DIpil Das

The coronavirus crisis dealt a significant blow to most discretionary retail sectors, including apparel, beauty and luxury. In this report, we discuss the implications for the US luxury market and how its recovery could play out, incorporating proprietary consumer survey data. We also look at the early rebound of the Chinese luxury consumer post crisis for potential learnings for the US market.

Base: US luxury shoppers aged 18+

Base: US luxury shoppers aged 18+

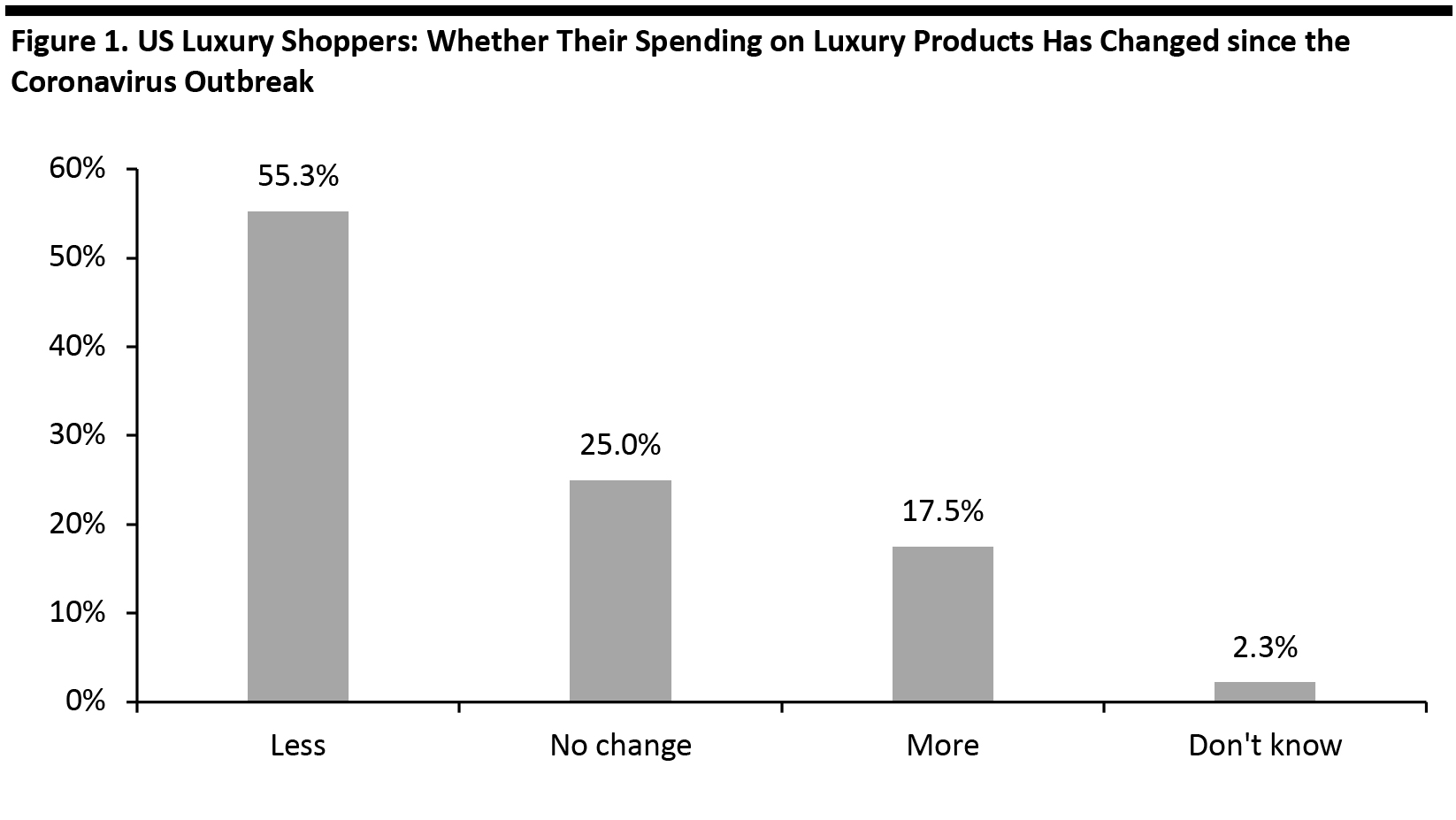

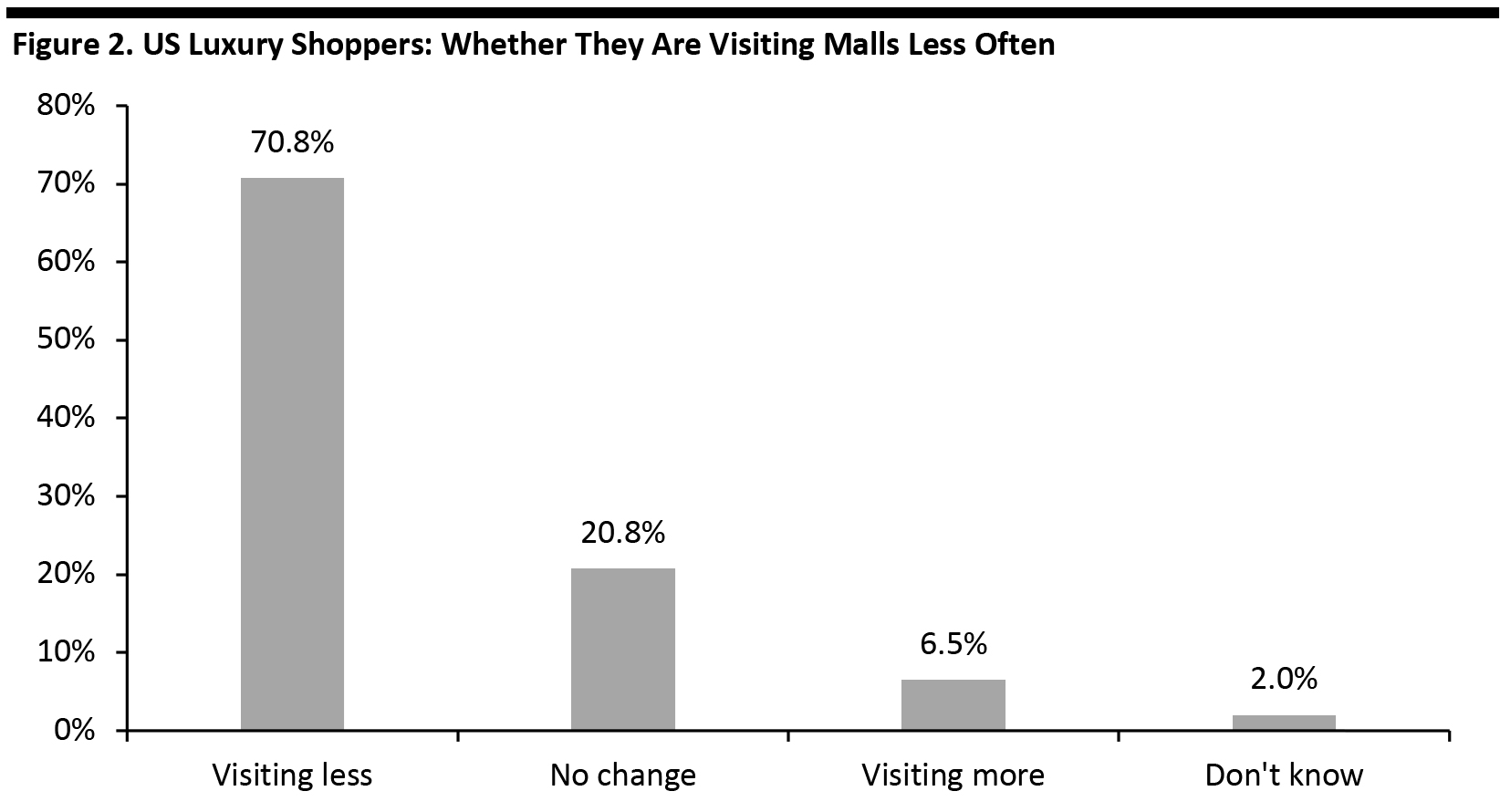

Source: Coresight Research [/caption] The retail shutdowns in the US from mid-March also reduced spending opportunity in all discretionary sectors, but with luxury lagging other categories in the adoption of digital retail—having only embarked on an e-commerce/omnichannel strategy in the past five or so years—sales retention by luxury companies was severely inhibited during lockdowns. The reported decline in consumer spending also reflects economic uncertainty: The performance of the stock market is a factor in driving luxury spending for nearly 20% of survey respondents. Notably, 67% of respondents in the $175,000–$200,000 annual income bracket stated that the stock market affects their luxury spending; the wealth effect exerts more than three times the average impact on this cohort. Although stores and malls in the US are now gradually reopening (as we discuss later in this report), most of our survey respondents reported that they are visiting shopping malls less often than prior to the crisis, according to our survey—reflecting that health concerns persist. [caption id="attachment_112378" align="aligncenter" width="700"] Base: US luxury shoppers aged 18+

Base: US luxury shoppers aged 18+

Source: Coresight Research [/caption] Respondents could select multiple options Base: US Internet users aged 18+

Respondents could select multiple options Base: US Internet users aged 18+

Source: Coresight Research [/caption] Furthermore, our conversations with executives at numerous luxury brands in the US reveal that during lockdowns, consumers had been engaging with brands online and via other touchpoints—such as through social media, by placing orders over the phone and by making video-call shopping appointments with store associates—and they have expressed eagerness to return to stores when it is safe to do so. One global luxury brand told Coresight Research, “Our clients have not stopped shopping and are calling regularly to complete a purchase and arrange for its receipt.” Another luxury executive told us that “the luxury shopper is fine; it’s the stores that are closed. Address their top concerns of safety and health and they will return to stores and spend. Meanwhile, consumers have happily adapted to alternative methods of making purchases.” Store Reopenings Luxury retailers and department stores have begun to reopen brick-and-mortar locations as states lift shelter-in-place restrictions (see Figure 4). Figure 4. Post-Crisis Luxury: Store Reopenings in the US [wpdatatable id=297]

