Nitheesh NH

Introduction: A Technology Waiting to Change Retail

The blockchain is a relatively new technology which, since its inception in 2008, has been tested for applications in different sectors, from finance to logistics. In the near future, we expect the technology to start having a real impact on the retail industry, in operations such as supply chain and logistics, product provenance, e-commerce, payments, loyalty programs and customer data management.

This report gives an overview of blockchain technology and how it can contribute to making retailers’ operations more efficient, in particular how it can assist — in conjunction with other technologies — the digitalization of the supply chain and the way retailers interact with consumers.

We’ll look at how the technology can be used in retail and what blockchain-related projects retailers are already working on. We’ll look at notable startups for each application that can help retailers with the integration of the technology into their businesses.

How the Blockchain Can Disrupt Retail Operations

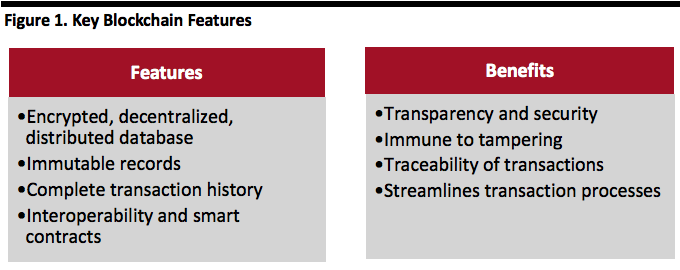

The blockchain is a distributed database that securely records transactions in a decentralized network using cryptography in a verifiable and permanent way. The technology eliminates the need for third-party verification, enables real-time information exchange, and is very secure since data recorded is encrypted.

A blockchain-based database is fully decentralized and distributed. This means it is open to all participants, each of which is responsible for verifying the data as well as storing the transaction record. Since each user has a copy of the ledger, this minimizes the risk of a single point of failure, increasing the overall security of the system.

Smart contracts — self-executing contracts that can be programmed on the blockchain — help streamline processes such as payments by removing the need for intermediaries. Figure 1 summarizes the main features and benefits of the blockchain.

[caption id="attachment_79389" align="aligncenter" width="580"] Source: Coresight Research[/caption]

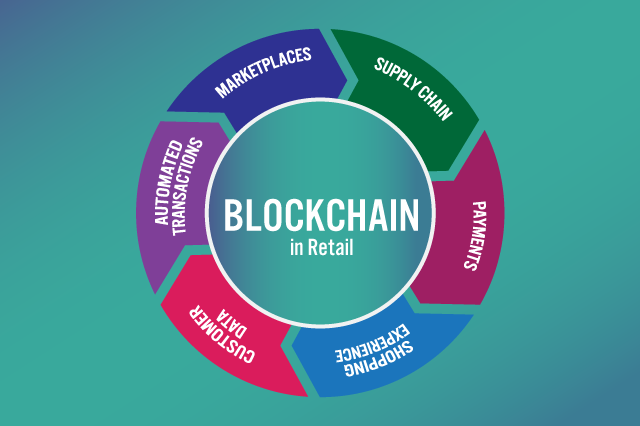

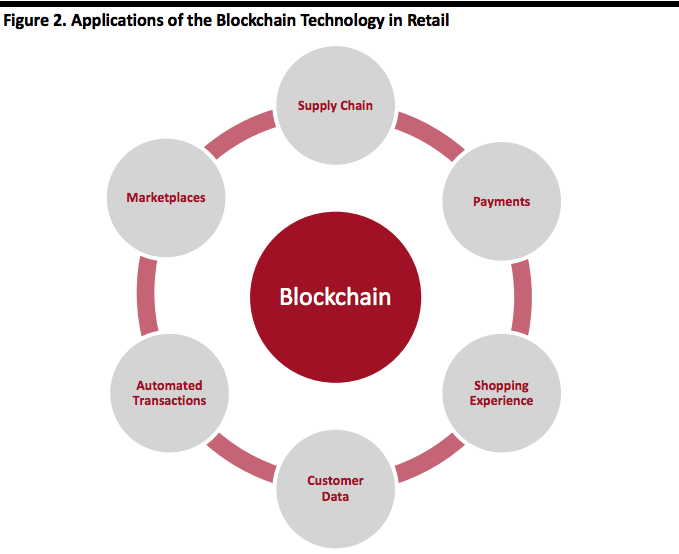

These features make blockchain technology attractive for applications in the retail space, particularly in support operations in supply chain and logistics, but also in customer data management, loyalty programs,Marketplaces and payments, as illustrated in figure 2.

