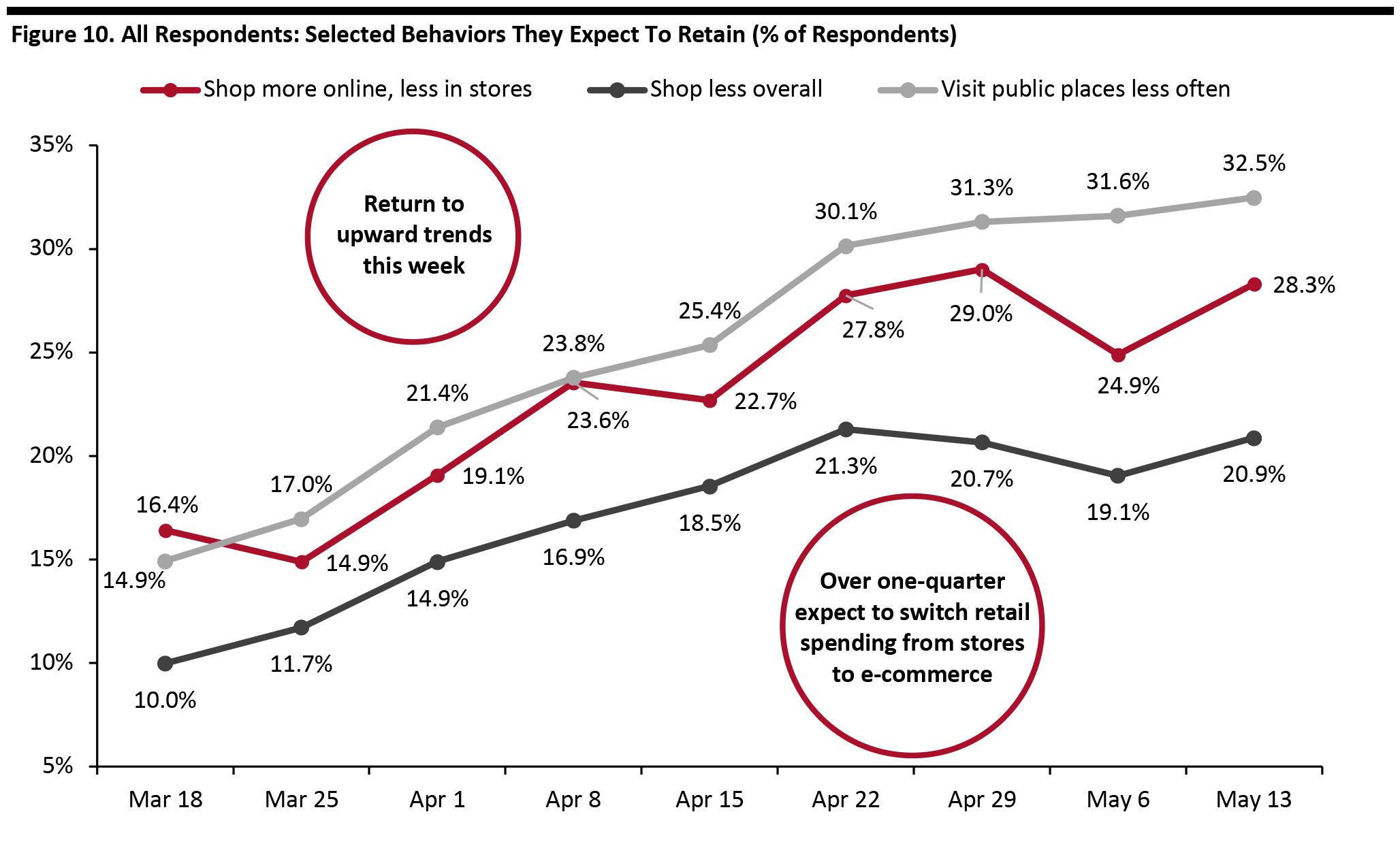

Source: Coresight Research [/caption] In the chart below, we focus on trending data in three of the metrics charted above. We represent these as a proportion of all respondents, to represent consumers overall, rather than as a proportion of those expecting to retain changed behaviors (which is what is charted above). Rebased to all respondents, the overall upward trends are more distinct—and these trends returned this week after tending to moderate in the last week or two. Spelling bad news for brick-and-mortar retail in particular, around one in five respondents expect to shop less overall; over one-quarter expect to switch shopping from stores to e-commerce; and almost one in three expect to visit public places less often. [caption id="attachment_109803" align="aligncenter" width="700"]