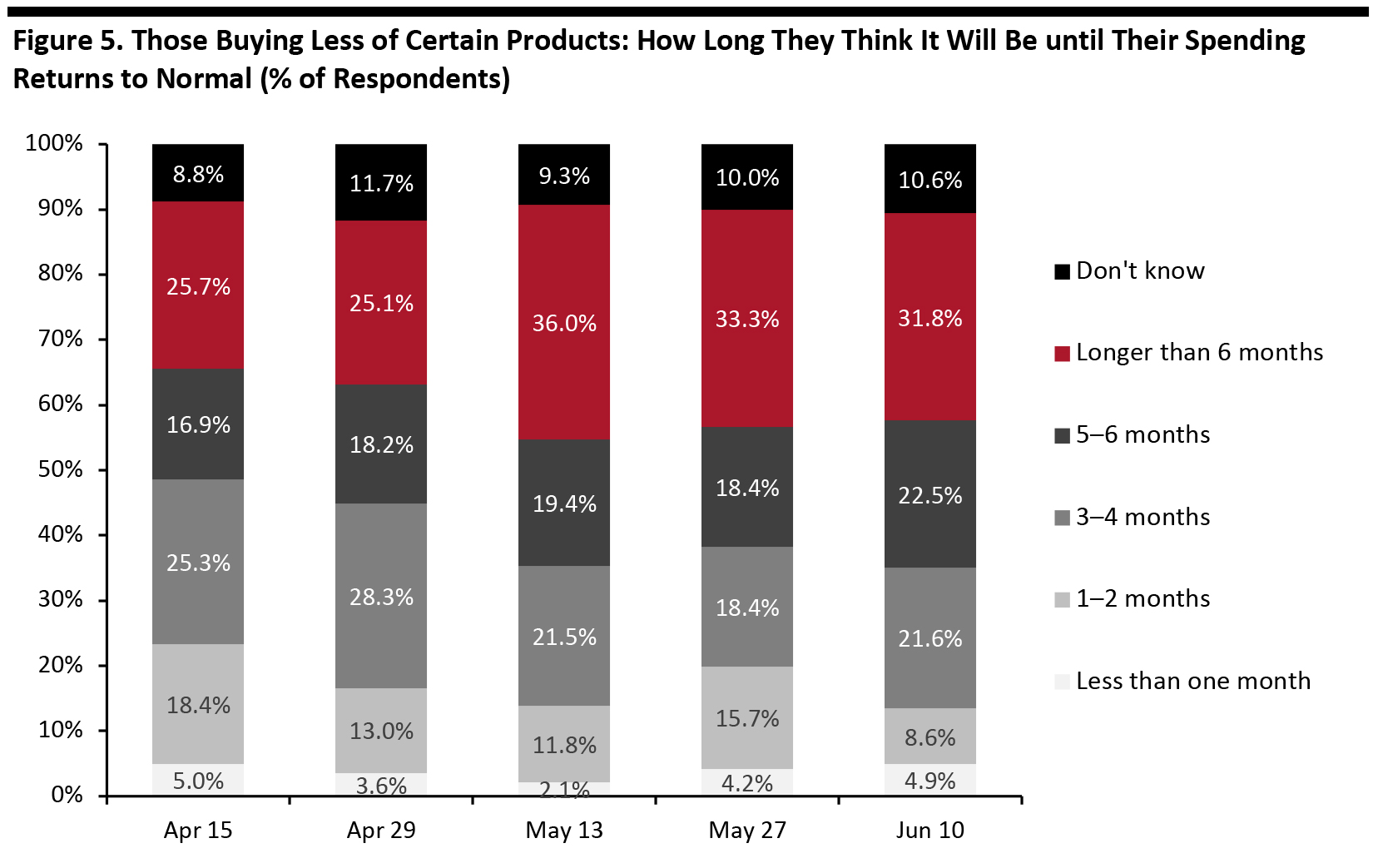

Source: Company reports So far, a number of reopened US apparel and luxury retailers have reported stronger sales than expected at reopened stores, exhibiting pent-up demand for nonessential goods and shopping in physical locations. After a few months of quarantine and self-imposed isolation, consumers desire social interaction in retail formats if they perceive it to be safe. This bodes well for many monobrand luxury shops that are palatial in size and can easily support appointment selling—two attributes that help mitigate the perceived risk of infection. Base: US Internet users aged 18+ who are purchasing any products less, because of the coronavirus outbreak Totals may not sum due to rounding

Base: US Internet users aged 18+ who are purchasing any products less, because of the coronavirus outbreak Totals may not sum due to rounding