[caption id="attachment_79390" align="aligncenter" width="580"]

Source: Coresight Research[/caption]

These features make blockchain technology attractive for applications in the retail space, particularly in support operations in supply chain and logistics, but also in customer data management, loyalty programs,Marketplaces and payments, as illustrated in figure 2.

[caption id="attachment_79390" align="aligncenter" width="580"] Source: Coresight Research[/caption]

We believe blockchain technology has the potential to improve all processes of digitalization in the supply chain and retail operations that currently use centralized systems. For example, digitalizing the supply chain entails using centralized Internet of Things (IoT) frameworks, which uses a central server – making it more vulnerable as there is one single point of failure that can be targeted. Data on the blockchain cannot be tampered once recorded, there is no single point of failure, since the system is run on multiple servers and there is no central authority that can arbitrarily modify the system without the consensus of the other parties.

Blockchain applications in retail are still at an early stage. Nevertheless, many companies are experimenting with the technology. A 2018 survey conducted by IBM among executives in retail and consumer goods from 203 organizations in 16 countries showed that 18% of companies have already started investing in the deployment of the technology in their business, while 70% of consumer industry executives surveyed expect to have a blockchain production network in three years. This shows most companies believe in the technology’s potential to have a real impact on the industry in the next few years.

Enhancing Supply Chain Traceability

Blockchain technology allows partners in the supply chain to track items accurately throughout the product cycle. This is particularly valuable when supporting highly fragmented and geographically dispersed sourcing systems in industries such as apparel, valuable items such as luxury goods, items at risk of counterfeiting such as pharmaceuticals, or perishables such as fresh food.

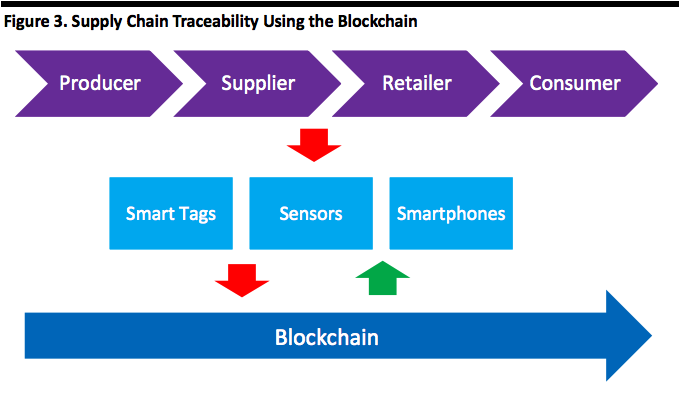

Figure 3 illustrates the application of the blockchain to enhance traceability within the supply chain. During the different stages of the product cycle, partners register the information on the status of the items through technologies such as smartphones, smart tags and sensors. All data is recorded on the blockchain, which guarantees that no party can alter historic entries, enabling trust without the need of an intermediary. Consumers can verify the provenance and authenticity of products by reading the information on the product cycle stored in the blockchain.

[caption id="attachment_79391" align="aligncenter" width="580"]

Source: Coresight Research[/caption]

We believe blockchain technology has the potential to improve all processes of digitalization in the supply chain and retail operations that currently use centralized systems. For example, digitalizing the supply chain entails using centralized Internet of Things (IoT) frameworks, which uses a central server – making it more vulnerable as there is one single point of failure that can be targeted. Data on the blockchain cannot be tampered once recorded, there is no single point of failure, since the system is run on multiple servers and there is no central authority that can arbitrarily modify the system without the consensus of the other parties.

Blockchain applications in retail are still at an early stage. Nevertheless, many companies are experimenting with the technology. A 2018 survey conducted by IBM among executives in retail and consumer goods from 203 organizations in 16 countries showed that 18% of companies have already started investing in the deployment of the technology in their business, while 70% of consumer industry executives surveyed expect to have a blockchain production network in three years. This shows most companies believe in the technology’s potential to have a real impact on the industry in the next few years.

Enhancing Supply Chain Traceability

Blockchain technology allows partners in the supply chain to track items accurately throughout the product cycle. This is particularly valuable when supporting highly fragmented and geographically dispersed sourcing systems in industries such as apparel, valuable items such as luxury goods, items at risk of counterfeiting such as pharmaceuticals, or perishables such as fresh food.