Base: US Internet users aged 18+

Base: US Internet users aged 18+ Source: Coresight Research [/caption]

Reviewing Trend Data in Purchasing Behavior

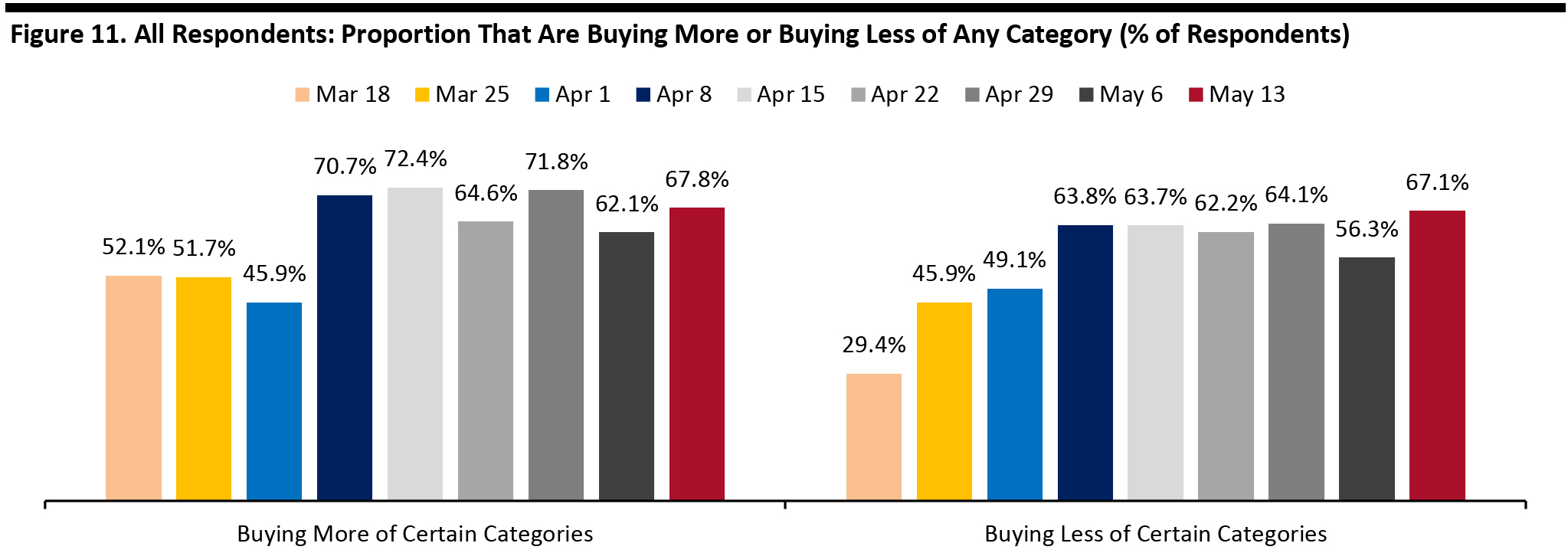

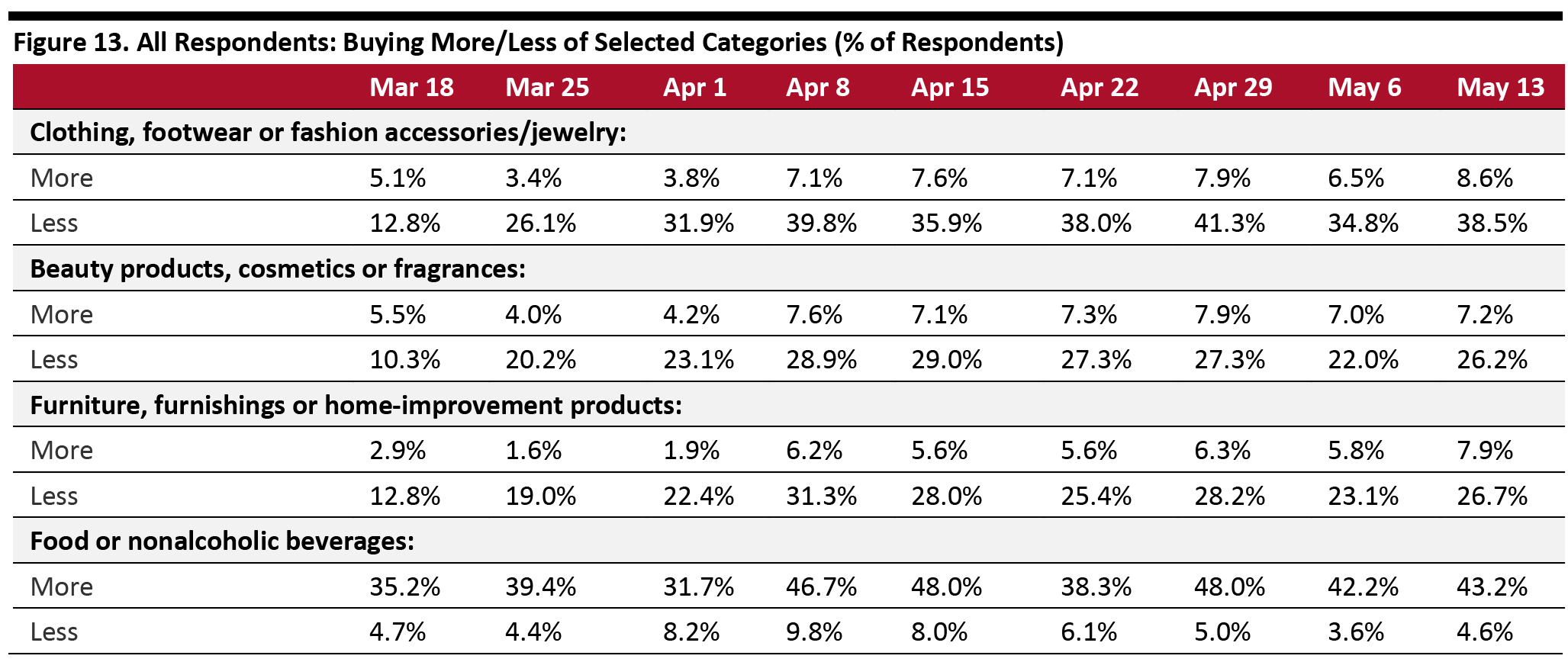

What They Are Buying More Of and Less Of This week, around two-thirds of respondents said they were buying more or less of any categories due to the outbreak. We show the category breakdown later.- Note, buying more of certain categories and buying less of certain categories were not mutually exclusive options, so respondents could answer yes to both.