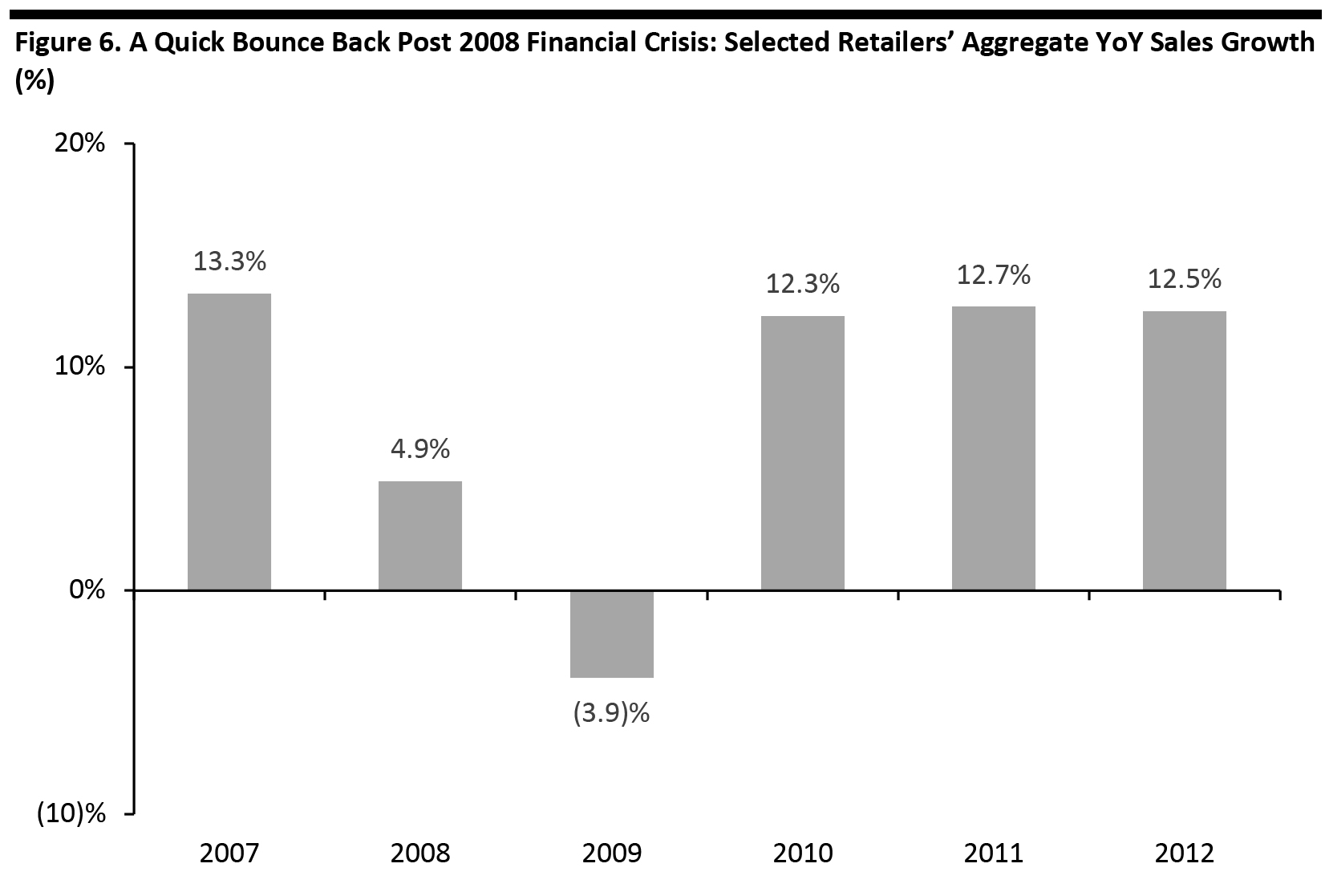

Source: Coresight Research [/caption] Looking back to the 2008 financial crisis further informs our estimates of the luxury sector’s recovery following Covid-19. Selected luxury brands experienced only one year of an aggregate sales decline followed by a return to double-digit growth in 2010. Applying this to the current situation, we would see the 2020 crisis impact 2021 luxury growth, before the sector bounces back by 2022. [caption id="attachment_112381" align="aligncenter" width="700"] Selected retailers: Burberry, Hugo Boss, Kering, LVMH, Ralph Lauren, Richemont, Tapestry and Tiffany & Co.

Selected retailers: Burberry, Hugo Boss, Kering, LVMH, Ralph Lauren, Richemont, Tapestry and Tiffany & Co.

Source: S&P Capital IQ [/caption] Apple Store in Shanghai

Apple Store in Shanghai

Source: Coresight Research [/caption] [caption id="attachment_112383" align="aligncenter" width="700"] Shoppers line up to gain entry to a Louis Vuitton store in March 2020

Shoppers line up to gain entry to a Louis Vuitton store in March 2020

Source: Coresight Research [/caption] Luxury companies have also reported physical retail trends steadily improving in China since late February (see Figure 7). Figure 7. Luxury Goods Companies: Recent Management Commentary on Performance in China [wpdatatable id=299]

Source: Company Announcements/Coresight Research, WWD

The Heavy Impacts of the Coronavirus Pandemic

As in other nonessential retail categories, Covid-19 caused widespread store shutdowns in the luxury sector. Furthermore, major players in the industry announced the temporary closure of production facilities amid the crisis.- French luxury brand Chanel announced on March 19 that it would gradually close its production bases in three countries: France, Italy and Switzerland.

- French luxury brand Hermès temporarily closed 42 production bases.