Figure 3 illustrates the application of the blockchain to enhance traceability within the supply chain. During the different stages of the product cycle, partners register the information on the status of the items through technologies such as smartphones, smart tags and sensors. All data is recorded on the blockchain, which guarantees that no party can alter historic entries, enabling trust without the need of an intermediary. Consumers can verify the provenance and authenticity of products by reading the information on the product cycle stored in the blockchain.

[caption id="attachment_79391" align="aligncenter" width="580"] Source: Coresight Research[/caption]

Retailers are already working for the implementation of blockchain platforms in their supply chain operations, often in collaboration with technology firms. Notable examples include:

Source: Coresight Research[/caption]

Retailers are already working for the implementation of blockchain platforms in their supply chain operations, often in collaboration with technology firms. Notable examples include:

Source: Provenance.org[/caption]

Companies can also use the traceability potential of the blockchain to prevent counterfeiting, a particularly valuable application in sectors such as luxury and pharmaceuticals:

Source: Provenance.org[/caption]

Companies can also use the traceability potential of the blockchain to prevent counterfeiting, a particularly valuable application in sectors such as luxury and pharmaceuticals:

Source: Coresight Research[/caption]

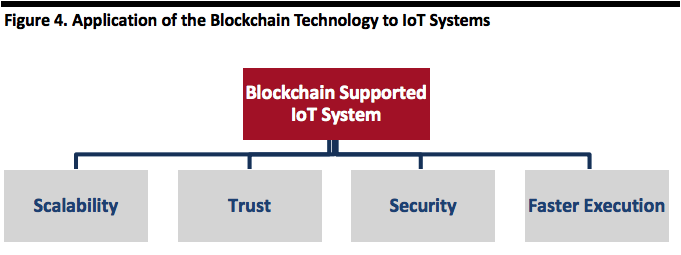

Companies including Fujitsu, Volkswagen, Hyundai and Bosch are testing the integration of the two technologies in their business operations. Hyundai, for example, is applying blockchain technology to enable effective communication, identification, authentication and data storage between IoT devices.

Examples of blockchain startups that have developed platforms specifically for the

integration of the blockchain with IoT include:

Source: Coresight Research[/caption]

Companies including Fujitsu, Volkswagen, Hyundai and Bosch are testing the integration of the two technologies in their business operations. Hyundai, for example, is applying blockchain technology to enable effective communication, identification, authentication and data storage between IoT devices.

Examples of blockchain startups that have developed platforms specifically for the

integration of the blockchain with IoT include:

Source: Streamr.com[/caption]

With greater control of their data thanks to the use of the blockchain technology, consumers could decide which company has access to their data and how the information is going to be used. Consumers could ask companies for incentives in exchange for the data they share, such as vouchers that could be spent on goods or services provided by the data recipient.

Enhancing Loyalty Programs Rewards and Effectiveness

Blockchain has the potential to disrupt the way companies manage loyalty programs. Retailers can use the technology to improve how they handle consumer data. With the support of the blockchain, consumers can use their reward points more effectively. The distributed nature of the blockchain can encourage loyalty scheme collaborations between companies which can prove beneficial for both retailers and consumers. The advantages of using a blockchain system to manage loyalty schemes include:

Source: Streamr.com[/caption]

With greater control of their data thanks to the use of the blockchain technology, consumers could decide which company has access to their data and how the information is going to be used. Consumers could ask companies for incentives in exchange for the data they share, such as vouchers that could be spent on goods or services provided by the data recipient.

Enhancing Loyalty Programs Rewards and Effectiveness

Blockchain has the potential to disrupt the way companies manage loyalty programs. Retailers can use the technology to improve how they handle consumer data. With the support of the blockchain, consumers can use their reward points more effectively. The distributed nature of the blockchain can encourage loyalty scheme collaborations between companies which can prove beneficial for both retailers and consumers. The advantages of using a blockchain system to manage loyalty schemes include:

Source: Overstock.com[/caption]