Base: US Internet users aged 18+

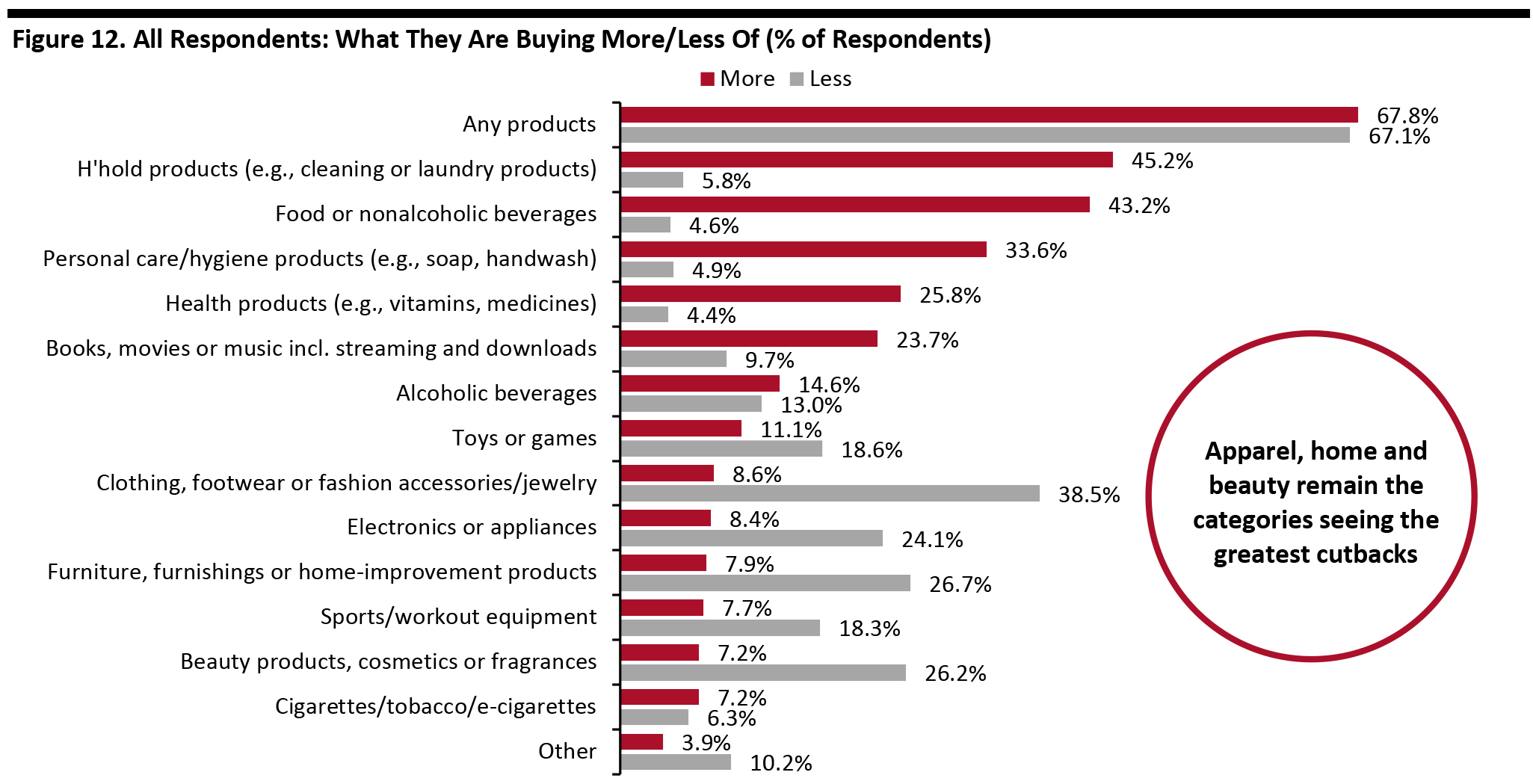

Base: US Internet users aged 18+ Source: Coresight Research [/caption] Buying more: Alongside food and other essentials, media products and streaming are net beneficiaries of the crisis. Buying less: Apparel continues to be the number-one category for cutbacks, with 38.5% of respondents this week saying they had reduced purchases, versus 34.8% last week—although the trend for apparel has proved volatile in recent weeks, so we should avoid reading too much into a one-week swing. We show trended data in Figure 13. Ratio of less to more: The ratio of those purchasing less to those purchasing more for clothing and footwear stood at 4.5 this week versus 5.3 last week. The ratio for furniture, furnishings and home improvement was 3.4 this week versus 4.0 last week. Beauty products stood at 3.6 this week versus 3.2 last week. [caption id="attachment_109779" align="aligncenter" width="700"]

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption] [caption id="attachment_109780" align="aligncenter" width="700"]