Base: US luxury shoppers aged 18+ Source: Coresight Research [/caption] The retail shutdowns in the US from mid-March also reduced spending opportunity in all discretionary sectors, but with luxury lagging other categories in the adoption of digital retail—having only embarked on an e-commerce/omnichannel strategy in the past five or so years—sales retention by luxury companies was severely inhibited during lockdowns. The reported decline in consumer spending also reflects economic uncertainty: The performance of the stock market is a factor in driving luxury spending for nearly 20% of survey respondents. Notably, 67% of respondents in the $175,000–$200,000 annual income bracket stated that the stock market affects their luxury spending; the wealth effect exerts more than three times the average impact on this cohort. Although stores and malls in the US are now gradually reopening (as we discuss later in this report), most of our survey respondents reported that they are visiting shopping malls less often than prior to the crisis, according to our survey—reflecting that health concerns persist. [caption id="attachment_112378" align="aligncenter" width="700"]

Base: US luxury shoppers aged 18+ Source: Coresight Research [/caption]

Actions Taken by Luxury Companies To Help Fight Covid-19

With luxury shopping on pause during lockdowns, many retailers diverted parts of their operations to assist in battling the coronavirus pandemic.- LVMH Group (parent company of Dior, Givenchy, Guerlain, Louis Vuitton and other brands) announced on March 15 that its perfume and cosmetics production lines would produce hand sanitizers and disinfectants to help address such product shortages in France.

- Hermès announced on March 30 that is would donate €20 million ($22.5 million) to public hospitals in Paris, France, in addition to its donation of 31,000 masks and 30 tons of hand sanitizer produced by its fragrance manufacturing facility in Vaudreuil.

- Masks were donated and/or manufactured by numerous brands to assist in combating the coronavirus, including Guess, J.Crew, Kering, Madewell, Mitchell Gold + Bob Williams, Nordstrom, Off-White.

- L’Occitane has donated hand sanitizer and masks.