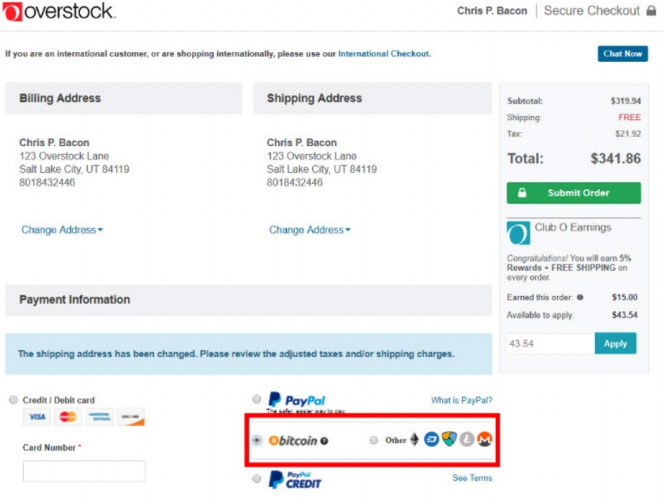

Increasing Payment Options

At its conception, the blockchain was conceived as a technology to enable payments without intermediaries such as financial institutions. In retail, the opportunity is to accept cryptocurrencies as a form of payment to add to other, more established, payment methods such as credit cards and cash.

However, there remain a number of challenges that stop major retailers from more widely adopting blockchain-based payment systems. Together with the uncertain legal status of cryptocurrencies in many countries, technical issues with the technology prevent significant adoption, including:

Source: Overstock.com[/caption]

Increasing Payment Options

At its conception, the blockchain was conceived as a technology to enable payments without intermediaries such as financial institutions. In retail, the opportunity is to accept cryptocurrencies as a form of payment to add to other, more established, payment methods such as credit cards and cash.

However, there remain a number of challenges that stop major retailers from more widely adopting blockchain-based payment systems. Together with the uncertain legal status of cryptocurrencies in many countries, technical issues with the technology prevent significant adoption, including:

Source: Overstock.com[/caption]

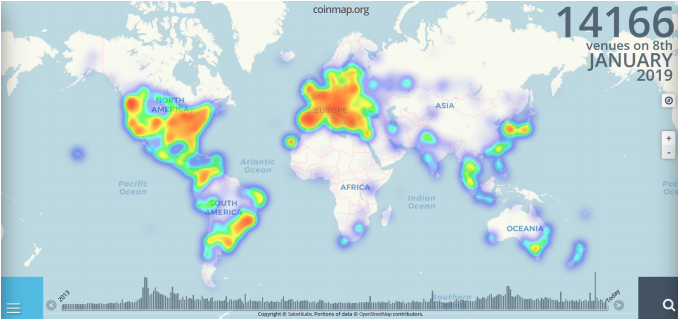

As of January 8, 2019, there were 14,166 venues accepting cryptocurrencies worldwide, according to Coinmap.org, a portal which shows the location of companies accepting cryptocurrencies worldwide.

[caption id="attachment_79397" align="aligncenter" width="580"]

Source: Overstock.com[/caption]

As of January 8, 2019, there were 14,166 venues accepting cryptocurrencies worldwide, according to Coinmap.org, a portal which shows the location of companies accepting cryptocurrencies worldwide.

[caption id="attachment_79397" align="aligncenter" width="580"] Source: Coinmap.org[/caption]

Developers are working to solve the problems that prevent cryptocurrency payment adoption. For example, the introduction of Lightning Network in 2018 — a second layer payment protocol that operates on top of a blockchain — have increased the speed of transactions and reduced costs, overcoming the issues that the network experienced in December 2017, when traffic was particularly high.

When the issues slowing adoption are resolved, cryptocurrency payments could be embedded in checkout-free platforms to enable automated payments in brick-and-mortar stores. Smart contracts could be used to process payments automatically following the shopper’s action of leaving a physical store with a bag of items that they have selected, as detected by sensors operating as part of the IoT system in store, and the payment could be processed using cryptocurrencies.