Base: US Internet users aged 18+

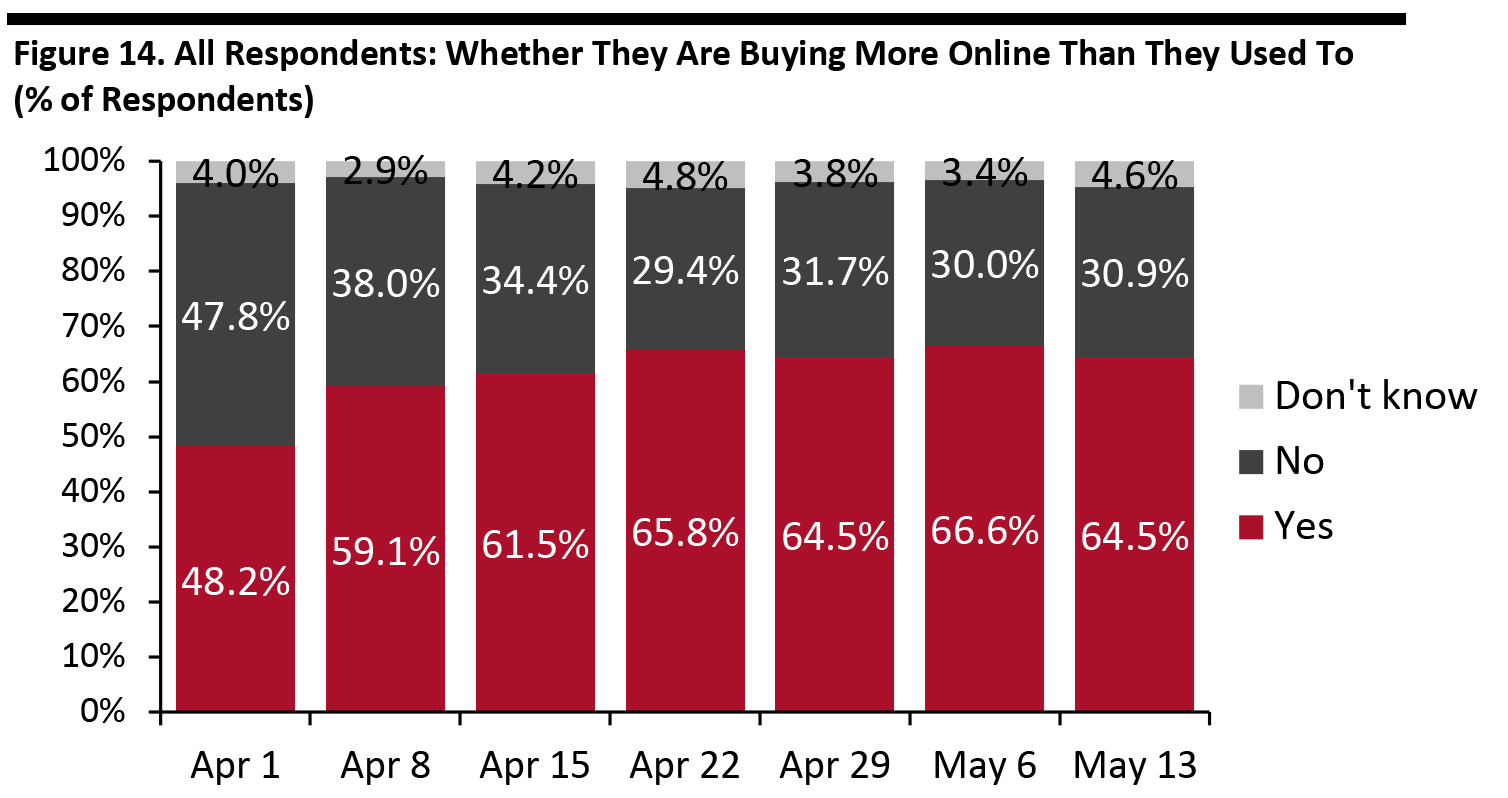

Base: US Internet users aged 18+ Source: Coresight Research [/caption] Two-Thirds Are Switching Spending Online The proportion of consumers switching spending to e-commerce has broadly leveled off, at two-thirds. This plateauing suggests that lockdown shopping habits have settled down after earlier fluctuations. [caption id="attachment_109781" align="aligncenter" width="700"]