US Luxury Market: Signs of Recovery

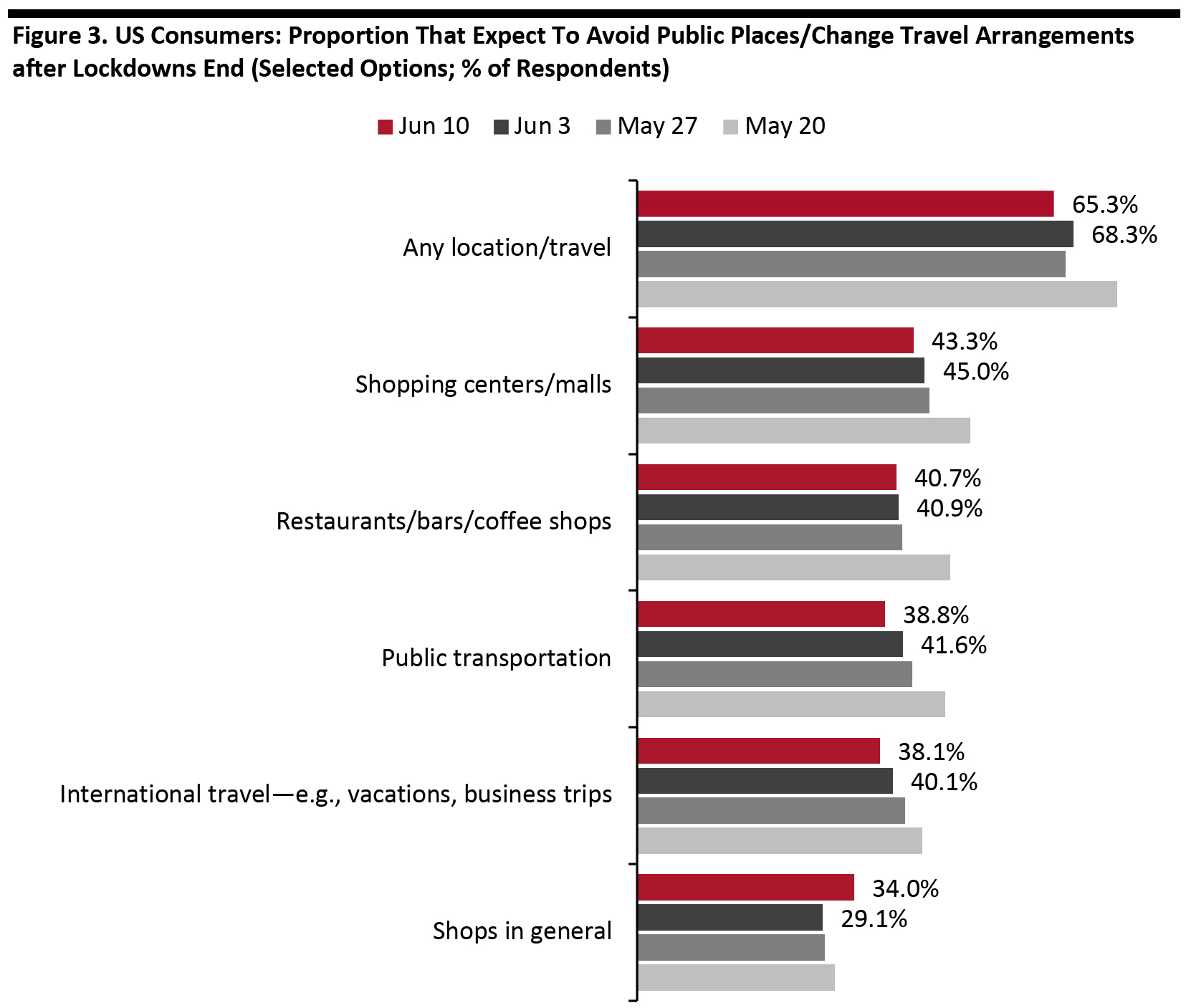

Consumer Sentiment Consumer sentiment in the US is stabilizing and showing initial signs of improvement, according to Coresight Research’s weekly surveys of US consumers: We have seen a recent decline in shoppers’ expectations to avoid shopping centers, public places and international travel (see Figure 3). We believe that expectations of avoidance behaviors have hit the nadir, and the optimistic signs of consumers returning to pre-crisis habits bodes well for all retail—and luxury specifically. [caption id="attachment_112379" align="aligncenter" width="700"] Respondents could select multiple options Base: US Internet users aged 18+ Source: Coresight Research [/caption] Furthermore, our conversations with executives at numerous luxury brands in the US reveal that during lockdowns, consumers had been engaging with brands online and via other touchpoints—such as through social media, by placing orders over the phone and by making video-call shopping appointments with store associates—and they have expressed eagerness to return to stores when it is safe to do so. One global luxury brand told Coresight Research, “Our clients have not stopped shopping and are calling regularly to complete a purchase and arrange for its receipt.” Another luxury executive told us that “the luxury shopper is fine; it’s the stores that are closed. Address their top concerns of safety and health and they will return to stores and spend. Meanwhile, consumers have happily adapted to alternative methods of making purchases.” Store Reopenings Luxury retailers and department stores have begun to reopen brick-and-mortar locations as states lift shelter-in-place restrictions (see Figure 4). Figure 4. Post-Crisis Luxury: Store Reopenings in the US [wpdatatable id=297]

Source: Company reports So far, a number of reopened US apparel and luxury retailers have reported stronger sales than expected at reopened stores, exhibiting pent-up demand for nonessential goods and shopping in physical locations. After a few months of quarantine and self-imposed isolation, consumers desire social interaction in retail formats if they perceive it to be safe. This bodes well for many monobrand luxury shops that are palatial in size and can easily support appointment selling—two attributes that help mitigate the perceived risk of infection.

- Capri Holdings began reopening its Americas and EMEA store fleets in May, and has since seen reopened store revenues reach 50–75% compared to the year-ago levels. Traffic at reopened stores is trending slightly better than expected, and conversion is meaningfully higher than expected, according to company management. Capri Holdings also reported that e-commerce growth accelerated significantly in the first quarter.

- At LVMH, the Covid-19 crisis impacted the second-quarter results in Europe and the US, but management expects to see a gradual recovery in the second half of 2020. Digital sales have increased by as much as 100% at some of LVMH’s brands this year, the company reported.