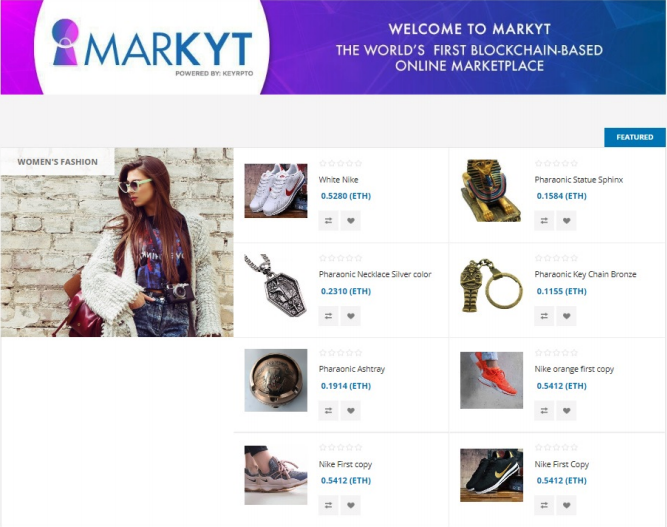

Decentralizing E-Commerce Marketplaces

Blockchain technology is used in e-commerce to decentralize marketplaces, enabling the seller and buyer to engage in a commercial relationship without the need for an intermediary. In decentralized marketplaces the blockchain can verify that the buyer has actually paid for the items purchased and that the seller has shipped the products. The advantages that decentralized marketplaces can have over traditional online marketplaces include the possibility of lower or no fees at all for opening a store or listing items, and no commissions on sales. Moreover, shoppers are not required to have a bank account as they can pay with cryptocurrencies.

Examples of blockchain-based e-commerce marketplaces include OpenBazaar, an open-source, decentralized marketplace for peer-to-peer commerce, and e-commerce portal Markyt, a blockchain platform that enables sellers and buyers to exchange products using cryptocurrency payments.

[caption id="attachment_79398" align="aligncenter" width="580"]

Source: Coinmap.org[/caption]

Developers are working to solve the problems that prevent cryptocurrency payment adoption. For example, the introduction of Lightning Network in 2018 — a second layer payment protocol that operates on top of a blockchain — have increased the speed of transactions and reduced costs, overcoming the issues that the network experienced in December 2017, when traffic was particularly high.

When the issues slowing adoption are resolved, cryptocurrency payments could be embedded in checkout-free platforms to enable automated payments in brick-and-mortar stores. Smart contracts could be used to process payments automatically following the shopper’s action of leaving a physical store with a bag of items that they have selected, as detected by sensors operating as part of the IoT system in store, and the payment could be processed using cryptocurrencies.

Decentralizing E-Commerce Marketplaces

Blockchain technology is used in e-commerce to decentralize marketplaces, enabling the seller and buyer to engage in a commercial relationship without the need for an intermediary. In decentralized marketplaces the blockchain can verify that the buyer has actually paid for the items purchased and that the seller has shipped the products. The advantages that decentralized marketplaces can have over traditional online marketplaces include the possibility of lower or no fees at all for opening a store or listing items, and no commissions on sales. Moreover, shoppers are not required to have a bank account as they can pay with cryptocurrencies.

Examples of blockchain-based e-commerce marketplaces include OpenBazaar, an open-source, decentralized marketplace for peer-to-peer commerce, and e-commerce portal Markyt, a blockchain platform that enables sellers and buyers to exchange products using cryptocurrency payments.

[caption id="attachment_79398" align="aligncenter" width="580"] Source: www.markyt.shop[/caption]

Key Takeaways: Promoting Industry Collaboration Thanks to the Blockchain

Blockchain applications in retail are still at an early stage. Nevertheless, things are moving in the industry and many companies are starting to experiment with the technology.

As we have outlined in this report, the deployment of the blockchain in conjunction with IoT systems in supply chain management for provenance tracking, preventing safety issues and counterfeiting is one of the most promising applications of the technology in the retail industry. Integrating blockchain into IoT systems contributes to the digitalization of the supply chain by decentralizing the management of operations, making the whole system more transparent, efficient and secure.

We have seen from the experience of large companies such as Walmart, Alibaba and Kroger that collaboration becomes important when implementing blockchain systems. The collaboration can be twofold, with technology companies and tech startups which have the technical expertise to set up the system, and with partners in the industry, typically thorough consortia of firms, to share the costs and the risk of applying the technology but also to make the system more effective through collaboration.

The ability of the blockchain to encourage collaboration among industry players is probably the key strength of the application of the technology in many sectors including retail. Because of its decentralized nature, all partners in the system are equal, collaboration is encouraged and the use of cryptographic records makes transactions visible to all but without necessarily revealing details that companies are not comfortable to share with their competitors.

Source: www.markyt.shop[/caption]

Key Takeaways: Promoting Industry Collaboration Thanks to the Blockchain

Blockchain applications in retail are still at an early stage. Nevertheless, things are moving in the industry and many companies are starting to experiment with the technology.