Base: US Internet users aged 18+

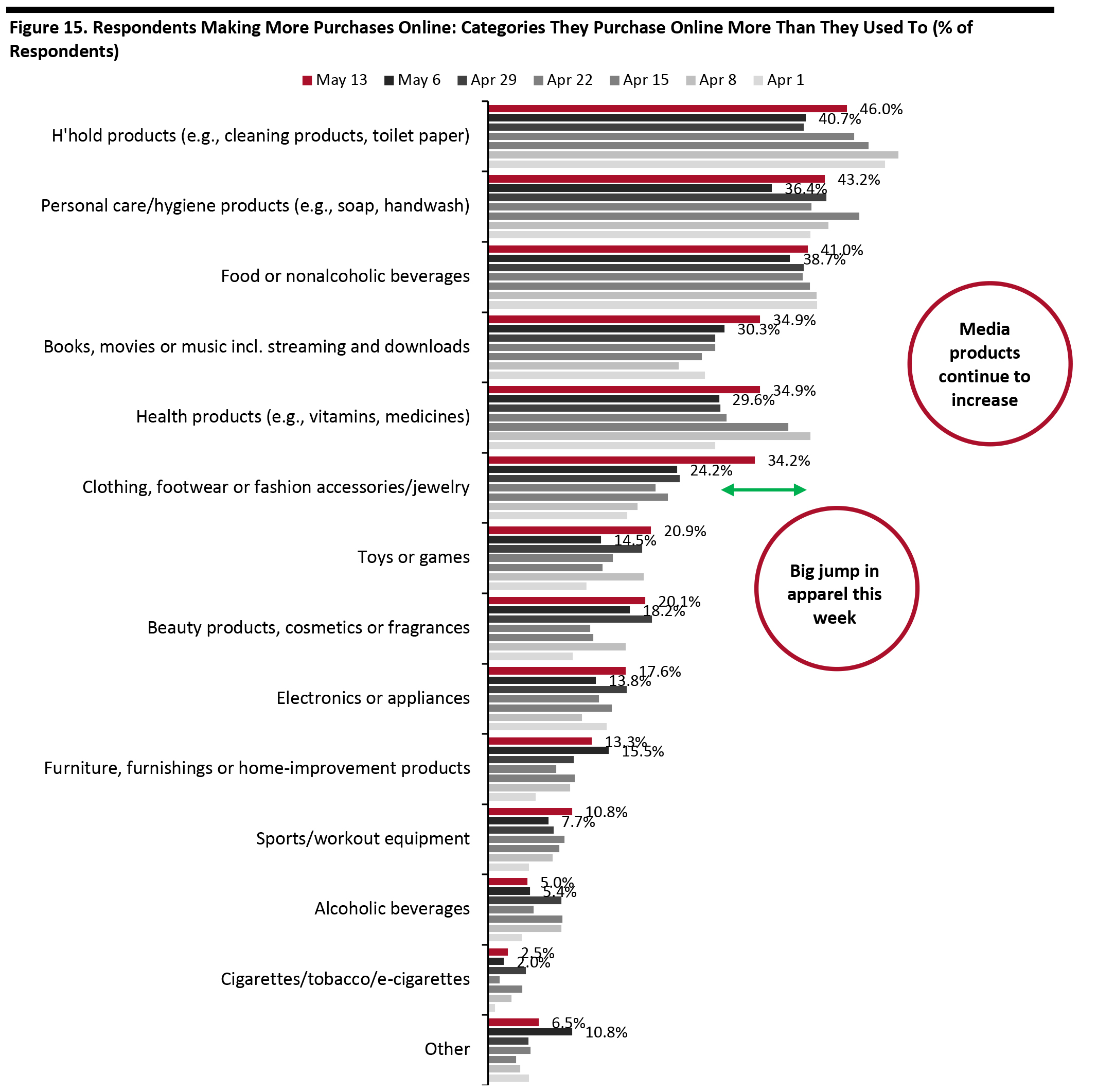

Base: US Internet users aged 18+ Source: Coresight Research [/caption] What They Are Buying More Of Online: Big Leap for Apparel Among the respondents making more purchases online, we saw a sizeable upswing for clothing, footwear and accessories:

- Week over week, we recorded a 10-percentage-point increase in the proportion of respondents buying apparel online more than they used to, to 34.2%.

- Versus April 1, when we began asking this question, we have seen a 16-percentage-point increase in the proportion of respondents buying more apparel online.