- During its shareholder call on June 2, Urban Outfitters reported that it had reopened two-thirds of its stores, with the remainder set to reopen by the end of June. Foot traffic and sales levels in reopened stores was tepid at first but improved each week. Digital online traffic and conversion has exploded since April, and the company believes that strong double-digit underlying demand could continue throughout the second quarter.

- According to a June 18 Reuters report, Chanel’s CFO said that some 85% of the group’s stores had reopened and that it had seen sales rebound in China—by over 100% in some weeks. Chanel also reported that shoppers were returning in Berlin, Milan and Paris too.

- By July 1, Macy’s had opened all but six locations, and initial sales trends as stores reopened were stronger than management expected. The company reported a few encouraging signs, including a steady, modest improvement in sales on a weekly basis at reopened stores as well as strong digital sales in each market.

- Less international travel—Our survey of US luxury consumers found that 30% of US shoppers' luxury spend is on purchases made while traveling abroad. This spending may be diverted to the domestic luxury sector in 2020 and 2021 if consumers prove reluctant to travel in the wake of the crisis—which would benefit US luxury brands and retailers.

- Preference for product over experience—New products are the most important driver for luxury buying in the US, according to our survey of luxury shoppers, with 41% of respondents reporting that new products determine their luxury spending. Furthermore, with the coronavirus pandemic having caused many experiential venues—such as theatres, performing arts, museums, sports arenas and restaurants—to temporarily shut down, the secular trend of consumer preferences turning to experiences over product is likely to reverse. Prolonged social distancing restrictions will further fuel this trend, with experiential services typically being allowed to resume at later dates than retail in many US states. Luxury brands should be encouraged by Sotheby’s opening of the art market, with a record $363.2 million modern and contemporary live auction conducted on three continents simultaneously on June 29, 2020. This attests to consumer interest in expensive discretionary items despite the recent lockdown.

- Demand for enduring value—Looking back to the Great Recession of 2007–2009, we observe that consumers look for products that hold value following a destabilizing event. For example, fast fashion is superseded by classic silhouettes that are timeless and so hold longer-term value. Luxury brands with long heritage and superior quality build consumer trust and a sense of security—qualities that consumers desire during periods of uncertainty. Post Covid-19, we could see this trend benefit the luxury sector, and the Sotheby’s art auction mentioned above indicates that wealthy consumers are seeking enduring value.

- Omnichannel shopping—Over 80% of luxury shoppers make such purchases online, according to our proprietary survey. According to Mailonline.com and CNBC, e-commerce drives consumers to make a store visit, if only to avail store and curbside pickup services.

Base: US Internet users aged 18+ who are purchasing any products less, because of the coronavirus outbreak Totals may not sum due to rounding Source: Coresight Research [/caption] Looking back to the 2008 financial crisis further informs our estimates of the luxury sector’s recovery following Covid-19. Selected luxury brands experienced only one year of an aggregate sales decline followed by a return to double-digit growth in 2010. Applying this to the current situation, we would see the 2020 crisis impact 2021 luxury growth, before the sector bounces back by 2022. [caption id="attachment_112381" align="aligncenter" width="700"]

Selected retailers: Burberry, Hugo Boss, Kering, LVMH, Ralph Lauren, Richemont, Tapestry and Tiffany & Co. Source: S&P Capital IQ [/caption]

China Luxury Market: A Rapid Return of Demand

China experienced a rapid return in luxury demand as the coronavirus quarantine came to an end. Although the progression and containment of Covid-19 in China and the US have followed different trajectories, we can derive insights from Chinese luxury shopper behavior post lockdown to inform expectations for the US market.The following photos exhibit the return of the Chinese luxury shopper to the nation’s reopened shopping malls—offering hope for American luxury retailers. [caption id="attachment_112382" align="aligncenter" width="700"] Apple Store in Shanghai Source: Coresight Research [/caption] [caption id="attachment_112383" align="aligncenter" width="700"]

Shoppers line up to gain entry to a Louis Vuitton store in March 2020 Source: Coresight Research [/caption] Luxury companies have also reported physical retail trends steadily improving in China since late February (see Figure 7). Figure 7. Luxury Goods Companies: Recent Management Commentary on Performance in China [wpdatatable id=299]

Source: Company Announcements/Coresight Research, WWD