As we have outlined in this report, the deployment of the blockchain in conjunction with IoT systems in supply chain management for provenance tracking, preventing safety issues and counterfeiting is one of the most promising applications of the technology in the retail industry. Integrating blockchain into IoT systems contributes to the digitalization of the supply chain by decentralizing the management of operations, making the whole system more transparent, efficient and secure.

We have seen from the experience of large companies such as Walmart, Alibaba and Kroger that collaboration becomes important when implementing blockchain systems. The collaboration can be twofold, with technology companies and tech startups which have the technical expertise to set up the system, and with partners in the industry, typically thorough consortia of firms, to share the costs and the risk of applying the technology but also to make the system more effective through collaboration.

The ability of the blockchain to encourage collaboration among industry players is probably the key strength of the application of the technology in many sectors including retail. Because of its decentralized nature, all partners in the system are equal, collaboration is encouraged and the use of cryptographic records makes transactions visible to all but without necessarily revealing details that companies are not comfortable to share with their competitors.

Source: Coresight Research[/caption]

These features make blockchain technology attractive for applications in the retail space, particularly in support operations in supply chain and logistics, but also in customer data management, loyalty programs,Marketplaces and payments, as illustrated in figure 2.

[caption id="attachment_79390" align="aligncenter" width="580"] Source: Coresight Research[/caption]

We believe blockchain technology has the potential to improve all processes of digitalization in the supply chain and retail operations that currently use centralized systems. For example, digitalizing the supply chain entails using centralized Internet of Things (IoT) frameworks, which uses a central server – making it more vulnerable as there is one single point of failure that can be targeted. Data on the blockchain cannot be tampered once recorded, there is no single point of failure, since the system is run on multiple servers and there is no central authority that can arbitrarily modify the system without the consensus of the other parties.

Blockchain applications in retail are still at an early stage. Nevertheless, many companies are experimenting with the technology. A 2018 survey conducted by IBM among executives in retail and consumer goods from 203 organizations in 16 countries showed that 18% of companies have already started investing in the deployment of the technology in their business, while 70% of consumer industry executives surveyed expect to have a blockchain production network in three years. This shows most companies believe in the technology’s potential to have a real impact on the industry in the next few years.

Enhancing Supply Chain Traceability

Blockchain technology allows partners in the supply chain to track items accurately throughout the product cycle. This is particularly valuable when supporting highly fragmented and geographically dispersed sourcing systems in industries such as apparel, valuable items such as luxury goods, items at risk of counterfeiting such as pharmaceuticals, or perishables such as fresh food.

Figure 3 illustrates the application of the blockchain to enhance traceability within the supply chain. During the different stages of the product cycle, partners register the information on the status of the items through technologies such as smartphones, smart tags and sensors. All data is recorded on the blockchain, which guarantees that no party can alter historic entries, enabling trust without the need of an intermediary. Consumers can verify the provenance and authenticity of products by reading the information on the product cycle stored in the blockchain.

[caption id="attachment_79391" align="aligncenter" width="580"] Source: Coresight Research[/caption]

Retailers are already working for the implementation of blockchain platforms in their supply chain operations, often in collaboration with technology firms. Notable examples include:

- US retailer Walmart is working with technology firm IBM to develop a food-safety blockchain platform. Walmart wants to respond more effectively to food safety issues by digitalizing fresh food traceability. If contaminated food is discovered, the information in the blockchain would enable straightforward identification of all batches that came from that producer, enabling the company to quickly discard specific batches. Walmart announced in September 2018 that all suppliers of leafy green vegetables will be required, by September 2019, to upload product data to the food-safety blockchain platform. IBM is collaborating with other retailers, including Kroger, on blockchain-based platforms for food supply chain tracking.

- E-commerce and technology giant Alibaba launched a blockchain-based food tracking system, the company announced in April 2018. For this project, Alibaba worked with the Food Trust Framework, a consortium of New Zealand companies. Through the blockchain, the consortium will be able to authenticate, verify and record transfers of ownership and provisions of products, and will enable consumers to have access to reliable and comprehensive information on product’s origins through access to the information recorded on the distributer ledger. The system protects consumers from counterfeiting, enables partners in the consortium to detect fraud and react quickly to food contamination.

