Nitheesh NH

[caption id="attachment_80296" align="aligncenter" width="640"] Source: Company reports/Coresight Research[/caption]

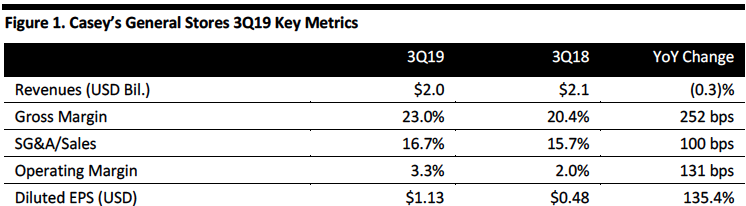

3Q19 Results

Casey’s General Stores reported 3Q19 revenue of $2.0 billion, down 0.3% year over year and below the consensus estimate of $2.2 billion. The company reported diluted EPS of $1.13, up 135.4% year over year and beating the consensus estimate of $0.87. Management attributed the strong growth in diluted earnings per share to effective operating expense control, a favorable fuel margin environment and continued focus on strategic pricing. The gross margin increased 252 bps year over year to 23.0%, and the operating margin increased 131 bps year over year to 3.3%.

Performance by Segment

Source: Company reports/Coresight Research[/caption]

3Q19 Results

Casey’s General Stores reported 3Q19 revenue of $2.0 billion, down 0.3% year over year and below the consensus estimate of $2.2 billion. The company reported diluted EPS of $1.13, up 135.4% year over year and beating the consensus estimate of $0.87. Management attributed the strong growth in diluted earnings per share to effective operating expense control, a favorable fuel margin environment and continued focus on strategic pricing. The gross margin increased 252 bps year over year to 23.0%, and the operating margin increased 131 bps year over year to 3.3%.

Performance by Segment

Source: Company reports/Coresight Research[/caption]

3Q19 Results

Casey’s General Stores reported 3Q19 revenue of $2.0 billion, down 0.3% year over year and below the consensus estimate of $2.2 billion. The company reported diluted EPS of $1.13, up 135.4% year over year and beating the consensus estimate of $0.87. Management attributed the strong growth in diluted earnings per share to effective operating expense control, a favorable fuel margin environment and continued focus on strategic pricing. The gross margin increased 252 bps year over year to 23.0%, and the operating margin increased 131 bps year over year to 3.3%.

Performance by Segment

- Fuel: 3Q19 revenue was down 4.9% year over year to $1.2 billion, with same-store sales by gallon down 3.4% year over year. However, total gallons sold in 3Q19 were up 2.7% year over year to 554.5 million gallons while gross profit increased 22.2% year over year to $122.6 million. The company attributed growth in gross profit to the company’s “balanced approach” to retail fuel pricing and to a favorable fuel margin environment. The total average fuel margin was 22.1 cents per gallon for the quarter.

- Grocery and Other Merchandise: 3Q19 revenue was up 2% year over year to $543.8 million. Same-store sales were up 3.4% year over year with a gross margin of 31.9%. Gross profit was up 8.3% to $173.5 million. Management believes accelerated same-store sales could help the company gain market share in this category.

- Prepared Food and Fountain: 3Q19 revenue was up 6.5% year over year to $256.1 million while total gross profit grew 9.6% to $159.7 million. Same-store sales were up 1.5% year over year and gross margin was up 180 basis points year over year to 3% in 3Q19, which management attributed to targeted price increases and favorable commodity prices.

- Same-store sales for fuel to be down 0.5-2.0% year over year.

- Same-store sales for grocery and other merchandise to increase 1.5-3.0% year over year.

- Same-store sales for prepared food and fountain to increase 1.5-3.5% year over year.

- To complete construction on 55-60 new stores by the end of FY19.

- To acquire at least 20 stores by the end of FY19.