Respondents could select multiple options

Respondents could select multiple options Base: US Internet users aged 18+ who make more purchases online than they did before the coronavirus outbreak

Source: Coresight Research [/caption]

Employment and Income Concerns

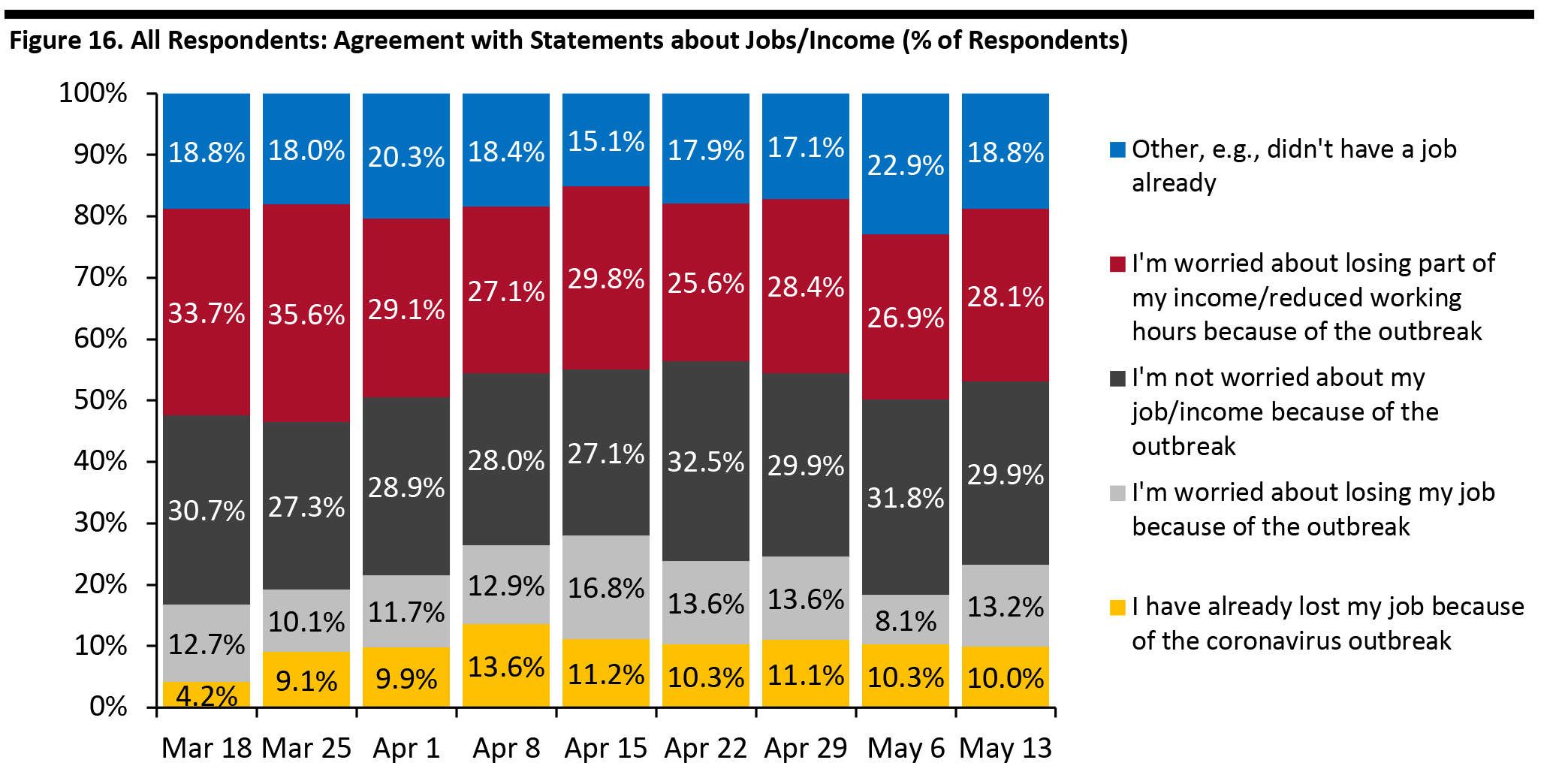

Each week, we ask respondents to choose from a selection of statements related to employment and income. We have seen some fluctuation in the proportion of respondents worried about what may happen. This week, a total of 41.3% were worried about losing their job or part of their income, versus 35.0% last week. [caption id="attachment_109783" align="aligncenter" width="700"] Base: US Internet users aged 18+

Base: US Internet users aged 18+ Source: Coresight Research [/caption]