Source: Provenance.org[/caption]

Companies can also use the traceability potential of the blockchain to prevent counterfeiting, a particularly valuable application in sectors such as luxury and pharmaceuticals:

- In 2018, diamond firm De Beers and other six industry stakeholders developed Tracr, an end-to-end diamond-industry blockchain traceability platform. The company announced in May 2018 that it had successfully tracked 100 high-value diamonds along the value chain during Tracr’s pilot, marking the first time a diamond’s journey has been digitally tracked from mine to retail. Tracr will enable consumers to verify that the diamonds they buy are authentic and are sourced ethically, including that they are from mines that are not in war zones and free from child labor. Retailers including Signet Jewelers and Chow Tai Fook have joined the platform’s pilot program.

- New York-based premium sneaker manufacturer Greats collaborated with tech startups Chronicled and Origin to launch Beast Mode Sneakers in 2016, which are equipped with a blockchain-based system to prevent counterfeiting. The shoes embed a 3D printed smart tag with a unique identifying code and an encrypted near-field communication (NFC) tag that transmits the information to the blockchain. Wearers can scan the NFC tag with their smartphones to verify the authenticity of the item and to track the complete product cycle.

- BlockVerify is a tech startup that uses the blockchain to avoid counterfeit products in pharmaceuticals, luxury items, jewelry and electronics. Through BlockVerify’s platform, items are labeled with a digital tag and verified along the supply chain. The value chain of the tagged product is recorded on the blockchain, enabling retailers and consumers to verify that the product is authentic.

Source: Coresight Research[/caption]

Companies including Fujitsu, Volkswagen, Hyundai and Bosch are testing the integration of the two technologies in their business operations. Hyundai, for example, is applying blockchain technology to enable effective communication, identification, authentication and data storage between IoT devices.

Examples of blockchain startups that have developed platforms specifically for the

integration of the blockchain with IoT include:

- VeChain integrates blockchain and IoT for applications in retail, logistics, supply chain and more. VeChain uses proprietary IoT sensors to track key metrics such as temperature, humidity and location information of a product throughout the supply chain. The data is transferred to VeChain’s blockchain to create an immutable record of the product’s state at any stage of the supply chain journey, enabling verification by regulatory authorities and consumers.

- Waltonchain combines blockchain with Radio Frequency Identification (RFID) in IoT systems for supply chain management. Waltonchain enables consumers to verify the authenticity and provenance of a product. RFID tags are embedded or attached to products such as clothing and transmit information about the status of the product which is recorded on the blockchain.

- Loomia: New York-based smart-fabrics startup Loomia is developing connected apparel that collects and transfer the wearer’s data — such as body temperature, location and frequency of wear — to the blockchain, enabling consumers to control how the information is used by companies and granting rewards for its use. For example, users could exchange the data they generate by wearing the items with companies in exchange for rewards points.

- Robin8: A platform enabling social media profile owners to retain control of the data generated by their online presence and to monetize social media activity by selling data to companies through the blockchain. Users can choose what to share about their social media engagement with advertizers and get rewarded with digital tokens for social network activities such as creating profiles, sharing content, promoting products, etc.

- Streamr: A blockchain-based marketplace that makes data streams tradeable. Consumers can sell the data they generate and buy the information they need. For example, the data on traffic congestion or road quality drivers generate by driving a smart car can be traded on the Streamr platform in exchange of information the driver might need, such as data on traffic or about fuel or electricity prices in the nearby gas and charging stations.

Source: Streamr.com[/caption]

With greater control of their data thanks to the use of the blockchain technology, consumers could decide which company has access to their data and how the information is going to be used. Consumers could ask companies for incentives in exchange for the data they share, such as vouchers that could be spent on goods or services provided by the data recipient.

Enhancing Loyalty Programs Rewards and Effectiveness

Blockchain has the potential to disrupt the way companies manage loyalty programs. Retailers can use the technology to improve how they handle consumer data. With the support of the blockchain, consumers can use their reward points more effectively. The distributed nature of the blockchain can encourage loyalty scheme collaborations between companies which can prove beneficial for both retailers and consumers. The advantages of using a blockchain system to manage loyalty schemes include:

- Safer storage: Retailers can benefit from a decentralized storage system which is more difficult to hack than centralized databases, reducing the risk of points being stolen or other fraud. Companies can reduce the reputational and legal risks resulting from database hacks.

- Empowering consumer rewards: Loyalty points earned by consumers can take the form of digital tokens tradeable on the blockchain. The blockchain could encourage companies to set up joint loyalty schemes with the participation of multiple companies so consumers can redeem or spend the tokenized points earned from one company on another participating partner, giving consumers more options on how they can spend their points. For example, airlines could set up joint reward schemes run on a blockchain, enabling customers to redeem air miles from other companies according to their travel route needs.

- Enhanced reward customization: Rewards programs can collect valuable information on the blockchain about the products and services customers are redeeming the points for, enhancing profiling and customizing.

Source: Overstock.com[/caption]

Increasing Payment Options

At its conception, the blockchain was conceived as a technology to enable payments without intermediaries such as financial institutions. In retail, the opportunity is to accept cryptocurrencies as a form of payment to add to other, more established, payment methods such as credit cards and cash.

However, there remain a number of challenges that stop major retailers from more widely adopting blockchain-based payment systems. Together with the uncertain legal status of cryptocurrencies in many countries, technical issues with the technology prevent significant adoption, including:

- Price volatility: The value of cryptocurrencies is volatile. The bitcoin ranged from more than $15,000 in early January 2018 to about $4,000 during the same period in 2019.

- Slow transaction time: Transactions are not instant and can take several hours to validate, particularly during high-traffic periods when many transactions are processed through the blockchain.

- High transaction fees: Volatility also occurred with transaction fees, which, while normally are comparatively low, in periods of high network traffic can be particularly high. For example, the average bitcoin transaction fee peaked to $52 on December 23, 2017, while was just $0.3 on January 6, 2019, according to cryptocurrency statistics portal com.

Source: Overstock.com[/caption]

As of January 8, 2019, there were 14,166 venues accepting cryptocurrencies worldwide, according to Coinmap.org, a portal which shows the location of companies accepting cryptocurrencies worldwide.

[caption id="attachment_79397" align="aligncenter" width="580"] Source: Coinmap.org[/caption]

Developers are working to solve the problems that prevent cryptocurrency payment adoption. For example, the introduction of Lightning Network in 2018 — a second layer payment protocol that operates on top of a blockchain — have increased the speed of transactions and reduced costs, overcoming the issues that the network experienced in December 2017, when traffic was particularly high.

When the issues slowing adoption are resolved, cryptocurrency payments could be embedded in checkout-free platforms to enable automated payments in brick-and-mortar stores. Smart contracts could be used to process payments automatically following the shopper’s action of leaving a physical store with a bag of items that they have selected, as detected by sensors operating as part of the IoT system in store, and the payment could be processed using cryptocurrencies.

Decentralizing E-Commerce Marketplaces

Blockchain technology is used in e-commerce to decentralize marketplaces, enabling the seller and buyer to engage in a commercial relationship without the need for an intermediary. In decentralized marketplaces the blockchain can verify that the buyer has actually paid for the items purchased and that the seller has shipped the products. The advantages that decentralized marketplaces can have over traditional online marketplaces include the possibility of lower or no fees at all for opening a store or listing items, and no commissions on sales. Moreover, shoppers are not required to have a bank account as they can pay with cryptocurrencies.

Examples of blockchain-based e-commerce marketplaces include OpenBazaar, an open-source, decentralized marketplace for peer-to-peer commerce, and e-commerce portal Markyt, a blockchain platform that enables sellers and buyers to exchange products using cryptocurrency payments.

[caption id="attachment_79398" align="aligncenter" width="580"] Source: www.markyt.shop[/caption]

Key Takeaways: Promoting Industry Collaboration Thanks to the Blockchain

Blockchain applications in retail are still at an early stage. Nevertheless, things are moving in the industry and many companies are starting to experiment with the technology.

As we have outlined in this report, the deployment of the blockchain in conjunction with IoT systems in supply chain management for provenance tracking, preventing safety issues and counterfeiting is one of the most promising applications of the technology in the retail industry. Integrating blockchain into IoT systems contributes to the digitalization of the supply chain by decentralizing the management of operations, making the whole system more transparent, efficient and secure.

We have seen from the experience of large companies such as Walmart, Alibaba and Kroger that collaboration becomes important when implementing blockchain systems. The collaboration can be twofold, with technology companies and tech startups which have the technical expertise to set up the system, and with partners in the industry, typically thorough consortia of firms, to share the costs and the risk of applying the technology but also to make the system more effective through collaboration.

The ability of the blockchain to encourage collaboration among industry players is probably the key strength of the application of the technology in many sectors including retail. Because of its decentralized nature, all partners in the system are equal, collaboration is encouraged and the use of cryptographic records makes transactions visible to all but without necessarily revealing details that companies are not comfortable to share with their competitors.